eAlerts

-

Leveling the Playing Field

Jody Locke, MA

Vice President of Anesthesia and Pain Practice Management Services,

Anesthesia Business Consultants, LLC, Jackson, MITraditionally, three factors have determined the value and profitability of an anesthesia practice: case volume, payer mix and appropriateness of staffing. Because case volume and payer mix are essentially determined by the location and reputation of the facility, the only factor in which the practice actually had any influence was staffing; but, even here, culture, tradition and the coverage expectations of the facility tend to be the effective determinants of staffing model and number of providers.

Each practice is unique in its case volume and mix of surgical and obstetric procedures. Each is also unique in the percentage of patients whose insurance pays at significantly discounted rates set by federal and state regulators. Then there is the question of coverage requirements and the facility’s willingness to subsidize the practice’s financial loss in providing the necessary services. All of this indicates the potential for great disparity in the financial viability and ongoing potential for success of American anesthesia practices. Some practices claim to have more leverage in negotiating contract rates with commercial insurance plans, and this may result in a strategic advantage. This is certainly the claim of some of the nation’s largest practices and staffing companies; but the reality is that, for a variety of reasons, this advantage is diminishing. The fact is that while many smaller practices have felt somewhat disadvantaged in the past, this may be changing. One might even argue that we are seeing a leveling of the playing field. In other words, when we take a close look at the impact of the recent surprise billing rules, they may actually be good news for small and moderate practices.

Those of us who have been monitoring public policy changes impacting anesthesia over the years can clearly document a consistent theme: the advanced press of most policy changes has always been more concerning than the actual implementation. When the Health Care Finance Administration (HCFA) changed the way payment would be divided between medically directing physicians and medically directed CRNAs in the 1980s, many anesthesiologists expressed concern that this would result in a loss of control and revenue when, in fact, the revised Medicare payment rules actually made billing simpler. It is true that the implementation of Resource-Based Relative Value System (RBRVS) in the 1990s did impact anesthesia more profoundly than other specialties, but most compensated for the drop in revenue by cost-shifting to commercial plans and by requesting higher subsidies from hospitals. The implementation of ICD-10 had the potential to increase claim denials and disrupt practice cash flow, but it turned out to be a non-event. And so, it may well prove to be with the No Surprises Act. The reality is that the economics of anesthesia are increasingly complex, and the impact of changes to one variable in the equation becomes less and less impactful.

Anesthesia Economics 101

Let us first assess the potential financial impact of the proposed changes on the typical anesthesia practice. Public payers—Medicare, Medicaid and workers compensation—are not affected by the new rules, and they represent 40 to 60 percent of the units billed by the average practice. The commercial insurance plans with which practices contract are also not affected, and they may represent another 30 percent of billed units. When a practice contracts with an insurance plan, the contract defines the patient responsibility, which is usually about 20 percent of the allowable payment amount. Let us be clear here: the No Surprises Act applies only to patient situations where there is no contractually defined allowable payment. For example, if the contract rate with a particular plan is $60, then this amount, multiplied by the billable units, determines the allowable amount, and there is no surprise. Some patients may not understand the impact on actual insurance payments of deductibles and co-insurance, but this is not what the legislation was intended to address.

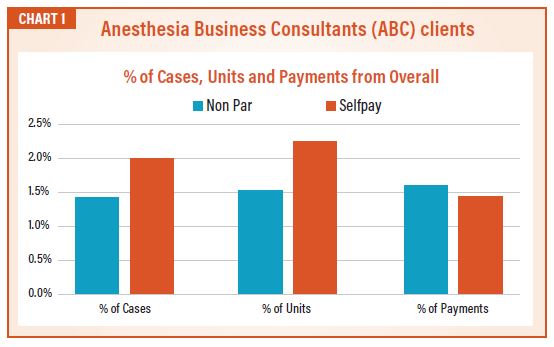

The No Surprises Act only affects two categories of charges: charges for out-of-network patients and those who have no insurance. The data used for Chart 1 is a composite of that from all Anesthesia Business Consultants (ABC) clients across the country. It demonstrates the number of cases and units billed in 2021 to each category of patient. In 2021, the percentage of the average practice impacted by the No Surprises law is relatively small, at about three percent. While it is unknown how much the percentage may increase in the years to come, this has to be our point of reference for now.

