Deductibles: Impact on the Physician

Arne Pedersen, MBA, FACMPE, Director of Client Services, ABC

Every year, it seems like health care premiums continue to rise along with the deductibles that accompany the latest versions of health care plans. Multitudes of questions abound regarding the size of deductibles, the collections of deductibles, and strategies to address deductibles. These are all good questions to discern. But, are these the only questions to ask? This article seeks to explore the impact of deductibles on physicians.

History

Deductibles have been a part of health care financing in various forms from the beginning of health insurance coverage. Health insurance began as disability insurance covering lost time from work in the 1800s leaving patients to pay for all of their medical bills1. Of course, healthcare was not the large industry that it is today with the plethora of clinical and technological advances we have come to expect. Over time, it has morphed into various other forms. In the last two decades, the trend for deductibles has been quite remarkable. The Kaiser Foundation has conducted several studies regarding types of insurance products (plans), increases in deductibles, and increases of worker’s contribution to health care premiums.

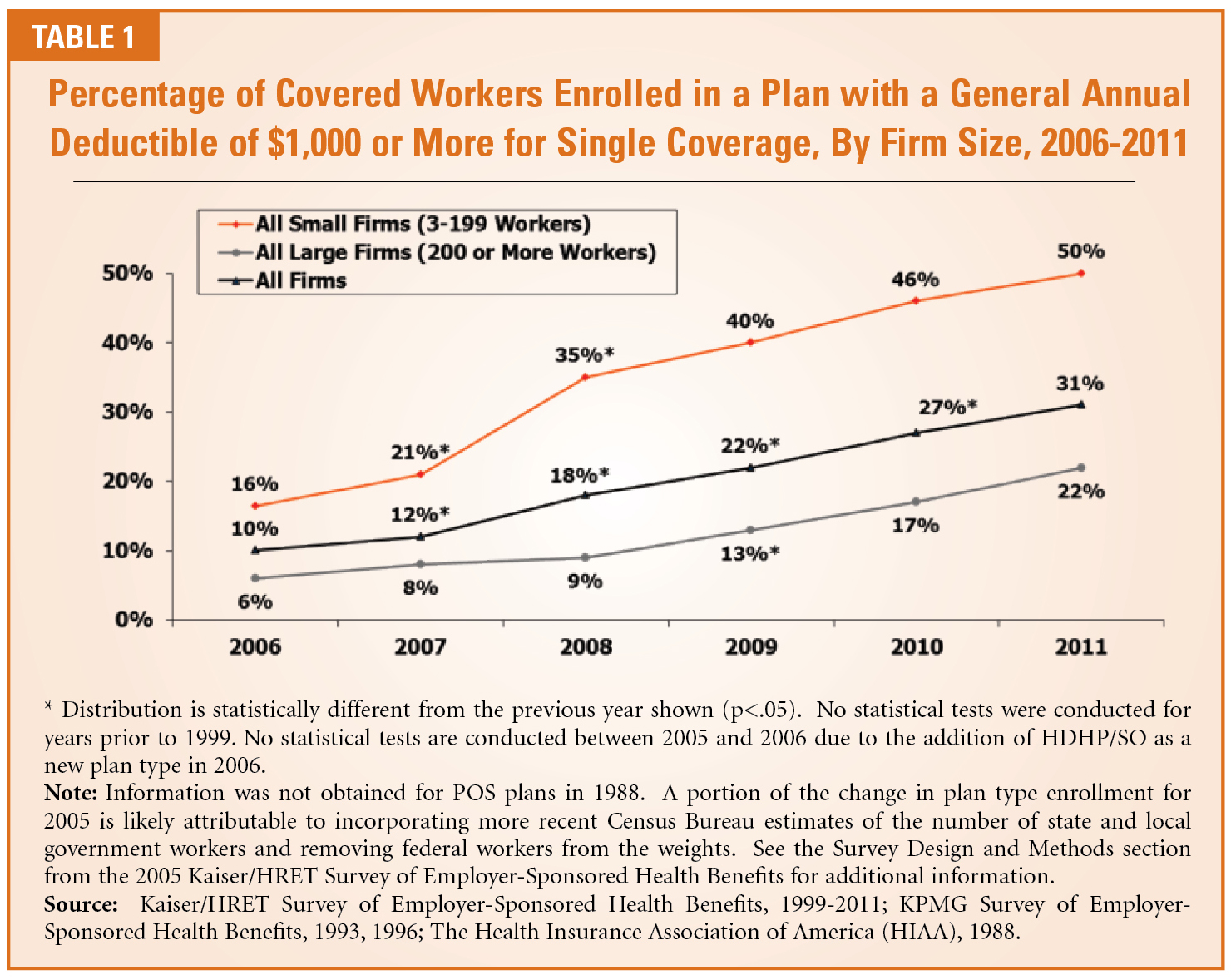

In addressing the various insurance products, it is important to note that this article is going to focus on the standard insurance approach. The difference between full insurance and self-insurance and their respective trends is left for a future article. As an illustration, Table 1 above from the Kaiser Foundationdemonstrates the changes over time with the types of plans in the market and the trends of what employers of all sizes purchase for employees.

The chart begins in 1988, makes a rapid move through the 1990’s, and explores the first decade of the 21st century. There are a few salient points to anchor in the article. The first one is that the PPO plan became very popular over the last decade and a half. The PPO plans include co-pays and deductibles. The deductibles were small when first introduced and have grown with the market since. Another salient point is the introduction of the high deductible health plan in the current product mix. In a trip down memory lane, I rememberworking for Anthem Blue Cross and Blue Shield more than a decade ago when the Consumer Directed Products were being designed and introduced. The idea was to get the consumer (patient) engaged in the cost of healthcare with the goal of lowering healthcare costs.

Health Reimbursement and Health Savings Accounts were introduced to provide employers with options to help employees to take a more active role in the cost of care. The success of these programs is measured by the adoption rate of these products, the increase in the number of workers paying higher deductibles, and, the increase in the number of workers paying a greater share of the healthcare premiums.

