Endoscopy : Revisited

Jody Locke, CPC

Vice President of Anesthesia and Pain Management Services, ABC

Just mention endoscopy at an anesthesia conference and see what happens. Few topics elicit such strong but disparate responses. For the anesthesiologist from the East endoscopy has been, and continues to be, his or her fastest growing and most profitable line of business. By contrast, the prevailing view of the physician in the West reflects a very high degree of skepticism. His experience is that the endoscopists don’t really want to work with his group. He interprets payer policy as forcing anesthesia through the same funnel of denial as other services and sees no meaningful light at the end of the tunnel, especially with regard to endoscopy. Such is the challenge to today’s anesthesia practice management: sorting out the realities of facility expectations, surgeon preferences, payer policies and economic realities and, most of all, rising above the prejudice of emotions. Cynicism and the weight of disappointment too often cloud our ability to make effective management decisions. While the specialty of anesthesia is at a particularly challenging crossroads, many are finding opportunity by reassessing previous assumptions and digging deeper into the analysis of customer expectations and market trends. To this end a review of endoscopy is a particularly fertile field for investigation.

These are five questions that should serve to frame the discussion.

- How does payment to anesthesia providers for endoscopic procedures fit into the broader national debate about the future of healthcare?

- Why is there such variability in practice patterns across the country as pertains to the role of endoscopy?

- What do we actually know about payer policies concerning payment to anesthesia providers for CPT® codes 00740 and 00810?

- What is an effective management strategy?

- What conclusions can we draw based on what we currently know about the value of endoscopy as a line of business?

The following is a review of actual data for 26 ABC client anesthesia practices, 13 in the Eastern United States and 13 in Western states over a three year period. Western states include Arizona, California, Idaho, Oregon and Washington. Eastern clients are located in Delaware, Florida, Georgia, Illinois, Ohio, New Jersey, New York, Pennsylvania and Virginia. These are all moderate to large practices that have been ABC clients since 2011; 24 of the practices have been clients since well before 2011. In two cases the clients joined ABC during the year and so their data for 2011 have been annualized to reflect historical production levels.

For purposes of this analysis all claims billed with CPT codes 00740 (upper G.I.) and 00810 (lower G.I.) were pulled for all 12 months of 2011, 2012 and the first six months of 2013, except as noted above. Charges and payments were tallied based on Date of Service. This represented 83,158 claims in 2011, 100,927 claims in 2012 and 51,072 claims for 2013, which would annualize to approximately 102,144 cases for 2013 if volumes continued at previous levels. igure 1 indicates the total percentage of anesthesia revenue derived from endoscopy claims by year and region of the country for the practices included in the study.

Endoscopy for Anesthesia and the National Healthcare Debate

The future of payment for anesthesia services for endoscopic procedure will ultimately be determined by a variety of factors: political, clinical and economic. As is so often the case in politics, philosophical principles and policy agendas may have more to do with the practical reality of clinicians in the field than clinical relevance or economic realities. Endoscopy is a case in point. If one assumes that it is desirable for all Americans over the age of 50 to get routine colorectal screening, then an argument can be made for the value of making the procedure as painless as possible. Here the economic policy argument hinges on the expectations that spending a little more on anesthesia to ensure that a higher percentage of patients is screened costs less than the alternative in which there is less screening and more colorectal surgery.

Inevitably, the specific realities underlying such broad policy determinations are far more complicated, but such assumptions do often drive public and private payer policy decisions. Apparently, this underlay the interplay between Aetna and United Healthcare a few years ago. Aetna decided to deny claims for anesthesia for ASA physical status I and II patients undergoing routine colonoscopy procedures. In response United Healthcare reaffirmed its policy of paying for such services. Ultimately, Aetna backed off and both payers now generally cover anesthesia for endoscopy. In fact, their rates are some of the best in the industry. How much insight this provides into the inner workings of other payers is hard to tell. The fact is that for years the pessimists have been arguing that the end of reimbursement for endoscopic anesthesia services is imminent and yet, the payments continue unabated, or so it would appear.