There is an important distinction demonstrated here. In 2021, the average practice collected fairly well for out-of-network patients (1.5 percent of charges resulted in 1.6 percent of payments), whereas they have collected less for patients with no insurance (1.8 percent of charges resulted in 1.4 percent of payments), which should come as no surprise. For most practices, when a patient has no insurance, there is no expectation of a meaningful payment. There are very few practices that collect more per unit for out-of-network cases than their average yield per unit. Based on this analysis, two things are clear. First, no practice is collecting an unusual or exorbitant amount per unit for out-of-network cases. Second, the implementation of the new law should not have a material impact on any ABC anesthesia practice.

The Impact on Contracting

Let us suppose that a client has a contract with an insurance plan that the client wants to renegotiate to a higher rate per unit. Typically, this process involves submitting a request for a higher rate. When the plan pushes back, there ensues a negotiation, the outcome of which depends on two factors: the value of the group’s participation in the insurance plan’s network and the provider group’s market leverage. Insurance plans need to be able to demonstrate their subscribers can access key specialists; that is an important aspect of their marketing plan. The fact is that, depending on the particular market, some practices are more valuable than others. Consider for example, Blue Cross of California. Being able to offer its subscribers access to any of the University of California hospitals is considered very important, which is why the anesthesia practices get a favorable rate. Market leverage is usually a function of market share. This is where size matters. A practice with a large share of a given market can usually use this leverage to their advantage and there are definitely examples of mega anesthesia groups that have negotiated higher unit rates than those given to smaller practices. It is important to understand, however, that their leverage was often based on their threat to opt out and bill patients as out-of-network providers. The reality is that No Surprises Act provisions essentially eliminate this leverage. Under the new rules, an out-of-network provider would only be paid at an average rate for the geographic area.

The Long View

The net effect of most market developments over the past few years has been to constrain practice revenue, and the No Surprises Act is entirely consistent with this trend. The average practice is seeing its Medicare population grow at a rate of about one percent, per year. This means that an ever-higher percentage of units gets paid at Medicare rates, over which providers have no control. As the cost of healthcare continues to rise, insurance plans are pushing back and limiting rate increases. Many plans have not agreed to contractual rate increases for a number of years. Since the ability to cost shift has been the advantage of many large practices, the impact of this act will constrain revenue options. In other words, only two factors will determine the revenue potential of a practice: volume and payer mix. What this also means is that anesthesia practices will have to shift gears and change their focus from revenue generation to cost management.

Most providers are aware of a basic reality, which is that it is easier to get paid by insurance plans than patients. This has been especially true during the pandemic. Collecting money from patients has always been a particular challenge for which there is no good solution. Collection agencies used to rely on a “dialing for dollars” approach to encourage patients to pay, but caller ID has effectively undermined that strategy. Many providers may have been concerned that the No Surprises Act would further erode the ability to collect from patients, but this is not true. As demonstrated above, only a small percentage of practice revenue has ever come from patients affected by this act.The reality of managing a practice in the United States is that things never get simpler; they only get more complicated over time. We tend to get excited and focus on each new policy change or payer development. Each new development is just one more factor in the overall challenge of getting paid. This is why practices need timely and reliable data so that they can assess and respond to the evolution of the market.

Jody Locke, MA serves as Vice President of Anesthesia and Pain Practice Management Services for Anesthesia Business Consultants. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He is a key executive contact for groups that enter into contracts with ABC. Mr. Locke can be reached at Jody.Locke@ AnesthesiaLLC.com.

-

Understanding the New Normal

There was a time in the history of anesthesia practices when the biggest question was whether the practice should explore new clinical opportunities and/ or merge with other practices in the area. Anesthesia practice management in those days tended to be very strategic and tactical. What we are seeing now makes us think those were the good old days. This issue of the Communiqué provides a useful overview of the new set of challenges practices must understand and address to remain viable.

Much has been made of the recent balance billing laws and the national No Surprises Act. Our own Jody Locke, MA helps put the recent regulations in perspective. As is so often the case, the advance press paints a more dire picture than the actual implementation. Leveling the playing field puts the key issues in a new and interesting perspective.

Dan Reale, JD, MBA has many years of experience managing small and large anesthesia practices across the country. No one is more qualified to address questions about the future of private anesthesia practice. His careful review of some very relevant data about the evolution of hospital perspectives on the specialty of anesthesia is quite informative. His article provides a very cogent caveat emptor about the future of hospital employment of anesthesia providers.