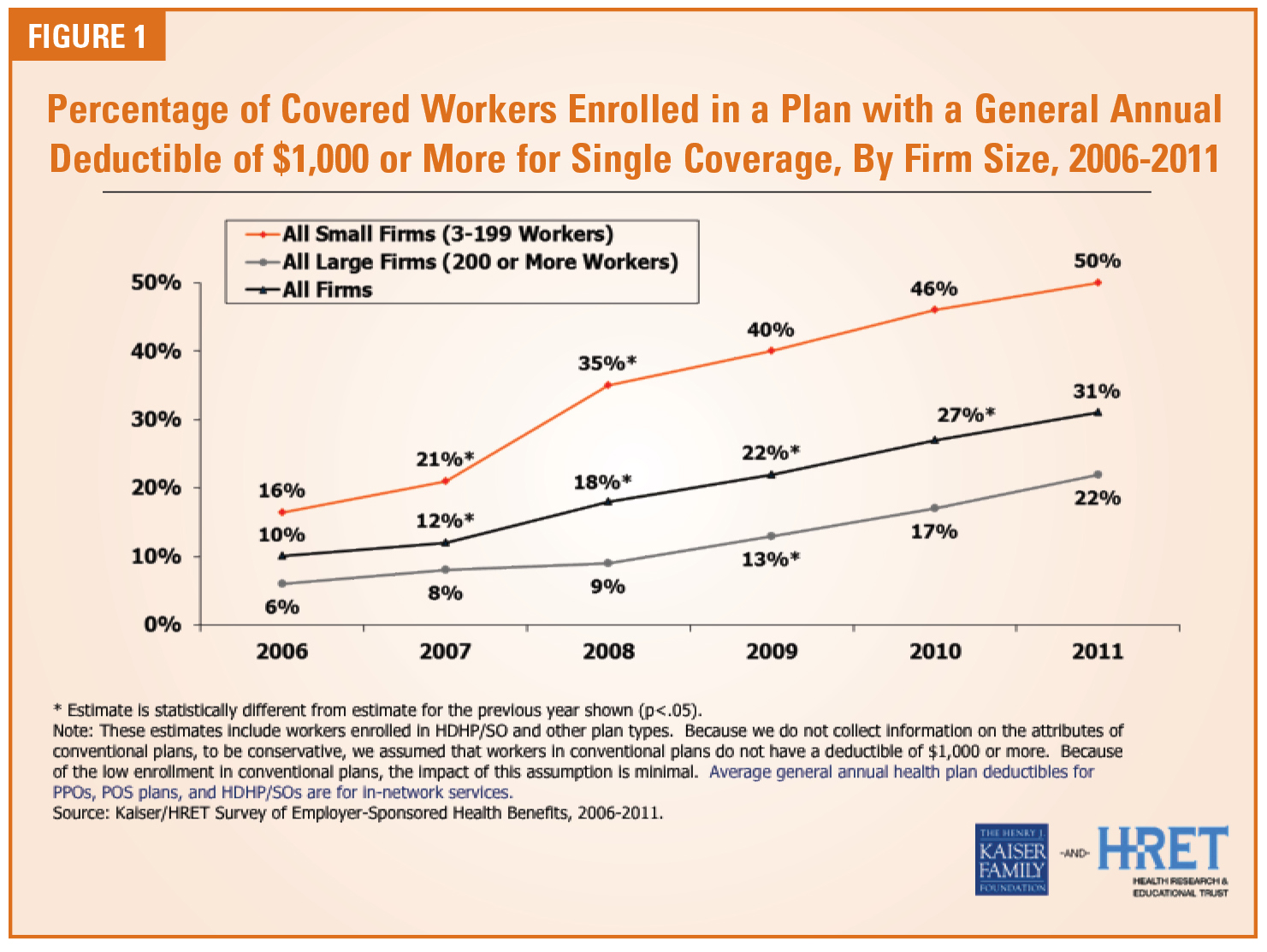

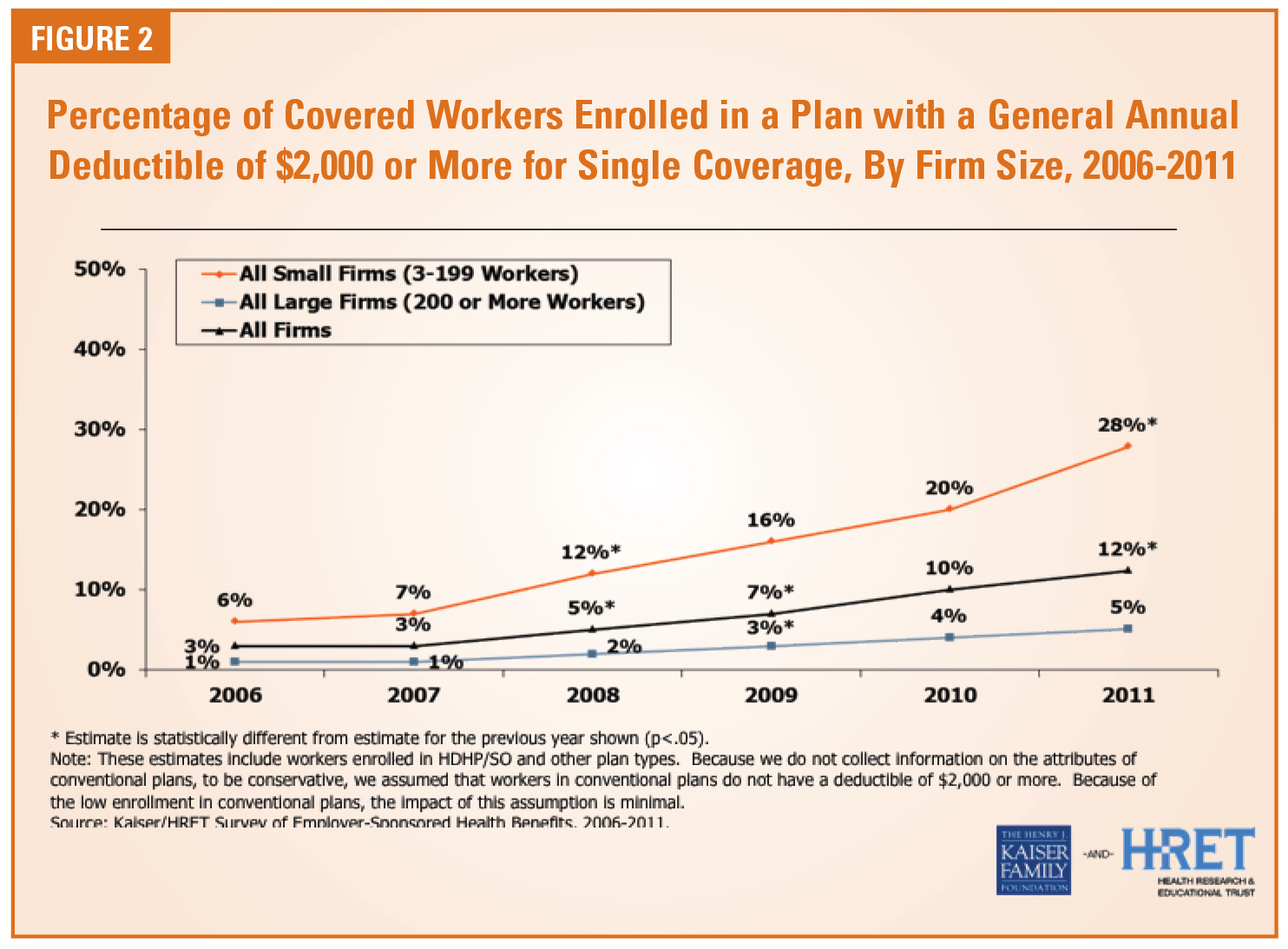

The adoption rate for the HRA and HSA is reflected in the High Deductible Health Plans’ (HDHPs’) growth from four percent in 2006 to 17 percent in 2010. In terms of the expansion of workers paying higher deductibles, the Kaiser Foundation again has some superb research, which is demonstrated above, in Figure 1 and Figure 2.

The keys to these two particular graphs are found in the rising annual deductibles. As stated earlier, the PPOplan is still the most popular plan. That is the reason for these levels of deductibles. The HDHP deductibles tend be much higher on average. The one group in these two graphs that has experienced the highest deductibles is the small firm (3-199 workers). This is important to note primarily because small firms create most of the jobs. Small firms have less leverage to work with in terms of negotiating more favorable healthcare premium rates. Therefore, they tend to choose less expensive plans with larger deductibles.

