Ambulatory Anesthesia: Everything You Wanted to Know But Were Afraid to Ask

Howard Greenfield, MD

Co-Founder and Principal, Enhance Healthcare Consulting, Aventura, FL

Jody Locke, MA

Vice President of Anesthesia and Pain Practice Management Services Anesthesia Business Consultants, LLC, Jackson, MI

The steady migration of surgical cases from traditional inpatient to non-traditional outpatient and ambulatory venues has required anesthesiologists and CRNAs, the quintessential service providers, to continuously reinvent themselves to adapt to evolving market conditions and customer expectations. The assumptions and strategies that helped many anesthesia groups build successful partnerships with hospitals may no longer serve them well in today’s dynamic ambulatory environment.

The steady migration of surgical cases from traditional inpatient to non-traditional outpatient and ambulatory venues has required anesthesiologists and CRNAs, the quintessential service providers, to continuously reinvent themselves to adapt to evolving market conditions and customer expectations. The assumptions and strategies that helped many anesthesia groups build successful partnerships with hospitals may no longer serve them well in today’s dynamic ambulatory environment.

Today’s medical mantra is “value proposition.” Anesthesia providers are no longer being asked simply to provide safe and effective anesthesia care. They are also expected to create value for the facility. The ability to generate this value requires close collaboration with the facility’s leadership, staff and surgeons.

If there is one overarching distinction between traditional hospital agreements and ambulatory agreements, it is the availability of subsidy money. While most hospitals are willing to provide financial support for unprofitable business lines, this is rarely, if ever, the case in the ambulatory environment. This reality of ambulatory anesthesia means that the anesthesia practice must make sure the arrangement with an ambulatory surgery center (ASC) makes financial sense before proceeding.

Is it time for anesthesia practices to evaluate and pursue ambulatory opportunities? The answer is yes, but caveat emptor: buyer beware. Never has it been so important to exercise rigorous due diligence and to objectively evaluate the potential benefits and risks. In the past, relationships with most ambulatory facilities would only enhance an anesthesia practice. This is no longer the case. The three rules of success are: 1) know what you are getting yourself into; 2) make sure the numbers make sense; and 3) monitor performance closely and continuously.

Types of Ambulatory Practices

While we tend to think of ambulatory anesthesia as a generic term, the fact is that no two ambulatory facilities—and therefore, no two ambulatory anesthesia agreements—are the same. To understand the challenges and opportunities associated with this new anesthesia frontier, it is useful to think in terms of five subsets of facilities and types of cases. These categories offer a framework for the key financial and strategic issues that anesthesia practices should consider before signing an agreement with a new facility:

- Hospital-owned outpatient facilities that are physically part of the hospital campus, billed with a place of service code -22;

- Freestanding ASCs that represent a joint venture between a hospital and surgeons, billed with a place of service -24 modifier;

- Surgeon-owned freestanding ASCs, also billed with a -24 modifier, but which may have different financial objectives than the hospital joint venture facilities;

- Single specialty centers, such as an endoscopy center, an eye center or a center for reproductive medicine, billed with a -24 modifier;

- A doctor’s office, billed with a place of service -11 modifier. Anesthesia provider to be asked to cover dental or plastic surgeons’ offices.

A Range of Realities

The challenges of successful anesthesia practice management in any of these types of facilities can be significant. The fact that ambulatory cases are shorter, of lower acuity and turn over faster may seem advantageous, but these characteristics create an entirely different set of customer expectations than those in hospital operating rooms (ORs). To understand this difference, think of email and texting. When people talked on the phone and sent documents by mail or messenger there was no expectation that things would happen instantly. The advent of texting and email has created an expectation of an instant response. Today’s well-run surgery center epitomizes the application of business principles to medicine, where the real measure of success is customer service, efficiency and profitability.

Smaller facilities with smaller staffs tend to require and encourage a collaborative approach to care delivery. Some anesthesiologists and CRNAs perform better than others in an environment where efficiency and throughput are a primary objective. These high-velocity facilities require high-velocity providers. Anesthesia practices will find that only a select subset of anesthesiologists and CRNAs work well in such settings. This is the place for skilled providers with proficiency in regional anesthesia and acute pain techniques. Contracts can easily be lost because of incompatible staff assignments.

