Why the Cost of Anesthesia Care Matters

Jody Locke, CPC

Vice President of Anesthesia and Pain Management, ABC

Have you heard about or seen the Hospital Corporation of America (HCA) white paper, ‘How to control the rising cost of anesthesia care’? Having spent over $96 Million in anesthesia subsidies last year alone, HCA has gone on the offensive by arming its legions of hospital CEOs with not only a logical framework for cost management but a team of anesthesia contract specialists whose job it is to carefully assess the economics of every anesthesia contract before it is renewed. The primary focus of the team is to assess the reasonableness of each private group’s request for support and the compensation they believe they are entitled to. Almost as important is the analysis of the hospital’s coverage requirements. More often than not, the review process results in resetting expectations for both anesthesia provider compensation and the CEO’s expectations of unrealistic staffing and call. It is unclear exactly how the other hospital networks will follow suit, but one thing is absolutely certain; renegotiating an anesthesia service contract is no longer what it once was. Maintaining the financial viability of the practice is not a simple matter of drawing a line in the sand any more.

There is no question that the most significant factor in the cost calculation is compensation. Every request for financial support starts with an estimate of what the providers should be paid for the services they provide. Ever since the publication of the Abt Report in 1994 anesthesia compensation requirements have tended to be based on national perceptions of comparability. Given a national manpower shortage, most anesthesiologists and CRNAs believed they were entitled to the same compensation they could get elsewhere. The result was a substantial increase in overall compensation levels across the country. According to MGMA surveys the average physician compensation increased by 10% from 2005 to 2006 alone (based on 2004 and 2005 survey data). It stands to reason that the source of this additional compensation was primarily the result of hospital subsidies and not better contract rates with payors or a wholesale improvement in collection performance by billing companies and private anesthesia office staff.

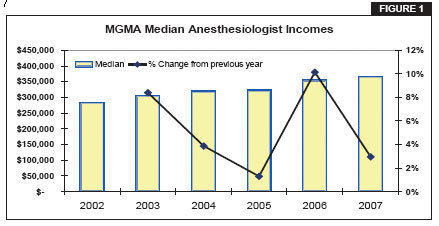

It should not surprise any reasonable observer of the anesthesia marketplace that a sharp spike in income and income expectations will trigger a reaction. Since anesthesiology groups are using the MGMA survey data as the basis of their requests for more support, hospital CFOs are starting to question the numbers with ever more care. Inevitably the survey data is proving to be as much of an obstacle as an argument for anesthesia requests for subsidies. The reason is simple; the tide has turned. With an increase in the supply of qualified providers, hospitals are beginning to look more at their own bottom line than the possibility of losing their anesthesia groups. To some this shift is perceived as counter-intuitive. In an effort to control costs long-term, a growing number of hospital CEOs are revealing that they are willing to pay considerably more in the short term to change anesthesia groups even if it means relying on locums for a period of time. The message seems to be that hospitals are growing restive and considerably less willing to give in to requests for financial support that will continue to increase anesthesia provider compensation in the face of declining overall hospital profits. They must be on to something, because anesthesia practices seem to be backing down and accepting what they are being offered with increasing frequency. The evidence of this change in attitudes is both empirical and statistical. The most recent MGMA compensation survey shows only a nominal increase (3%) in median compensation from the previous year (see Figure 1).

There is a lesson in this for the specialty as a whole. Just as businesses must constantly find ways to manage their cost of doing business to remain profitable, so must anesthesia group managers and administrators find ways of maintaining their own competitive advantage in an increasingly competitive market. While it is true that some businesses have more options than others – banks did away with tellers and airlines did away with food – no business or specialty is immune from the need to be as efficient and effective in the delivery of services as possible. The days of supplier-induced demand have long since disappeared. Every anesthesia group that gets financial support from its hospital today would do well to develop alternative strategies in anticipation of the elimination of that support.

Unfortunately, traditional cost management strategies only go so far in the delivery of anesthesia services. A group practice can increase its deductible for healthcare, shop around for cheaper malpractice or renegotiate its contract for billing services, but none of these ultimately has as significant an impact on the cost of service as the number of staff required to provide the service.

Fortunately, anesthesiology has some strategic options not as readily available to other medical specialties. The most obvious of these is the potential to leverage more expensive physician time with less expensive CRNA time. Just as high-priced lawyers rely on junior lawyers and paralegal assistants to perform the less demanding aspects of their job, so too have anesthesiologists in most parts of the country, except the far west, perfected the medical direction model. The fact is that it is virtually impossible for a physician-only practice to compete on price with a careteam practice without lowering the compensation expectations of the anesthesiologists. In addition, we all know that the best possible situation for an anesthesiologist is to work with hospital-employed CRNAs. To a large extent this explains deltas in average compensation between the west and the rest of the country.

There is no question that a careteam approach to the administration of anesthesia services will maximize the income of the physicians so long as there is a reasonable differential in the total compensation package between the anesthesiologist and the nurse. Conventional wisdom suggests that if the total physician compensation package is 2.5 times that of the CRNA there will be a slight cost advantage at an average medical direction ratio of 1 physician to 2 nurses and a material cost advantage at an average medical direction of 1:3. In other words, there is no question that the more leveraged a practice is, the more cost effective the delivery of service. As we all know, though, cost is not the only factor in determining the configuration of the careteam. More often than not, historical, philosophical, and practical considerations involving the availability and cost of CRNAs will also play a significant role in any consideration of modification to an existing model.

