What’s the Problem? Providers’ Waivers of Patient Copays or Deductibles

Frank Carsonie, JD

Chair, Health Care & Life Sciences Practice Group Benesch, Friedlander, Coplan & Aronoff LLP, Columbus, OH

Nathan Sargent, JD

Associate, Health Care & Life Sciences Practice Group Benesch, Friedlander, Coplan & Aronoff LLP, Cleveland, OH

Most health insurance plans are cost-sharing arrangements between the individual patient and the patient’s insurance payer. Depending on the plan’s structure, the patient is typically responsible for some combination of a monthly premium; a deductible; coinsurance; and/or copays. With the patient’s financial obligation established, the plan is then responsible for the balance of costs for covered healthcare services.

Most health insurance plans are cost-sharing arrangements between the individual patient and the patient’s insurance payer. Depending on the plan’s structure, the patient is typically responsible for some combination of a monthly premium; a deductible; coinsurance; and/or copays. With the patient’s financial obligation established, the plan is then responsible for the balance of costs for covered healthcare services.

Plans and healthcare providers establish rates and fee schedules for covered healthcare services by contract. Such rates and fee schedules are the result of extensive negotiations and are based on a number of factors. Despite the existence of such contractual arrangements, healthcare providers sometimes waive patient copays, coinsurance and deductibles (generally referred to as a “waiver” or “waivers” in this article). This happens with in-network and outof- network healthcare providers alike, and they do so for different reasons and under varying circumstances.

Regardless of the rationale, healthcare providers who grant waivers should know that there are serious healthcare fraud and abuse implications under federal and state law. It is an understatement to say the consequences of inappropriate waiver practices are significant.

The questions and answers below provide an overview of key laws and legal concepts, operational considerations and risk mitigation strategies related to healthcare providers granting waivers.

Under What Circumstances Are Copays, Coinsurance and Deductibles Typically Waived?

A patient’s deductible is the amount of healthcare-related costs the patient must incur before the patient’s plan begins to pay for healthcare services. Coinsurance is typically calculated as a percentage of the total cost of a given healthcare service for which the patient remains responsible. A copay is a fixed amount that the patient must pay for a specific healthcare service. A copay amount can vary based on the specific service or procedure and is often collected at the time of service. However, a copay can be collected at a later time or date.

Given the nature of when and how coinsurance, deductibles and copays are paid, providers typically grant waivers during patient intake (i.e., prior to service) or after a service has been provided and the patient has been deemed delinquent with payment. A waiver can be a full fee waiver, a partial fee write-down or discount, or a write-off once the patient obligation has been referred to collections.

As mentioned above, healthcare providers grant waivers for various reasons, such as to accommodate individual circumstance (e.g., financial hardship), as a professional courtesy or for marketing and business development purposes. The fraud and abuse concerns exist regardless of the reason for granting the waiver.

As mentioned above, healthcare providers grant waivers for various reasons, such as to accommodate individual circumstance (e.g., financial hardship), as a professional courtesy or for marketing and business development purposes. The fraud and abuse concerns exist regardless of the reason for granting the waiver.

What Law Applies to Patient Copay or Deductible Waivers?

At the federal level, healthcare provider waivers implicate civil monetary penalties under the Social Security Act as well as the Federal Anti-Kickback Statute.

Civil Monetary Penalties

According to Section 1128A(a)(5) of the Social Security Act, any person (including an organization, agency or other entity) that offers, or transfers, remuneration to an individual eligible for Medicare or Medicaid benefits, and such person knows or should know the remuneration is likely to influence an individual to order or receive a covered Medicare or Medicaid service from a particular healthcare provider, is subject to a civil monetary penalty (the CMP Law).

The penalty under the CMP Law can be up to $10,000 for each item or service, plus an assessment of “not more than three (3) times the amount claimed for each item or service.”1 In addition to the financial penalties, the Secretary of Health and Human Services has the ability to exclude such person from participating in the Medicare and Medicaid programs. A waiver can be considered remuneration likely to influence an individual to do business with a particular provider.