Mark Weiss, JD shares his thoughts on the challenge of the RFP. Mark’s article, Anesthesia Services RFPs: Cognitive Biases and Hidden Opportunity, challenges the current and prevailing perspective of RFPs. One man’s problem may just be another man’s opportunity.

As always, Will Latham, MBA brings us down to earth with some very pertinent and useful observations about executive boards and their limitations. His piece contains a particularly probative discussion of board challenges and opportunities. After 30 years in the anesthesia practice management business, Will has learned some important lessons that we should all take to heart.

Kathryn Hickner, Esq., along with Chuck Mackey, share some critical insights into the world of cybersecurity. Their article, Three Cybersecurity Safeguards to Implement in your Organization Today, provides a wealth of specific, technical information about the current cybersecurity environment and how it may impact your practice. Her piece provides an invaluable glossary for all of us.

And finally, Bart Edwards, MHS, MBA digs into the impact of the shift of cases from inpatient to outpatient. His data and focus give us much to think about and highlights the trends we should be tracking.

As always, we have given considerable thought to the trends facing our client practices. We hope these articles will give you a new perspective and some useful suggestions as you navigate today’s perilous healthcare market. Please feel free to give us some feedback and insights from your specific practice.

With best wishes,

Tony Mira

President and CEO -

Anesthesia Services RFPs: Cognitive Biases and Hidden Opportunity

Mark F. Weiss, JD

The Mark F. Weiss Law Firm, Dallas, TX, Los Angeles and Santa Barbara, CAAt a recent anesthesia conference, I heard speakers address the avoidance of, and observed audience members nearly quivering in fear of, three rather insignificant symbols, the letters: R, F and P.

Yes, it’s true that “RFP” is the acronym for a “Request for Proposal,” the commodity buying tool that’s been morphed into a services buying tool by midlevel bureaucrats and lazy thinkers. Ah, but such is life, and there’s no upside in pretending that it isn’t so. But if the world is full of lemons, why not think lemonade?

RFPs and Cognitive Bias

Fear is a driver of action, and I don’t blame speakers, authors or experts for driving home the point that, for an incumbent anesthesia group, an RFP can be a calamitous event, one to be avoided at nearly all cost. In full disclosure, as a speaker, author and expert, I, too, often drive home that exact same point.After all, if you’re the incumbent anesthesia group, your relationship with the hospital or other facility, including your exclusive contract, if you have one, is at risk. There’s little doubt about it, even if the outcome, a little form of death, isn’t completely certain.

But it might be certain for your group, thus the entirely rational fear of an RFP on the part of the average anesthesia group leader, or perhaps even on the part of close to all anesthesia group leaders.

When you think of it, the fear of RFPs is akin to the fear of snakes. The fear is so ingrained that we see general things that might possibly be snakes, like sticks on a hiking path, as snakes. After all, that cognitive bias makes perfect sense: there’s little to no downside in seeing a stick as a snake, but a potentially calamitous downside in seeing a snake as a stick.

Anesthesia group leaders generally see the entire topic of RFPs from the point of view of being bitten by one. That’s the cognitive bias that RFPs, like snakes, are dangerous and to be avoided. Yet others eat snakes and (carefully) go looking for them, which takes us to the jumping off point of this article: Maintain a healthy fear of RFPs that seek to bite you, but develop a careful approach to hunting for RFPs that you can bite into.

After all, snake meat can be delicious. Let’s go get some.

Flipping the Cognitive Bias: Let’s Go Snake Hunting

To recap what we’ve discussed so far, if you’re the incumbent anesthesia group, an RFP puts your relationship with the hospital or other facility at risk. But, if you’re an outside aspirant, RFPs as to other facilities present opportunities to expand your business to additional locations. And even better, the facility issuing the RFP is probably (see below) considering a change.

Instead of fearing the RFP process as you do in defending your existing facility relationships, embrace it in seeking to respond to other RFPs.

In the way of thinking that I urge you to consider (don’t worry about the competition, most won’t consider it), you’ll see RFPs as a way to hedge against your existing facility side bets, not as betting your facility.

But is the RFP for Real?

Let’s examine the RFP process from a simple starting point: is any particular RFP real, or is it something else?

But even before doing that, it pays to start with the truth: professional services are not, and cannot, be a commodity. But themselves (or more likely, others) into believing that they are. In fact, there’s an RFP industry ready to help.