Beyond these staffing considerations, the anesthesia practice must also deal with the economic realities of an ambulatory environment. Logistics and resource deployment can be far more challenging, especially if the practice covers multiple outpatient facilities in addition to its primary hospital. In the main hospital OR, a team of providers can be assigned to cases as needed, with an expectation that, on average, there are enough cases or subsidy to cover staff costs.

This is not the case with outpatient and ambulatory facilities, especially if they need anesthesia only a few days a week or if anesthesia is needed for only a few cases per day. Large practices with multiple outpatient relationships often create a separate scheduling function to ensure that their providers meet their obligations at the various facilities in a timely manner. The economics of ambulatory anesthesia are not always as favorable as one might expect. Practices often focus on general production data that does not allow the practice to compare business lines or assess their profitability. Standard billing reports that simply show basic anesthesia values such as cases, units, charges and payments by month—even if they include a breakdown by facility—will never be adequate to manage an expanding and dynamic book of ambulatory business.

This is not the case with outpatient and ambulatory facilities, especially if they need anesthesia only a few days a week or if anesthesia is needed for only a few cases per day. Large practices with multiple outpatient relationships often create a separate scheduling function to ensure that their providers meet their obligations at the various facilities in a timely manner. The economics of ambulatory anesthesia are not always as favorable as one might expect. Practices often focus on general production data that does not allow the practice to compare business lines or assess their profitability. Standard billing reports that simply show basic anesthesia values such as cases, units, charges and payments by month—even if they include a breakdown by facility—will never be adequate to manage an expanding and dynamic book of ambulatory business.

Numbers Tell the Story

The use of normalized data is essential for understanding each ambulatory setting’s value to the practice as a whole. The fact that collections at one facility are twice as high as at another says nothing about their real value. As any manager responsible for multiple business lines will attest, business lines must be compared using the same criteria and benchmarks. This consistency is especially important in practice management in anesthesia. There is discussion in the field about which type of normalized metric is most useful. We will discuss common examples and weigh their value, including yield per unit, yield per hour and yield per provider day.

Table 1 provides a high-level example. The table shows data for 766 ABC client ambulatory facilities across the country for calendar year 2017. The first two metrics—units per case and yield per unit—are the revenue drivers that determine the next three metrics. Yield per hour can be a useful comparative metric if the objective is to compare business lines. However, many find the last two metrics of most value in assessing a coverage agreement’s potential profitability. Based on this sample, only two types of facilities cover the cost of a physician anesthesiologist.

There are three main challenges in ASC staffing:

- The number of days per week that coverage is required. While it can be advantageous if a facility generates a few extra cases that can be done during down time, often these cases are performed during peak morning times, which means extra resources are needed for additional morning starts.

- The consistency of production. An anesthesia practice needs a guarantee of revenue to cover manpower costs. Unpredictable weekly coverage and daily swings in case volumes create a potentially risky situation.