Federal Anti-Kickback Statute

The Federal Anti-Kickback Statute imposes criminal and civil monetary penalties on any person (an entity or individual) that knowingly and willfully pays or offers to pay any remuneration, directly or indirectly, overtly or covertly, in cash or in kind, to any person to induce such person to purchase, lease, order or arrange for any good, service or item for which payment may be made, in whole or in part, by a federal healthcare program, such as Medicare and Medicaid.2 The Federal Anti-Kickback Statute also prohibits a person from arranging for or recommending the purchase of goods or services for which payment may be made, in whole or in part, under a federal healthcare program in exchange for remuneration. A waiver can be considered remuneration to induce a patient to arrange for a service with the granting provider.

A violation of the Federal Anti-Kickback Statute may be prosecuted as a criminal action and is classified as a felony, punishable by fines of up to $25,000 per violation and imprisonment for up to five (5) years. Like the civil monetary penalties, a violation of the Anti-Kickback Statute may result in exclusion from participation in Medicare and Medicaid and the imposition of civil monetary penalties in an amount equal to treble damages plus $50,000 per violation. A violation of the Federal Anti-Kickback Statute may also result in collateral claims against the violator under the False Claims Act3 brought by enforcement authorities or through whistleblower actions, potentially resulting in additional civil monetary penalties of up to $10,000 per violation, plus treble damages.

State Law

In addition to federal authority, states often have their own healthcare fraud and abuse laws. Some states even have statutes and regulations that govern the specific practice of healthcare provider waivers. Others address the issue in provider disciplinary rules and standards of professionalism, expressly prohibiting a licensed practitioner from waiving patient insurance obligations except under certain circumstances. Regardless, it is critical to understand the federal and state requirements and limitations related to healthcare provider waivers prior to granting them.

In addition to federal authority, states often have their own healthcare fraud and abuse laws. Some states even have statutes and regulations that govern the specific practice of healthcare provider waivers. Others address the issue in provider disciplinary rules and standards of professionalism, expressly prohibiting a licensed practitioner from waiving patient insurance obligations except under certain circumstances. Regardless, it is critical to understand the federal and state requirements and limitations related to healthcare provider waivers prior to granting them.

What Waiver Practices Are Prohibited? What Practices Are Permitted? And Why?

Despite the foregoing, there are ways for healthcare providers to grant waivers compliantly. The critical point is to understand what is permitted and what is not.

Permissible Activity Under Civil Monetary Penalties

As it relates to the CMP Law, “remuneration” is specifically defined to include the waiver of coinsurance, copay and deductible amounts (or any part thereof). However, a waiver does not become remuneration subject to the CMP Law prohibitions if:

- The waiver is not offered as part of any advertisement or solicitation; and

- The healthcare provider does not routinely waive or reduce coinsurance, copay or deductible amounts; and

- The healthcare provider (a) waives or reduces the coinsurance, copay or deductible amounts after determining, in good faith, that the individual is in financial need or (b) fails to collect after making reasonable collection efforts.4