Clinical realities in medicine are also subject to their own arcane evolution. The debate as to what categories of providers are sufficiently qualified to administer propofol continues at many levels. Thus far propofol is the agent of choice for GI procedures and anesthesia providers are uniquely qualified to manage the risks of its use but this too could change. The fascinating thing about the specialty is its ability to develop new ways to manage patients through the trauma of surgery with less risk and fewer complications. It is not unreasonable to assume that some new agent or technology will similarly transform the care of endoscopic patients.

Is it true that all such policy decisions are ultimately resolved based on economics? It is not always clear that this is the case. Or maybe it is a matter of how one defines the economics of the issue. The evidence is that in medicine it is not always the cheapest option that wins out. Despite a concerned focus on the cost of healthcare, costs continue to rise faster than for any other sector of the economy. Businesses are continually striving to provide more service for less cost and to push their operations to ever higher levels of productivity and while we hear the same hope for healthcare, the reality does not bear this out.

What appears to happen in healthcare is that the public or policy makers decide on priorities irrespective of the economic implications and then the task that falls to providers is to implement the policies. Today’s public debate about healthcare turns on whether it is a privilege or a right. Those that argue that it is a right seem to be gaining ground, especially with the recent changes introduced by the Affordable Care Act. How this general perception will play out in the specific domain of endoscopic care is hard to predict but clearly anesthesia has become a significant stakeholder in the debate. Curiously enough, while it used to be that the cost of anesthesia was 20 to 25 percent of the cost of the surgery, when it comes to endoscopic care anesthesia payments are roughly equal to those of the endoscopists. This fact alone speaks volumes with regard to the public perception of anesthesia and is consistent with the view that two factors have driven most advancement in healthcare: antibiotics and anesthesia.