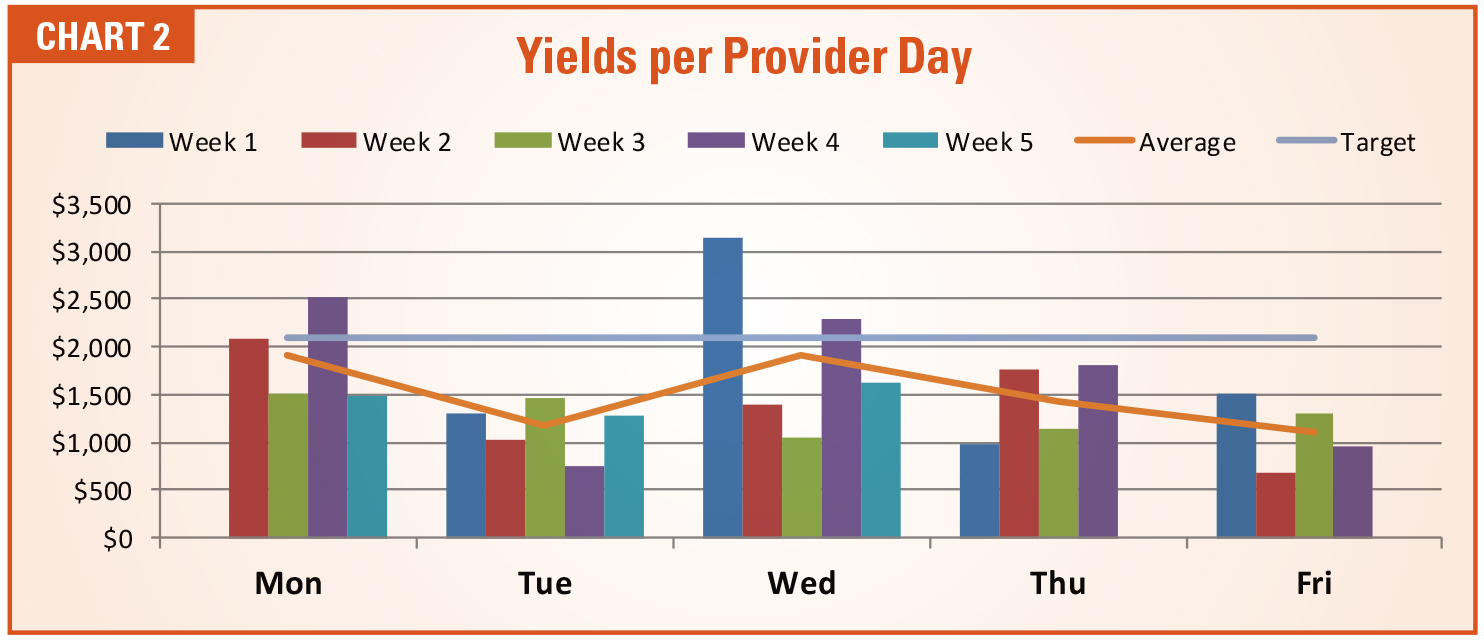

- The average yield per clinical provider day. Production metrics must be calculated as averages over time. A few profitable days does not make for a profitable relationship.

As indicated in Chart 2, most physician- only practices find it difficult to profitably staff ambulatory facilities. The cost of a physician-only practice in the current environment is simply too high, at $2,100 per provider day. Even if the average cost can be driven down to $1,700 or $1,800 with the use of a care team model, that is still higher than the average value of $1,540 shown in Table 1. There may be offsetting strategic or tactical reasons to incur such a loss, but it is still a loss.

Making the Most of a Good Thing

Given all these challenges, then, what is the upside? The difference between a profitable arrangement and an unprofitable one hangs on three key factors: consistency of production, consistency of collections and cost of providing the requested coverage.

Consistency of Production

A practice cannot manage what it does not measure. For example, consider production consistency. In an ambulatory environment this metric should be monitored by day. Chart 1 provides a typical example. Typically, an anesthesia practice staffs for a daily number of 7:30 am starts, meaning that first-case starts determine the staffing needed for the facility. The hope and the assumption are that sufficient activity in the OR will cover the cost of the providers. While this is not always the case in the hospital, it is definitely not always the case in the ambulatory environment. The smaller the facility, the greater the challenge.

Consistency of Collections

Billed ASA units are the most useful production metric in anesthesia. Conventional wisdom holds that an optimally run hospital OR suite should consistently generate 50 billed units per location day. Table 3 represents actual production data based on date of service (DOS) for January, 2018 for a randomly selected ABC client facility. Note that most rooms do not meet the target threshold.

Cost of Providing Coverage

For this reason, it is useful to monitor actual collections per provider location day (see Table 2). While Chart 1 may bear a striking resemblance to Chart 2, the financial scale of the data makes it far more relevant to the management of the practice. The target here is based on the daily provider cost of a physicianonly practice. If we assume that the total burdened cost (base compensation plus overhead and benefits) is $490,000 and that the physician works 231 days a year, then the cost would be $2,100 per physician day. This number might be high for some practices and some parts of the country. Actual target yields will vary based on region. Practices applying this analysis are advised to use actual data.

What value does this information have for a practice? If specific business lines are underperforming, the practice has three choices:

- Accept the loss for broader strategic reasons.

- Identify opportunities to increase revenue. Subsidies are rarely an option in an ASC, but there may be other ways to enhance revenue. For example, some practices have added 10 percent to their revenue with the inclusion of additional services such as the appropriate use of nerve blocks and ultrasonic guidance in orthopedic facilities.

- Consider ways of reducing the costs of care.

In the example provided, the practice can manage with physicians only, since the average daily collections are roughly equal to the cost of the physicians (see Table 2). However, as shown in Table 3 this is rarely the case. Many factors determine the cost per anesthetizing location. Table 2 shows the basic elements of the calculation: the total cost of each category of provider, the number of weeks each works and the number of clinical location days to be covered.