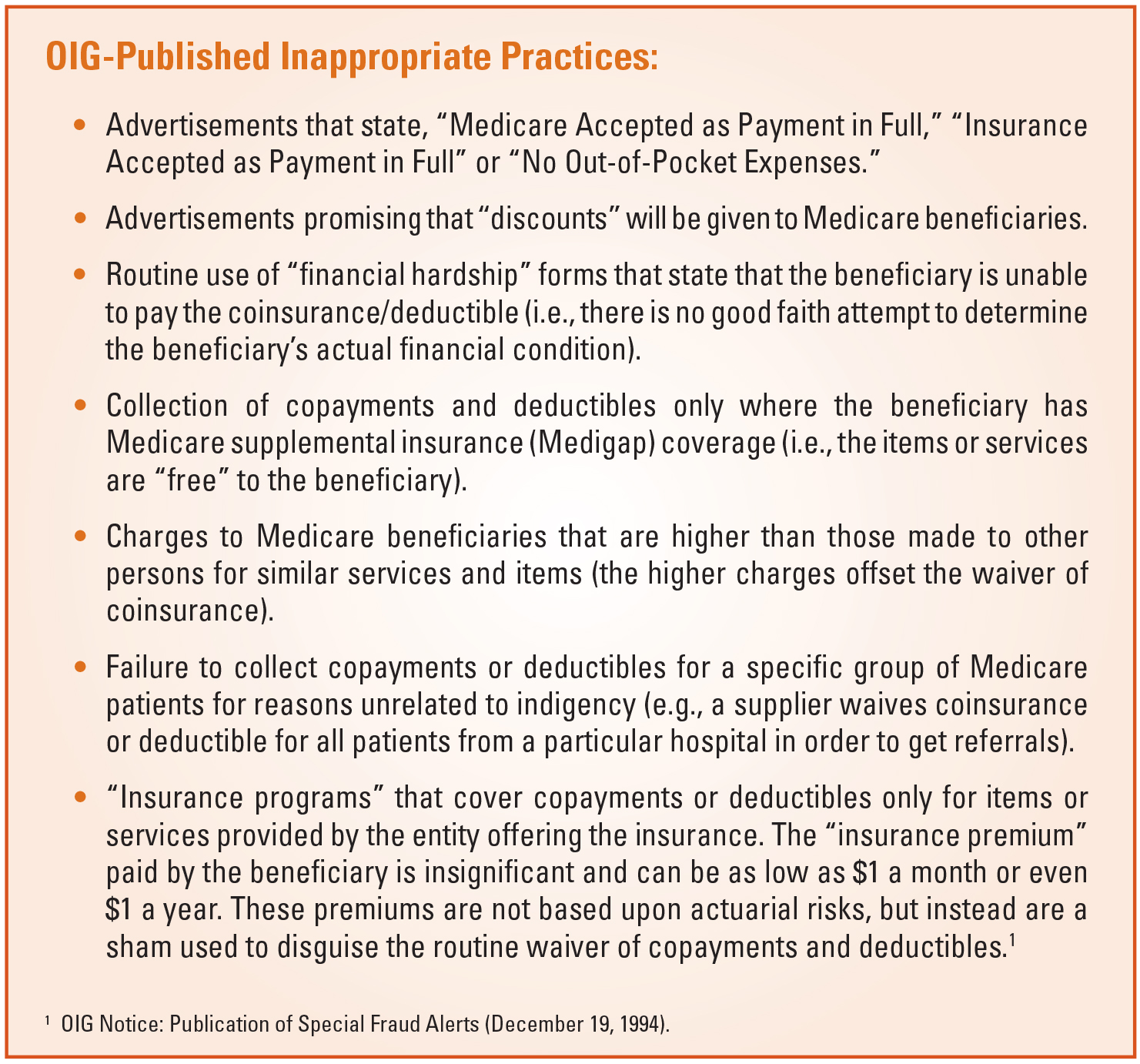

The Office of Inspector General (OIG) has published a Special Advisory Bulletin that addresses many facets of the CMP Law as it pertains to gifts and other inducements to Medicare and Medicaid beneficiaries. For waivers, the OIG has provided exceptions for: “Non-routine, unadvertised waiver of copayments or deductible amounts based on individualized determination of financial need or exhaustion of reasonable collection efforts.”5

A key element to implicating the civil monetary penalties is that the remuneration is likely to influence the beneficiary to order or receive items or services from a particular healthcare provider. No specific intent is required; deliberate ignorance or reckless disregard could trigger the inducement element.

In addition, valuable goods and services offered as part of a marketing or promotional activity is a way specifically recognized by the OIG to qualify as an inducement. The OIG has pointed out that “even if a provider or supplier does not directly advertise or promote the availability of a benefit to beneficiaries, there may be indirect marketing or promotional effects or informal channels of information dissemination, such as ‘word of mouth’ promotion by practitioners or patient support groups.”