Diverse Practice Patterns Across the Country

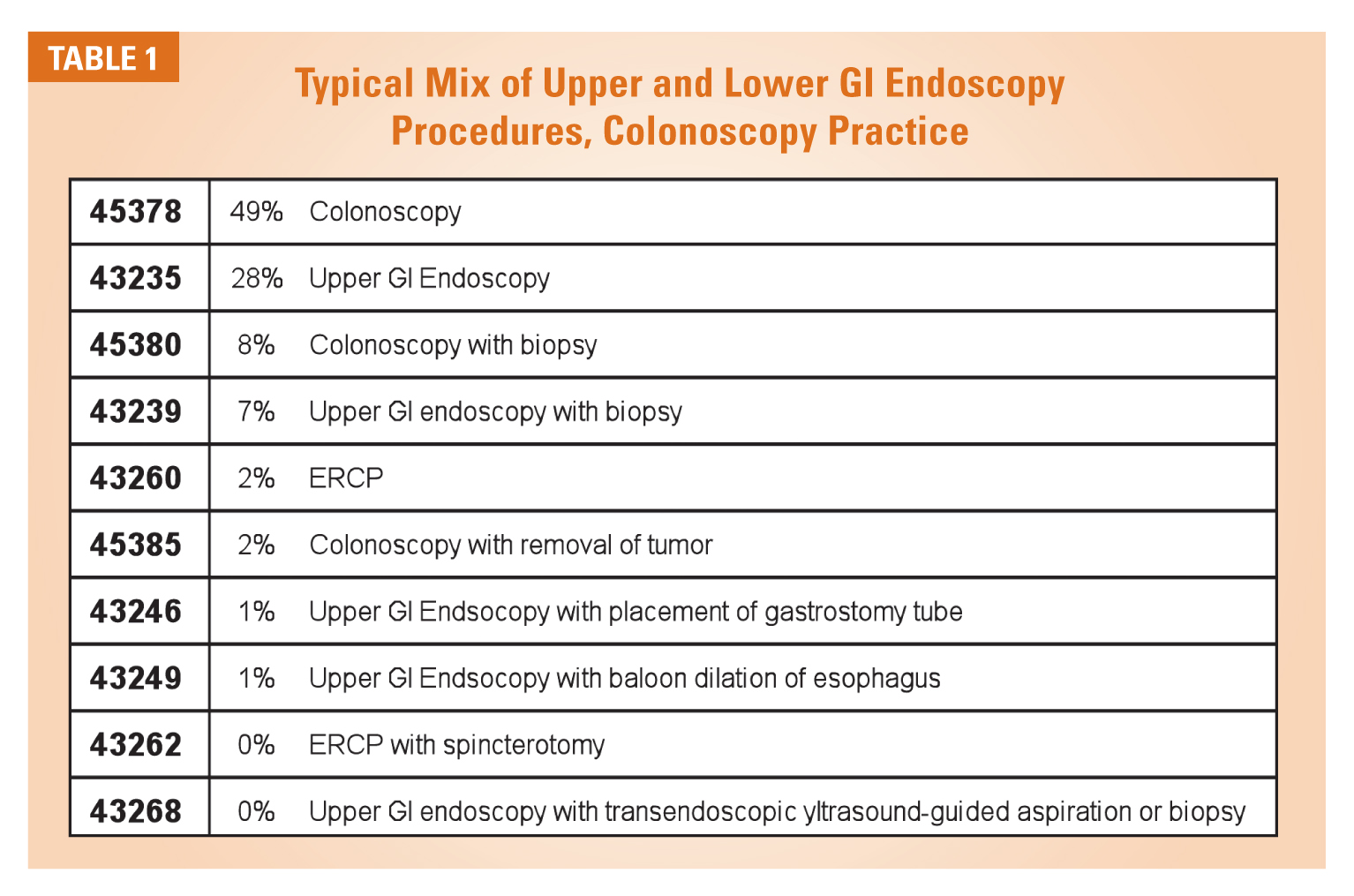

It is important to note that from a claims processing perspective, endoscopy poses a very specific coding and billing challenge. Claims are typically processed based on one of two CPT codes: 00740 for upper GI procedures and 00810 for lower GI procedures. We tend to associate these codes with diagnostic and screening services, but this is not always the case. Table 1 indicates a typical mix of services that may fall under the heading of endoscopy for a practice that focuses on colonoscopy. (Under the ASA CROSSWALK®, a wide variety of surgical procedures all fall under one rather generic category.)

A useful predictor of a dedicated endoscopy practice, however, is the percentage of colonoscopies performed. Herein lies the most obvious factor differentiating practices across the country. Figure 2 compares the impact of colonoscopy on the various practices included in the study. As indicated, even the practice with the highest percentage of colonoscopy cases is under 50 percent. There is an interesting strategic issue raised by this mix. Some will claim that the real growth and revenue potential lies in capturing the colonoscopy business because these are short cases involving healthy patients with potential a favorable payer mix. Others will look at these practices with a particularly high percentage of colonoscopy cases and see this as a point of vulnerability. This is the kind of tricky strategic challenge that anesthesia practices must sort out.

The site of service is another significant factor in understanding the nature and extent of a practice’s commitment to endoscopy. For reasons that are not entirely clear or logical, a higher percentage of endoscopy centers in the East encourage the participation of anesthesia practices in the management of their patients. Such situations make it easy to determine the profitability of the commitment in that all of the key variables for analysis, volume, payer mix and utilization are easily isolated and defined. However profitable such arrangements may be, they pose some special challenges to an anesthesia practice, namely, if the arrangement is too profitable, then the center may be interested in or exploring ways to retain a portion of the anesthesia revenue itself. There has been considerable debate in recent months about corporate models that attempt to co-opt the role of the anesthesia practice.

While endoscopy centers continue to be built across the country, these venues are still the exception rather than the rule for the typical anesthesia practice. The ideal setting involves the dedication of one or two rooms in an ambulatory surgery center or outpatient facility specifically for the provision of endoscopic procedures. Such arrangements typically prove to be the most profitable for three reasons: consistent volume of cases, quick turn-over and favorable payer mix. From a business perspective, a service line can best be assessed when all the variables such as staffing and revenue are clearly identified and logically integrated. This is what cost accounting attempts to do and its role in anesthesia practice management is becoming ever more relevant. The most complicated situations to analyze are those where endoscopic cases are mixed in with the rest of the surgical schedule.