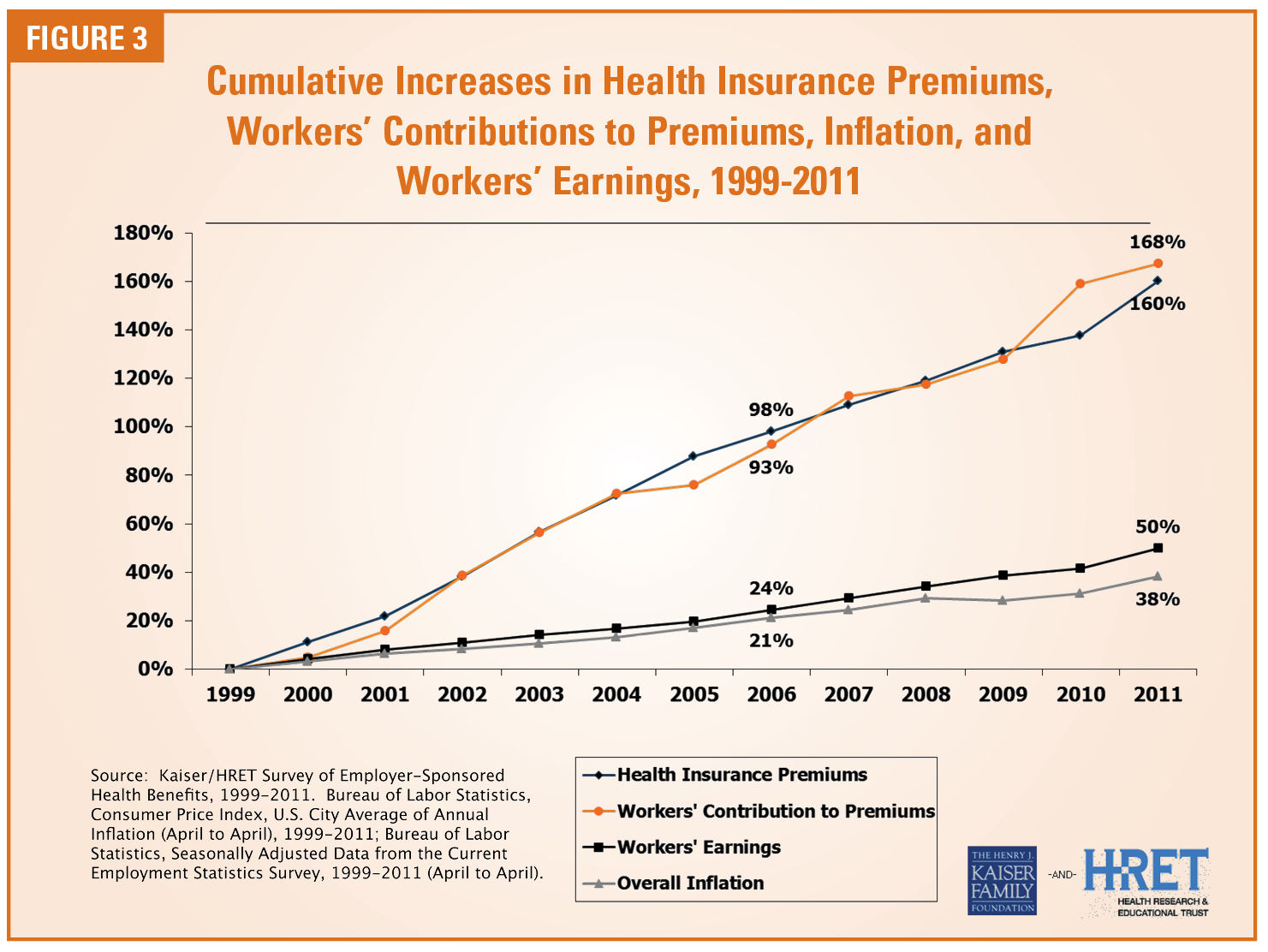

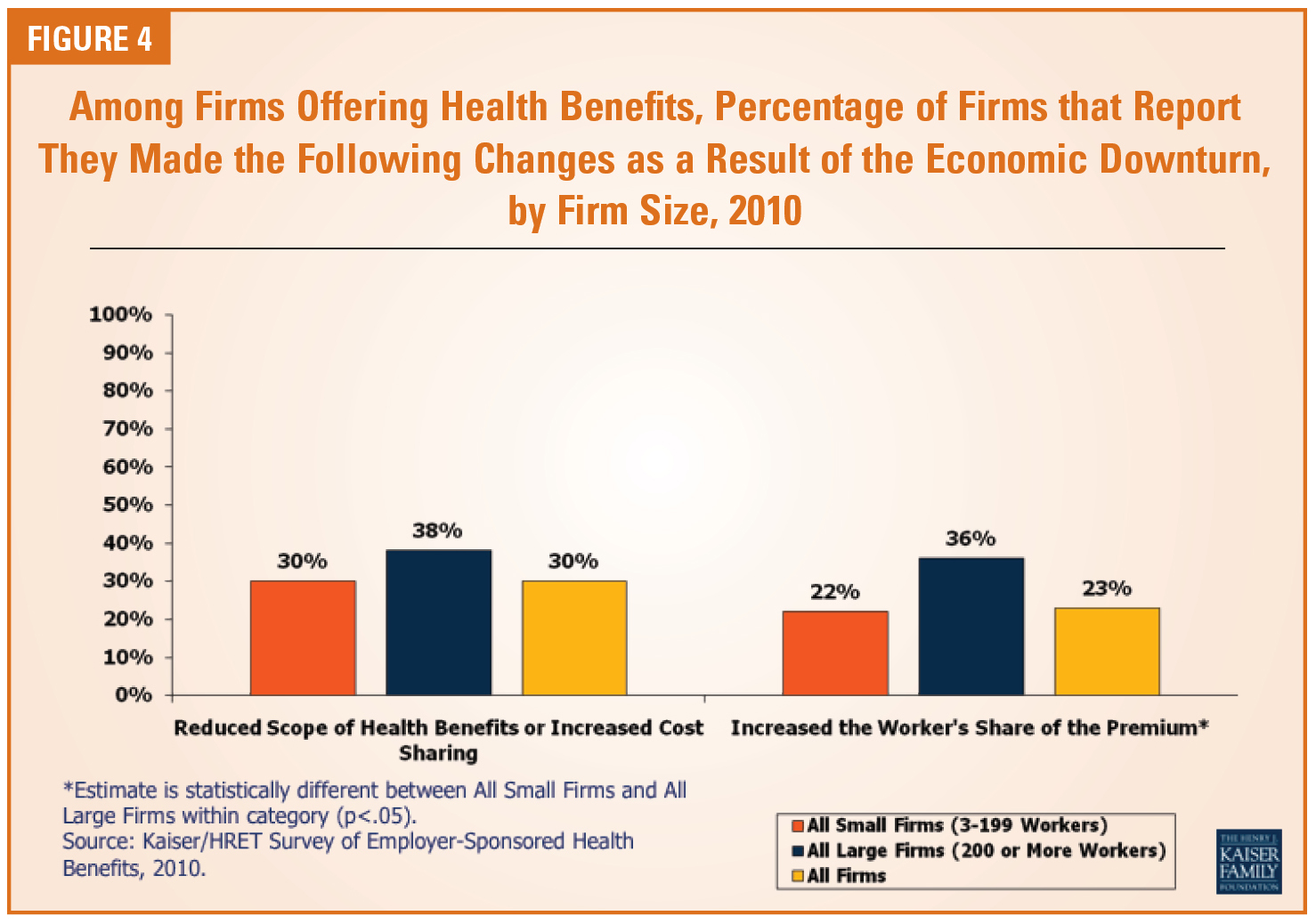

One last point in the history section is the cost shifting of premiums from employers to employees. This phenomenon influences the average employee to carry a higher deductible in their insurance plan. The greater impact is to the employee (consumer) who now must decide how much health insurance they can afford. Figures 3 and 4 on the next page, again from the Kaiser Foundation, show the shift of premium dollars as well as the shift to less comprehensive health insurance plans.

In Figure 3, both the worker’s contribution to premiums and health insurance premiums have seemingly risen in tandem from 1999 through 2011. While this has been happening, the worker’s earnings have risen by much less a margin over the same period. This leaves the American worker far less choice in health insurance plans and potentially leaves a gap between actual needs and coverage.

This stark reality is represented in Figure 4. In this graphical representation, all firms seem to be showing signs of reduced scope of benefits and increased share of the premium cost to the workers. The simple family calculation for healthcare dollars in recent economic times demonstrates the gap between the needs and the ability to pay. The demand is simply outpacing supply in healthcare and is creating an unsustainable situation. Hence, the question of collecting deductibles comes into play.