The OIG has noted that such waivers occur in a wide variety of circumstances, some of which do not present a significant risk of fraud and abuse. The OIG has encouraged the use of its advisory opinion process to confirm appropriateness of healthcare provider practices.

Federal Anti-Kickback Statute Safe Harbors and Required Intent

The Federal Anti-Kickback Statute is recognized as a broad regulatory framework. Seeing that many reasonable arrangements might implicate the statute, the OIG has periodically issued regulatory “safe harbors” that define business arrangements that would be considered non-abusive to federal healthcare programs. There is a safe harbor for waiver of beneficiary copays, coinsurance and deductibles; however, the safe harbor contemplates specific healthcare providers and suppliers, such as inpatient hospitals, pharmacies and ambulance providers (among others).6 Each provider type has specific elements that must be satisfied for the safe harbor to apply.

Note that all elements of the applicable safe harbor must be satisfied in order for an arrangement to be protected. Business arrangements that do not satisfy all of the requirements of a safe harbor are not per se illegal. Such arrangements are reviewed on a case-by-case basis, in light of all relevant facts and circumstances, and may be deemed by the OIG not to violate the Federal Anti-Kickback Statute.

Note that all elements of the applicable safe harbor must be satisfied in order for an arrangement to be protected. Business arrangements that do not satisfy all of the requirements of a safe harbor are not per se illegal. Such arrangements are reviewed on a case-by-case basis, in light of all relevant facts and circumstances, and may be deemed by the OIG not to violate the Federal Anti-Kickback Statute.

Parties to an arrangement that falls outside the scope of a safe harbor will only violate the Federal Anti-Kickback Statute if they “knowingly” and “willfully” entered into an inappropriate arrangement. An arrangement that is outside the scope of safe harbor protection will be found to be in violation of the Federal Anti-Kickback Statute only if the purpose of the remuneration is to induce referrals or the arrangement or recommendation of the purchase of goods or services covered under a federal healthcare program. Note, however, that the sole purpose of the arrangement does not have to be inappropriate or illegal; the presence of a legitimate purpose will not alone shield a healthcare provider from liability.

To mitigate the risks of enforcement, it is critical to understand if the safe harbor applies based on provider type and what elements must be satisfied to fit squarely within safe harbor protection. This should be determined prior to granting such waivers. If no safe harbor applies, the provider will need to assess the enforcement risks with any waiver practices. Adopting best practices or guidance from government enforcement authorities, such as the OIG, in consultation with regulatory counsel will help to mitigate risks.

Integrity of Rate-Setting Process

In addition to fraud and abuse, the integrity of the rate-setting process remains an important consideration when it comes to healthcare provider waivers. As mentioned above, plans and healthcare providers negotiate rates and fee schedules based on a number of factors: usual and customary charges, utilization data, underwriting, geography and patient populations, to name a few. Systematic or recurring waivers can amount to a healthcare provider’s misrepresentation or manipulation of actual service and procedure costs. Depending on the language in each applicable payer/provider agreement, such practices could be considered inappropriate and result in breach of contract or even a violation of state-specific insurance fraud statutes and regulations. Infrequent or non-routine waivers are far less likely to fall under such scrutiny, especially if granted based on financial need or after good faith efforts to collect due fees, as described above.

What Steps Can Be Taken To Mitigate Fraud And Abuse And Other Risks Associated With Such Waivers?

A number of steps can be taken to help guard against fraud and abuse and other inappropriate waiver practices, such as:

- Develop or update policies and procedures. All waivers should be granted consistent with established policies and procedures. This should include non-customary waiver approvals. Such policies and procedures should be compliant with applicable federal and state law and take into account the healthcare provider’s plan agreements.

- Conduct ongoing employee training. Employee education and training is a critical component of any effective compliance plan. Waiver policies and procedures should be part of the compliance training and education curriculum, as should the underlying legal authority. Special attention should be paid to staff involved in marketing/ business development, patient intake, accounting and billing.