This represents an ideal situation, in which a practice has the opportunity to dedicate three CRNAs under the direction of a physician. This is very rarely the case. However, changes in the staffing model may be problematic for some practices for a variety of philosophical and practical reasons. Many anesthesiologists prefer to work alone and not medically direct CRNAs. Until recently, private anesthesia groups in California rarely employed CRNAs, despite the fact that they were routinely used in academic centers, Kaiser hospitals, the military and small, rural facilities.

Qualified CRNAs may not be readily available in certain markets. As some of the nation’s largest staffing companies convert to a medical direction model, which has increased the demand for CRNAs, the supply has yet to catch up. A number of practices considering hiring CRNAs report that it is not easy to find providers who are willing to work where the practice needs them.

Changes in staffing model or the development of a new staffing model for a facility must be carefully evaluated. An anesthesia practice can’t change its culture or mode of delivery quickly. New entities are being formed on a regular basis to target the ambulatory market. Almost without exception, these entities are based on a care team model, where anesthesiologists supervise CRNAs or anesthesiologist assistants.

Critical Metrics

In this era of rapid change, metrics matter. There can be no doubt about the value of clinical data in the OR. Most providers pride themselves on being able to make timely and accurate clinical decisions in a matter of seconds. Why, then, do so few practices fail to apply this same principle to the management of their practices? It is probably the result of a perception that, unlike anesthesia delivery, anesthesia practice management is not a time-critical exercise. No one talks about hours of boredom punctuated by moments of sheer terror in the anesthesia board meeting. However, practices that don’t monitor key metrics closely can make some costly mistakes.

Three distinct management metrics are often confused in the assessment of anesthesia staffing: provider productivity, OR utilization and profitability. Each has its place in the ongoing evaluation of any coverage arrangement.

Provider Productivity

Provider productivity is the term most commonly misused. Technically, it is a measure of the manner in which a provider completes their assigned cases. In other words, if there are only three cases on the schedule and the anesthesia provider completes them all satisfactorily, then they have achieved 100 percent productivity. This said, different fewer units in the completion of the same number of cases than their colleagues, which could be considered a measure of productivity, but very few practices seriously monitor such measures.

OR Utilization

Most practices are actually interested in OR utilization. This is a comparison of actual to potential production. If an OR is open for cases for eight hours a day, then the optimal utilization is typically considered to be six hours. Utilization metrics are normally calculated as a percentage of potential. Six hours of billed anesthesia time during an eight-hour shift would represent 75 percent utilization. It can be useful to compare actual billed hours of anesthesia time to coverage requirements. This is especially useful in that manpower and staffing is always a function of the facility’s coverage requirements.

Profitability

Profitability is not always an easy concept to apply to an anesthesia practice in which providers simply get paid based on collections net of expenses. If it costs you $.50 to make a hamburger and you sell it for $2.00 then your profit is $1.50 per burger. While most practices do not think this way, profit is defined as revenue generated minus the expense of providing the service. If it costs the practice $2,130 per provider day and the practice generates $1,700 per day, then the arrangement is unprofitable. However, if the cost can be reduced to $1,580, then the same level of revenue would result in a profitable arrangement. However, unless you have this information you cannot really know whether the arrangement is profitable or not.

It used to be that success in anesthesia was defined simply in terms of collections. A favorable payer mix and busy ORs were all a practice needed to be successful. Life is no longer so simple. Anesthesia providers must now learn the arcane science of cost accounting. For each venue or line of business, the practice should be able to clearly monitor both the revenue potential and the actual cost. Table 3 is an example of what this might look like. It is based on actual data for a practice in the western United States. Because this is a physician-only practice that allows providers to work as much or as little as they want, the cost part of the equation has yet to be established. Even so, this data clearly demonstrates the financial value of each facility.

Strategic Considerations

The five categories of ambulatory practices shown in Table 1 represent a continuum of management opportunities and challenges. Increasingly, anesthesia practices are actively pursuing new venues and lines of business to diversify. The good news is that well-managed outpatient venues can increase the yield per day and offset hospital coverage and call obligations. The problem is that not all outpatient venues are such a good fit. Adding venues and case volume for the sake of growing a practice can be a very bad idea, especially if new venues require additional manpower and staffing whose costs are not covered by additional revenue potential.