Collecting Deductibles

When does a patient meet his or her deductible? How much of the deductible does a group have to go after? The complex answers begin with something called a plan design. Health insurance companies have a plethora of plans with multiple designs to meet the needs of the consumers, both employers and individuals. These plans come with a variety of co-pays, deductibles, and co-insurance. To further complicate this matter, the plans also have differences between in-network and out-of-network. These and other factors make billing and collecting deductibles challenging at best.

In office and surgery centers which tend to be more “retail” in nature,physicians and facilities look to collect all or a portion of the deductibles at the point of service. After all, the sooner you get money from the patient, the better. In most cases, this approach does not apply to anesthesia due to the nature of the brief relationship with the patient and because the determination of charges is after the fact. Therefore, the insurance is billed first and after the determination of what the patient still owes on their deductible, the patient is then billed for their portion of the anesthesia service.

Patients will pay in full, make payments, or not pay at all. The first is the ideal, with the second being preferred over the third. The latter two approaches to patient payments can also have an adverse effect on the patient portion of the accounts receivable. This leads to the last point: strategies to address deductibles.

Strategies to Address Deductibles

There is a finite number of strategies for anesthesiologists to address deductibles. They can attempt to collect money up front, provide letters to remind patients of their responsibilities, hold the bills, do nothing, or write the payment off.

Collecting money up front sounds great but needs a practical application. Analysis will help to determine the best approach to executing this strategy. Most importantly, groups should work with their billing partner to determine if this course of action makes sense. If so, they can need help implement the best solution.

Providing letters to remind patients of their responsibilities is reasonable... The effort is not great. The cost is associated with the developing, printing, signing, and copying of these letters to go into patient packets. Of course, groups will need to communicate with their respective facility to have this included into the packet. The word of caution with this strategy is that this is just a reminder letter and is part of a larger patient packet.

Holding bills can be effective. However, it is not for every group. The basic goal is to capture more of the insurance dollars instead of attempting to collect a larger deductible amount from the patient. To achieve this goal, the practice holds its bills while other providers including the facilities are submitting theirs. Their bills will bounce up against the deductible before the practices bill does. This provides the greatest opportunity to collect more from the payor and less from the patient. There are gating factors to consider when reviewing this strategy. It is important to work with your billing partner to determine if this is a viable strategy.

There are times when doing nothing is the right strategy due to timing issues or a lack of a compelling strategy. There are also times when doing nothing is a very dangerous strategy that could produce adverse affects to a group. In the instances when a group is struggling to come to some consensus on a strategy, using a third party to facilitate a discussion makes sense. The third party can provide the fresh perspective to help facilitate an appropriate decision.

Writing off bad debt is never an easy task. The hard part for an anesthesiologist is that every business has bad debts that they must write off. Since the practice is a modified cash-based business, prudent write offs make sense. This alone, though, is not a solid strategy to address deductibles. It will negatively affect the group’s cash flow by itself. Coupled with other strategies, it becomes viable as part of the overall solution.

Ultimately, groups who work with their partners will be able to develop the best set of strategies to address the ever-increasing deductibles.

Arne Pedersen, MBA, FACMPE serves as Director of Client Services for ABC. He is a Fellow of the American College of Medical Practice Executives. His distinguished background includes serving as a former Anesthesia Group Administrator, an expert on leadership, and a Bronze Star Medal recipient from the Persian Gulf War. Mr. Pedersen authored the book, “Lead with Intent” a comprehensive, yet practical leadership bible with a vision of training leaders. Mr. Pedersen serves an adjunct professor at the University of Notre Dame in the Executive Education Certificate Program and teaching Performance Management. He can be reached at Arne.Pedersen@AnesthesiaLLC.com.

1 Fundamentals of Health Insurance: Part A, Health Insurance Association of America, 1997