One other question is often asked about the profitability of endoscopy. What is the impact of the anesthesia care team? In theory, the use of CRNAs allows a practice to reduce its cost of providing care, a fact that should make it possible for a practice to be more competitive. The fact that the anesthesia care team is more prevalent in the East than the West may explain part of the regional disparity but cannot be the whole story. Some notable practices in California have significant stakes in endoscopy centers with a physician-only model. The real issue, however, is that the care team only reduces costs when a physician’s salary and expenses can be leveraged over multiple rooms. Typically endoscopy suites only consist of one or two rooms and so the opportunity for leverage is limited.

What is the ideal arrangement for the anesthesia practice and when is endoscopy care most profitable? Quite simply, it is any situation where the net financial yield per clinical day of service equals or exceeds that of the other venues covered by the practice. The two most important metrics to monitor are average cases per day and average yield per case. These are the foundation for any financial serious analysis and should be integral to any practice’s ongoing review of its endoscopic activity. Table 2 below lays out the elements of such a review. While this might be an extreme example it is based on actual data. The real point, though, is that even with a lower yield per case it is the productivity of the facility that makes the arrangement so favorable, no matter what the staffing model. This is the aspect of endoscopy that makes it so favorable for anesthesia practices. The keys to success are efficiency of the facility and productivity of each anesthetizing location.

More important, however, the ideal arrangement is the one where the endoscopists believe that the anesthesia providers will enhance their productivity and profitability. It is on this point that there appears to be the greatest disparity of perceptions across the country. Some centers and endoscopists are simply more willing to partner with their anesthesia colleagues than others. Those anesthesia practices that have been particularly successful in growing their endoscopy business claim this is little more than an educational and marketing challenge.

The Impact of Payer Policies

The impact of payer mix cannot be overstated; even a slight increase in the percentage of Medicare patients can dramatically reduce the average yield per case. Of even greater concern, however, is the ability of payers to change their policies such that payments that were once the norm become the exception, or where the cost and time associated with managing denials and the need to justify the medical necessity of the service makes the cost of the service prohibitive. Such changes can completely invalidate the best laid plans and the most careful business planning. Such unilateral payer policy decisions are especially noxious in that they are completely beyond the control of the practice. Historically, and despite the common perception of many providers, payer policies have not been an unreasonable impediment to most anesthesia practices in endoscopy. Clearly, though, the fear is that this could change dramatically and very quickly.

Table 3 summarizes average actual payments per case for the practices in this study. Not surprisingly, the Medicare average payment per case is about 38 percent of the average Preferred Provider Organization (PPO) #1 plan rate with the Medicaid rate being even lower than this. Overall about 34 percent of all cases billed in 2013 were billed to either a traditional or a managed Medicare plan but some practices saw more than 45 percent Medicare patients, which has a material impact on the potential yield per case.

Based on the data collected for the practices in this study over a three year period, the overall yield per endoscopic case has remained reasonably constant across the country. There is a slight drop from 2012 to 2013 but further review would be required to determine if this was simply the result of payer mix changes or actual declines in payment per case. Medicare rates have increased slightly as have those for most PPO and managed care plans. Those on the front lines of accounts receivable management complain that there are more denials and that it is getting harder to get paid, but based on the results this is more of an operational challenge than a change in economic reality. Aggressive accounts receivable management is an important factor in the success of any practice and the impact of payer inconsistency in the adjudication of anesthesia claims for endoscopic care is more typical than exceptional.

Given the nature of the service, though, these rates will still result in a competitive average daily yield if the facility is well managed and productive.

Given the nature of the service, though, these rates will still result in a competitive average daily yield if the facility is well managed and productive.

In general, the conclusion one might draw from these data is that it continues to be business as usual for endoscopy. Not indicated here is the fact that only two of the practices realized an increase in their net yield per case, while 12 saw a decrease of anywhere from 5 to 28 percent. The rest have been collecting just about exactly what they were collecting in 2012. As is so often the case, we should not be too quick to generalize based on limited data. Each practice and each line of business needs to be assessed individually to draw any meaningful conclusions about underlying patterns or trends.