The five categories of ambulatory practices shown in Table 1 represent a continuum of management opportunities and challenges. Increasingly, anesthesia practices are actively pursuing new venues and lines of business to diversify. The good news is that well-managed outpatient venues can increase the yield per day and offset hospital coverage and call obligations. The problem is that not all outpatient venues are such a good fit. Adding venues and case volume for the sake of growing a practice can be a very bad idea, especially if new venues require additional manpower and staffing whose costs are not covered by additional revenue potential.

Most American hospitals now provide care on an inpatient and outpatient basis. This is considered essential in the current environment. How they achieve the objective or provide a more customer-friendly environment for healthy patients undergoing relatively minor procedures may vary greatly. Some will try to create the look and feel of an ambulatory environment in existing ORs. When this occurs, anesthesia is essentially a captive participant to the change. The hope is that the facility restructuring will increase cases and improve the payer mix.

For the anesthesia practice, such developments tend to represent a difference of degree rather than of kind. The outpatient unit’s focus and business objectives may be more specific, but the outpatient ORs are typically managed by the same people and in the same manner as the inpatient rooms.

The freestanding surgery center that is a hospital joint venture with a group of surgeons represents the next step in the migration of surgical cases from the hospital to the freestanding environment. Various factors may motivate such an arrangement. Every administration is competing for surgeon allegiance. The establishment of a patient-friendly facility with convenient ingress and egress may be one way to accomplish this. The joint venture may be a preemptive strike to keep the surgeons from building their own facility and competing with the hospital.

There is a critical management concept at work here that can have a significant impact on anesthesia. Hospitals must serve a range of customers and, therefore, strive to develop policies that provide a consistent level of service. The hospital will try to schedule cases together as efficiently as possible to maximize the return for a day’s work. They want surgeons to complete cases as expeditiously as possible. Surgeons, by contrast, may want to do a couple of cases in the morning, go to their office and then come back for a case or two in the afternoon. The result can be a significant amount of unproductive downtime for the anesthesia providers.

Each of these types of facilities must be evaluated on its own merits. It can be dangerous to assume that what worked at facility A will now have the same results in facility B. Herein lies one of the trickiest aspects of the ambulatory anesthesia market. How do you determine that covering a facility will be a good deal?

It all starts with the data. If the facility can provide reliable payer mix and volume information, the practice can project revenue. Clearly defined coverage requirements will allow for the formulation of a staffing model. However, such detail often is not available. This can be a big problem. Miscalculating revenue can be very serious. Facilities in rampup mode tend to be overly optimistic in projecting the likelihood of achieving an optimum run-rate.

Working in a doctor’s office, which does not have all of the equipment and recovery drugs for general anesthesia as a hospital or ASC, poses its own set of challenges. The doctor’s office is the extreme end of the convenience/safety continuum. Most of the resources and safeguards that make a hospital OR a safe place to provide anesthesia are typically absent in the doctor’s office. If there is an anesthesia machine, the anesthesiologist may have to provide it. The doctor’s office is the ultimate example of bowing to the surgeon’s needs. Agreeing to provide general anesthesia under such circumstances assumes that one has a very good relationship with the surgeon, that the patients are consistently healthy, and that the payer mix and volume cover the costs of the provider’s with such an environment.

As in so many aspects of business, deciding whether to provide anesthesia outside of the hospital involves a risk-benefit calculation. The specialty prides itself on its safety. Morbidity and mortality related to anesthesia are at an all-time low. The tragic story of Joan Rivers is a constant reminder that such standards should never be compromised.

The Real Question

Most anesthesia practices now understand that they have only three options to survive: expand, merge or sell out. There are very few practice situations where the status quo will work. Hospitals are merging. Customer expectations are changing. The economics of anesthesia are becoming increasingly more challenging. More than 75 percent of all group practices need some level of financial support to survive. So there are many reasons to actively explore practice options. The question is what options actually make sense? The logical tendency is to follow the cases as they migrate into non-traditional venues. It has become inevitable, but is it a good thing?

Most anesthesia practices now understand that they have only three options to survive: expand, merge or sell out. There are very few practice situations where the status quo will work. Hospitals are merging. Customer expectations are changing. The economics of anesthesia are becoming increasingly more challenging. More than 75 percent of all group practices need some level of financial support to survive. So there are many reasons to actively explore practice options. The question is what options actually make sense? The logical tendency is to follow the cases as they migrate into non-traditional venues. It has become inevitable, but is it a good thing?

