Anesthesia Industry eAlerts

Sent to subscribers every Monday morning, our eAlerts deliver timely updates on regulatory, legislative and practice management developments of interest to anesthesia professionals.

Complete the simple form below to subscribe.

Paycheck Protection Program Application Extension Alert!!

July 6, 2020

On July 4, 2020 President Trump signed legislation that extends the filing time for small businesses to apply for the Paycheck Protection Program (PPP). The former deadline was June 30th and is now extended to August 8th. Applications for the program and updated interim rules can be found on the US Treasury website: Click here.

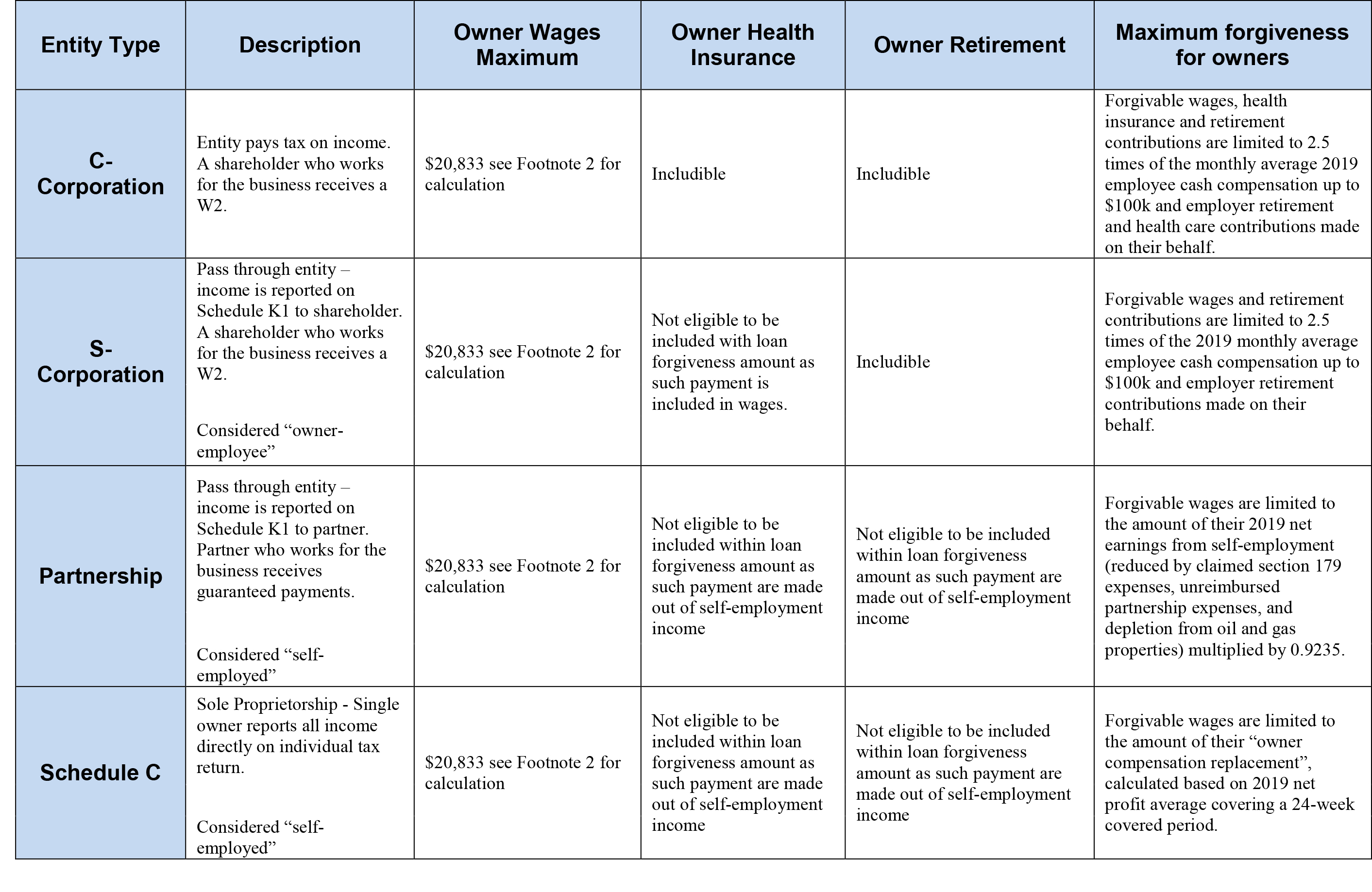

In the interim rule released on June 22, 2020, additional details were provided regarding shareholder and owner compensation that is eligible for PPP loan forgiveness. Shareholder or partner payroll costs that qualify for forgiveness will vary depending on the applicant’s corporate structure. This chart provides a summary of those eligible costs as it applies to different entity types. To view the full text, please click here.

Grant Thornton's COVID-19 Stimulus for Small and Mid-Sized Businesses

Appendix PPP loan forgiveness – eligible payroll costs

Interim Rule Forgiveness Update June 22, 2020

Footnote 1- Eligible employee compensation includes salaries, wages, commissions, or similar compensation; cash tips or the equivalent; payment for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payment for the provision of employee benefits consisting of group health care coverage, including insurance premiums and retirement; payment of state and local taxes assessed on compensation of employees.

Maximum forgiveness per employee using annualized 24-week period is $46,154 = ((24/52) x $100,000) any annual wages less than $100,000 should be considered in the formula on a pro rata basis. Assumes 8-week period is not elected.

Footnote 2- Maximum forgiveness for “owner-employee” and “self-employed” income is limited to 2.5 months set by the loan application: $20,833 = ((2.5/12) x $100,000). Assumes 8-week period is not elected.

*Information in this “Appendix” is provided for informational purposes only. Please consult with your legal, finance, accounting, or other business advisers when making any decisions relating to the above information.