Given this generally favorable scorecard, then, where is the basis for concern with regard to the future of reimbursement for these services? It is being driven by the payers and it pertains to the issue of medical necessity. Endoscopy has been a subject of special concern to CMS and others for many years because such a high percentage of cases are billed as Monitored Anesthesia Care (MAC) cases. A MAC case must be specifically flagged on the claim form with a –QS modifier. This is not intended to result in a reduction in payment, but, depending on the payer, has the potential to increase the likelihood of a denial or request for additional information. Many Medicare intermediaries also require a separate diagnosis to justify the payment to the anesthesia provider. There is a long tradition of compliance audits following changes in payment patterns, and anesthesia for endoscopy is no exception. With increased utilization comes tighter policies in an attempt to manage the payer’s exposure.

An Anthem-Blue Shield policy that became effective July 2013 is a case in point. Of particular note is the following statement: “The routine assistance of an anesthesiologist or Certified Registered Nurse Anesthetist (CRNA) for individuals not meeting the [criteria listed in the policy] who are undergoing gastrointestinal endoscopic procedures is considered not medically necessary.” The list of criteria for medical necessity describes a common list of risk factors for either undergoing anesthesia or a surgical procedure. Such policies open the door to closer scrutiny of endoscopy claims and are sure to lead to higher denial rates over time. It is because of such policies that many practices in California will not provide anesthesia to ASA I and II patients. It is also why they tend to be so diligent in confirming documentation of medical necessity for the anesthesia provider’s service in anticipation of a request for additional documentation.

At the heart of the matter is the ultimate payer litmus test for payment justification: medical necessity. Unfortunately medical necessity is often in the eye of the beholder and subject to its own arcane algorithm of application. What makes a service medically necessary is not an easy question to answer. If a patient has an infected appendix that threatens to contaminate the perineal space we assume that it is medically necessary to remove it because the procedure will restore the patient’s health and avoid other complications. Does the same logic apply to the 94 year old patient undergoing coronary artery bypass surgery or the 50 year old executive who is reluctant to submit to a colonoscopy with moderate sedation only because it is an uncomfortable procedure? Payers are attempting to define medical necessity by defining the necessary diagnostic preconditions for a service but this is where the process starts to break down. Maybe the implementation of a new, more specific diagnostic code set, ICD-10, will make these determinations more rational, but maybe not. Ultimately an individual must still make a subjective assessment of the value of the service and herein lies the ongoing uncertainty of medical necessity.

The administration of anesthesia to healthy patients for routine endoscopic screening is a clear point of vulnerability and should be monitored closely. This is, in part, why it is so important to track endoscopic volume at the CPT level, but also why diagnosis is so important. The use of “V” codes for diagnostic screening has been a point of particular vulnerability in the current diagnosis coding sequence called ICD-9, and is likely to be even more so once ICD-10 is implemented next October. Payers use two codes to adjudicate claims: the CPT surgical or anesthesia service code and the diagnosis code. It is only by monitoring the impact of particular combinations of these codes that a practice can monitor and gain insight into payer claims’ adjudication policies. This is why there is such concern about what are referred to as “Black Box edits.” Practices that try to anticipate payer edits by picking payable diagnoses should be very careful for such practices will ultimately incur a higher level of risk for an audit.

An Effective Management Strategy for Endoscopy

No one can predict the future of reimbursement for endoscopy with certainty. No crystal ball is that powerful. The best we can hope for is to monitor patterns of payer behavior and policy changes and infer the implications. Thus far the pessimists have been proven wrong, but maybe their day will come. Those who chose not to participate have clearly missed a potentially valuable line of business. The big winners have been those practices, primarily in the Northeast, that have aggressively pursued contracts at endoscopy centers and that have been fortunate to have very productive endoscopy suites in their hospitals. Hindsight is 20/20 but what should we be monitoring as the market evolves? Where are the particular risk areas? What is the best way to ensure that today’s silk purse does not suddenly become tomorrow’s sow’s ear?