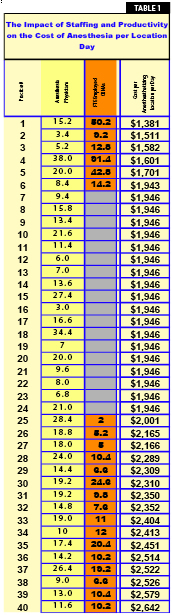

The data in Table 1 were developed to objectively assess the impact of staffing models and provider productivity on the overall cost of anesthesia care. The data are based on a sampling of ABC client data for 40 practices, carefully reviewed and compiled for this purpose. These are all private anesthesia practices, which have been with the company for at least year. They represent clients all across the country with consistent books of business, i.e. none is in a ramp-up mode for any of its main facilities. FTE staffing levels were based on a standard metric of days worked and assumed that an FTE physician or CRNA would take 6 weeks of vacation. The significant disparity in the cost per day of coverage for an anesthesthetizing location is the result of both productivity and coverage requirements, which will be discussed in more detail below.

On the one hand, the data raise a very interesting question: how can the cost of covering one anesthetizing location for a day be so much higher in one location than another? The short answer is because it can be. In other words, there is sufficient revenue, either from fee-for-service collections or from a combination of fee-for-service collections and hospital support to justify such a cost structure. On the other hand, the data clearly indicate just how much the cost can be reduced if it must. Ironically, what the data also demonstrate is that the careteam does not always result in lower costs if the nurses are not managed in an economically advantageous or significantly leveraged mode.

It is worth noting here that it is not uncommon for subsidy discussions to focus on an average cost per location day of $1,950, which is the cost of a physician providing coverage alone. This is approximately what results if the total cost of an anesthesiologist is $430,000 (W2 income, benefits, malpractice and overhead) and is divided by 221 days (365 days minus 108 weekend days, 6 holidays and 30 days of vacation).

Clearly the careteam is no panacea, nor a guarantee of above average physician compensation. For all the advantages of economic leverage, if the practice does not generate adequate revenue from professional service collections it doesn’t matter how carefully the pie is divided. There can also be significant offsetting considerations to the careteam model including decreased provider productivity, management costs, and provider availability and turn-over in staff. There is a prevailing belief in the Western states that the inclusion of CRNAs in the delivery model is not a desirable option. The more a practice limits its options, the more it becomes an effect of, rather than in control of its circumstances.

Given all these issues, considerations, and limitations how can a practice stay competitive and remain financially viable without increased financial support from the hospital? Some might suggest the solution requires thinking outside the box regarding historical perceptions of the role of the anesthesia department in the management of the operating room. In short, if the anesthesia practice cannot increase its revenue through more effective collections or reduce its costs materially then it must look at ways to manage the number of staff necessary to provide the service. The most cost effective practice represented in Table 1 is also the practice that has been most effective in two areas of practice management: maximizing the leverage of the careteam and minimizing the impact of scope creep in hospital coverage requirements.

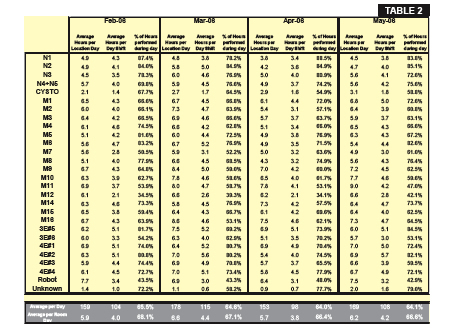

As the head of the group would be quick to add, though, the pressure to add locations and give in to scope creep is never ending. His approach is simple. Armed with monthly updates of actual O.R. utilization he is constantly educating administration and pushing back on requests for new venues. His own private benchmark is 45 ASA units per location day (see Table 2 on page 6); if he cannot see this as a reasonable average level of productivity he will not accede to expanding coverage.

Obviously this is an approach that requires considerable focus and discipline, but it is clearly one that has paid off handsomely for the group. Not only does the practice get no financial support from the hospital, but physician compensation levels are above average. It is hard to argue that this is not one of those best practices that could benefit most other anesthesia groups across the country.

Every anesthesia practices’ situation is unique. It would be naive to think that a given strategy or plan that works well in one hospital in one part of the country would have the same results elsewhere. This is not the point. Every practice must assess and address the unique factors that determine provider costs, and be willing to analyze and address them. More often than not the result will be a difference of degree rather than of kind, but sometimes it is that 10% extra that will make the difference between success and failure, between the ability to recruit and retain the best providers and an inability to do so, between the perception that the anesthesia practice is part of the solution versus part of the problem, and, ultimately, between the ability to demonstrate to the administration that the group can manage itself effectively versus needing to be taken over by the hospital or some other entity.

In the ever changing dynamic of anesthesia relations with hospital administrators there is a lot at stake. Many victories are Pyrrhic. The value of success does not always seem to justify the cost of the battle. There is a tendency to give in or, worse yet, give up in the face of today’s changing economic realities. Just as there is almost always a solution to an inscrutable clinical challenge, so too, there is virtually always a solution to a seemingly intractable economic problem so long as there is sufficient commitment to a positive outcome and a persistent willingness to creativity and innovation. What anesthesiologists and CRNAs should always remember is that every hospital needs anesthesia services to run its operating rooms. There is always a way to make the numbers work. The choice is simple: be part of the problem or part of the solution. The necessary tools and resources are more available to the typical anesthesia practice than most anesthesiologists are willing to admit. The question is when and how they want to take advantage of them.