- Periodic, routine reviews and audits. Healthcare providers should conduct periodic internal reviews or audits of waivers and waiver practices to ensure appropriate documentation and compliance with policy and procedure. This should occur at least once per year.

- Maximize use of technology. Technology platforms used for billing and accounting should include checks or prompts to ensure waivers are granted and documented consistent with policy and procedure.

- Engage outside counsel. Outside legal counsel can be engaged to assist in the development of policies and procedures, employee training and ongoing consultation to help providers ensure they are planning, developing and implementing compliant waiver practices.

Irrespective of when a waiver is granted, there are serious ramifications that must be duly considered. If you have questions about any past, current or proposed waiver practices, you should consult experienced healthcare regulatory counsel.

- 42 U.S.C. §1320a-7a.

- 42 U.S.C. §1320a-7b.

- 31 U.S.C. §§3729-3733.

- 42 U.S.C. §1320a-7a(i)(6)(A).

- OIG Special Advisory Bulletin: Offering Gifts and Other Inducements to Beneficiaries (August 30, 2002).

- 42 C.F.R. §1001.952(k).

Frank Carsonie, JD is chair of the Health Care & Life Sciences Practice Group at Benesch, Friedlander, Coplan & Aronoff LLP and a member of the Corporate & Securities Practice Group. He is the Columbus office partner-in-charge as well as a member of the firm’s Executive Committee. Mr. Carsonie’s practice focuses on counseling individuals and entities engaged in the healthcare industry on business transactions and regulatory matters. Mr. Carsonie is also experienced in advising individuals and entities, including public and private for-profit and non-profit companies, on organization, reorganization, mergers and acquisitions, divestitures, strategic alliances and joint ventures, capital financings, including private equity and venture capital funding, corporate governance, negotiation, drafting and enforcement of contracts, and general business counseling. He can be reached at fcarsonie@beneschlaw.com.

Frank Carsonie, JD is chair of the Health Care & Life Sciences Practice Group at Benesch, Friedlander, Coplan & Aronoff LLP and a member of the Corporate & Securities Practice Group. He is the Columbus office partner-in-charge as well as a member of the firm’s Executive Committee. Mr. Carsonie’s practice focuses on counseling individuals and entities engaged in the healthcare industry on business transactions and regulatory matters. Mr. Carsonie is also experienced in advising individuals and entities, including public and private for-profit and non-profit companies, on organization, reorganization, mergers and acquisitions, divestitures, strategic alliances and joint ventures, capital financings, including private equity and venture capital funding, corporate governance, negotiation, drafting and enforcement of contracts, and general business counseling. He can be reached at fcarsonie@beneschlaw.com.

Nathan Sargent, JD is an associate in the Health Care & Life Sciences Practice Group at Benesch, Friedlander, Coplan & Aronoff LLP. Mr. Sargent’s practice is focused on healthcare business transactions and regulatory matters, including mergers, acquisitions, contract drafting, licensure, and Medicare and Medicaid program enrollment and reimbursement. Mr. Sargent also provides counsel on matters involving corporate governance and related best practices. Prior to joining Benesch, Mr. Sargent worked in multiple capacities for a northeast Ohio health system where he maintained responsibilities in board and committee governance and administration as well as physician contracting services. He can be reached at nsargent@beneschlaw.com

Nathan Sargent, JD is an associate in the Health Care & Life Sciences Practice Group at Benesch, Friedlander, Coplan & Aronoff LLP. Mr. Sargent’s practice is focused on healthcare business transactions and regulatory matters, including mergers, acquisitions, contract drafting, licensure, and Medicare and Medicaid program enrollment and reimbursement. Mr. Sargent also provides counsel on matters involving corporate governance and related best practices. Prior to joining Benesch, Mr. Sargent worked in multiple capacities for a northeast Ohio health system where he maintained responsibilities in board and committee governance and administration as well as physician contracting services. He can be reached at nsargent@beneschlaw.com