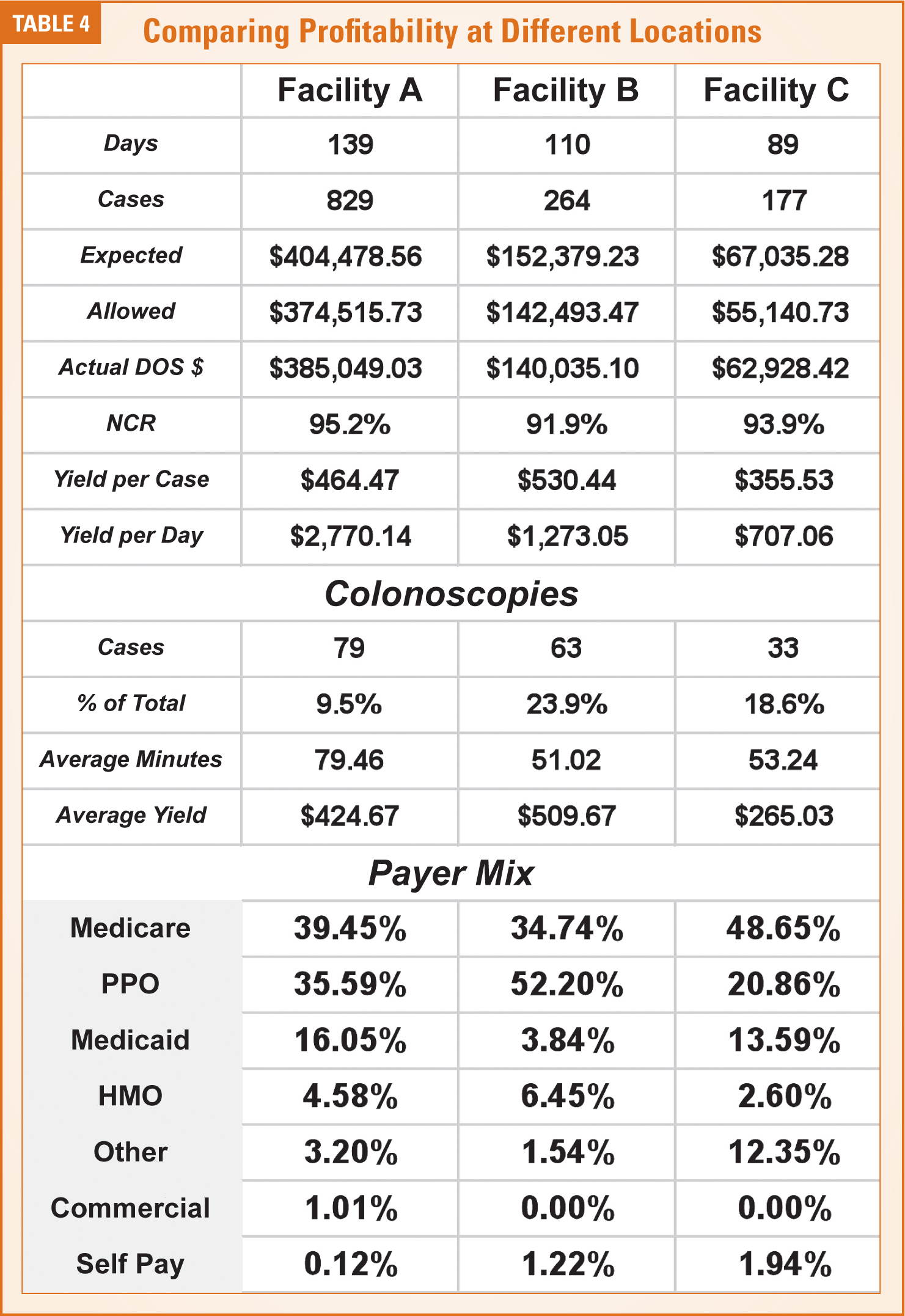

An effective management strategy for any line of business must be specific to each site of service. As a general principle, a cost center model is most appropriate. The idea is to be able to establish and monitor the profitability of each venue (as in Table 4), which would involve tracking all the factors that determine both the potential revenue stream, the overall productivity of the venue and the cost of providing the care. This is the direction where most anesthesia practice management accounting is heading because of the challenge of unprofitable lines of business and venues. Today’s practices must be more vigilant and willing to take appropriate action when particular lines of business are identified as unprofitable because unproductive venues can be the death of a practice.