The answer depends on the following factors:

An appropriate culture and structure is a prerequisite. Many small practices (fewer than 10 providers) simply do not have the depth of staff or the flexibility to expand, which is a limitation they may ultimately have to deal with. Other practices consist of providers who are risk-averse and therefore disinclined to take on additional coverage responsibilities. There are practices that simply feel comfortable with the practice they have and have no desire to complicate things.

The financial objectives of the members can be an essential determinant but may also be a source of great debate or conflict. For example, younger members may be very eager to expand the practice and position it for the future, while older members with an eye on retirement may not be so inclined. Obviously, any decision to expand the practice must have membership support. Many practices have watched opportunities come and go as they debated the merits.

At issue is whether the additional venue will enhance partner or shareholder compensation. This is where practice demographics really come into play. Millennials with medical school loans and big mortgages are more inclined to assume risk than those who are closing in on the end of their career. This places a special burden on management to demonstrate the value of the additional cases.

The local market is also a critical factor. Some locations are more target-rich than others. Many practices feel they must pursue every anesthesia opportunity in the local market in order to fend off potential competitors. However, not every practice that wants to expand has the ability to do so without looking at venues that are distant to the primary sites. Careful environmental scanning is an essential prerequisite for any level of expansion. Management must be aware of any and all opportunities and have the ability to assess them objectively.

A practice’s structure and infrastructure will either facilitate or complicate a successful expansion. Some practices are run in a more business-like manner than others. A decision to take on another facility requires decisiveness and strong management. The practice must have a clear chain of command and the ability to manage remote sites effectively. The practice has to be able to clearly demonstrate its ability to meet customer expectations and requirements consistently.

One of the distinct advantages that the nation’s largest staffing companies can demonstrate is their organizational structure. This allows them to prepare more impressive proposals, present more compellingly and monitor ongoing performance more consistently. It is not uncommon for an inexperienced management team to mess up the first few proposals.

Strategic thinking is a relatively new discipline for anesthesia practices. How will a practice position itself to survive in the current environment? The answers and options are not always clear. This can be the most complicated issue of them all.

Howard Greenfield, MD, co-founder and principal of Enhance Healthcare Consulting, is a board certified anesthesiologist with a thorough understanding of the financial and clinical needs of both hospitals and anesthesia providers. Throughout his career, he has worked with hospitals and providers to align incentives and develop cost-effective and timely solutions for OR management. In addition, he has expertise in optimizing anesthesia group and OR performance by working collaboratively with hospital administration, surgeons, OR nurses and anesthesiologists nationwide. He was a founding partner of Sheridan Healthcare and served as chief of anesthesia at Memorial Regional Hospital, Hollywood, FL. Dr. Greenfield received his training at Temple University School of Medicine and Jackson Memorial/University of Miami. He can be reached at hgreenfield@enhancehc.com or (954) 242-1296.

Howard Greenfield, MD, co-founder and principal of Enhance Healthcare Consulting, is a board certified anesthesiologist with a thorough understanding of the financial and clinical needs of both hospitals and anesthesia providers. Throughout his career, he has worked with hospitals and providers to align incentives and develop cost-effective and timely solutions for OR management. In addition, he has expertise in optimizing anesthesia group and OR performance by working collaboratively with hospital administration, surgeons, OR nurses and anesthesiologists nationwide. He was a founding partner of Sheridan Healthcare and served as chief of anesthesia at Memorial Regional Hospital, Hollywood, FL. Dr. Greenfield received his training at Temple University School of Medicine and Jackson Memorial/University of Miami. He can be reached at hgreenfield@enhancehc.com or (954) 242-1296.

Jody Locke, MA, serves as Vice President of Anesthesia and Pain Practice Management Services for Anesthesia Business Consultants. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He is a key executive contact for groups that enter into contracts with ABC. Mr. Locke can be reached at Jody.Locke@AnesthesiaLLC.com.

Jody Locke, MA, serves as Vice President of Anesthesia and Pain Practice Management Services for Anesthesia Business Consultants. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He is a key executive contact for groups that enter into contracts with ABC. Mr. Locke can be reached at Jody.Locke@AnesthesiaLLC.com.