Applying this concept to endoscopy is not always easy, especially when endoscopy cases are scheduled in surgical venues, but it is critical in all situations where the specific focus of a coverage contract is endoscopic care. Consider the example mentioned above. A practice provides anesthesia for endoscopy in three distinct venues: two hospitals and a surgery center. Good accounting requires a clear delineation of the factors affecting the profitability of each site in order to assess the actual impact on the practice as a whole. It may be that one venue is so inherently profitable that it more than covers the cost of the others, which is fine. Suppose, however that the revenue from the once profitable surgi-center business starts to slip dramatically. This could be critical to the overall management strategy of the practice. The same five factors listed below will also serve as useful criteria for the evaluation of potential new venues.

- Volume trends are essential to profitability and it is especially useful to monitor volume at the CPT level because the goal is a preponderance of short cases involving relatively health patients.

- Payer mix can be tracked at a fairly high level for purposes of monitoring the impact of Medicare and Medicaid on the overall revenue stream.

- Payer policies, however, should be monitored at the individual payer or plan level because these will determine the ongoing viability of the practice and because failure to identify changes in payer requirements on a timely basis can prove both significant and costly to resolve.

- Monitoring the accounts receivable closely is also essential. This would typically involve a regular review of the consistency and accuracy of contractual payments, the impact of deductibles and co-payments and changes in payer processing that can materially alter cash flow.

- In addition, the practice should closely monitor the productivity of each venue on a normalized basis by tracking the average cases per day and the average net yield per case so that there is always an accurate determination of the overall yield per provider day.

There is no one way to achieve this level of financial accountability but it should be understood that the data elements must somehow be combined to provide a clear and concise dashboard that the practice can monitor. Few billing systems have one report that brings all the pieces together in a single report, which is where a spreadsheet may prove the most useful accounting tool of all. Visual charting of volume, payer mix, A/R, productivity metrics and overall profitability is always an effective management tool. The key to effectiveness is the ability to monitor performance trends at a high level with an eye to outliers and exceptions, so that problems and issues can be identified and analyzed before they become significant.

Conclusions

Anesthesia for endoscopy is not a new phenomenon. Many of us have been monitoring the economics of this line of business for years, wondering whether or when the market will change. We are still waiting for the crash that so many have anticipated for so long. The fact is that despite all the hype and all the dire predictions change actually happens only incrementally in medicine. Payers adopt more stringent policies and this impacts the processing of their claims. This is where payer mix is either a practice’s curse or salvation. It is all about the numbers. The sum of the factors identified above must be adequate for the arrangement to be profitable and the changes over time should be neutral or positive.

Every anesthesia practice finds itself covering three kinds of venues: those that are inherently profitable with no financial support from the facility; those that are profitable with some level of financial support; and those that are completely unprofitable. Because there is no evidence that any facility is going to subsidize an anesthesia practice for anesthesia for endoscopy coverage then these arrangements must, by definition, fall into the first category if they are to be viable. This is the challenge facing all anesthesia practices today: knowing which coverage obligations will meet the financial requirements of the practice especially given the reimbursement and policy changes that have been discussed. Given the evidence, though, it is safe to assume that there is likely to be a place for anesthesia in managing patients through endoscopic procedures for the foreseeable future. Just as preparation is the most critical phase of an anesthetic procedure, so too is rigorous due diligence the most critical predictor of success in any endoscopic service agreement. Success and opportunity will come to those who do their homework and test their assumptions assiduously.

Jody Locke, CPC, serves as Vice President of Pain and Anesthesia Management Services for ABC. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He will be a key executive contact for the group should it enter into a contract for services with ABC. He can be reached at Jody.Locke@AnesthesiaLLC.com.