But, even if you’re a true believer in the commodity theory of healthcare, an RFP process for anything other than fixed items (such as for 3.72 million screws meeting Mil-Spec MS51861-1C) is a ridiculous way to make a decision, a way that exists only in a world in which those bureaucrats known as facility administrators are rewarded by visible, yet lazy action, situated in a universe devoid of the knowledge that not taking visible action can be action just the same.

Are these lies moral failings? Usually not. They’re generally more akin to resume embellishments, nicely pressed suits and shiny shoes. But either way, they’re a fiction, a fantasy and perhaps even fraud.

So, what to do in the real world in which my thoughts about the craziness of the process have (unfortunately) little weight?

You must first assess the reality of the RFP against the three categories into which I divide them:

- True RFPs: These are genuine searches for the best-quality provider with a favorable ratio of quality to cost. This type of RFP is the closest in relationship to the traditional form used in industry and government. It’s commonly seen in situations in which the current, or sometimes very recently former group, has “blown up” and can no longer provide coverage. It’s also common in scenarios where the current group has completely lost the facility’s trust.

- Fictitious RFPs: These RFPs belie the fact that hospital administrators are not interested in the merits of any response; they have already decided to whom they will award the contract. Yet, for one political reason or another, they’ve decided to issue a phony RFP to project a patina of “fairness” to the medical staff, to the hospital’s own board, to some third party—or perhaps to you.

- Fulcrum RFPs: Consider this the weaponized RFP. As the name implies, the increasingly common fulcrum RFPs are designed to create leverage. The facility intends on renewing with the present group but uses the RFP as a tool to dictate terms by fiat and to pressure the group into negotiating against its own best interests out of fear of replacement. Nonetheless, the facility is open to competing proposals.

Although no outside assessment of category can be completely reliable, clues often abound. And, category dictates your strategy moving forward—or not moving forward.

Some More Cognitive Flips: You’re a Buyer Not a Seller

Groups seeking to protect themselves against an RFP being issued, and, certainly, those seeking to protect themselves against an already issued RFP, generally see themselves as the seller of services.

After all, if the group is dependent upon that facility relationship for its existence, they have little choice, that is, unless they are the rare outlier that would rather disband than be forced into a bad deal.

But in connection with hunting down other RFPs, you must adopt a buyer mindset.

Note that I said “mindset” to distinguish the concept of inner talk and expectations from the fact of the matter that you will still engage in activities to, in essence, “sell” the deal, as you desire it, to the potential facility deal partner.

Understand how to play to the administrators’ cognitive biases (e.g., “the existing group is dysfunctional,” and, for new CEOs, “you need to demonstrate leadership”). But be very careful about what you promise because, in the event that you “win,” you’ll actually have to deliver.

However—and here’s the important point—if the deal doesn’t look attractive to you, or if you think it’s not real (i.e., that it’s a Fictitious RFP or a Fulcrum RFP), or if you “lose” the RFP (which might turn out to have been a win in disguise, because winning the race to the bottom is like a participation trophy at the local recreation center: it isn’t a real win), so what! Just don’t “buy” it; move on to the next deal.

As an offensive weapon, pursuing RFPs can be a powerful strategy to exploit. Yes, time and effort and a governance structure that allows you to take advantage of it are all required; however, properly strategized, you control your group’s timing, you control how much effort to devote, and you control if and when to pull the plug, protecting your downside.

You will have flipped the usual RFP paradigm on its head: even if the odds of not obtaining the contract are high, the costs and effort can be controlled. But the upside of obtaining the right deal can be tremendous. And, since you are thinking like a buyer, not a seller, if the deal isn’t right, don’t buy; just walk away.

Mark F. Weiss, JD is an attorney who specializes in the business and legal issues affecting physicians and physician groups on a national basis. He served as a clinical assistant professor of anesthesiology at USC Keck School of Medicine and practices with The Mark F. Weiss Law Firm, a firm with offices in Dallas, Texas and Los Angeles and Santa Barbara, California, representing clients across the country. He can be reached by email at markweiss@weisspc.com.

-

The Future of Independent Anesthesia Practice

Daniel S. Reale, JD, MBA

President, Plexus Management Group, LLC, Westwood, MAMuch has been written over the past decade on the supply and demand for anesthesia services, and how it relates either to the acquisition of anesthesia practices or to the direct employment of anesthesia providers by hospital systems. These crosscurrents need to be analyzed in the context of the overall trend in physician services in the United States.

An analysis prepared by Avalere Health in June 2021 provided an in-depth view of overall trends among physician practices. Among the key findings of the analysis, which was conducted over a two-year period between January 1, 2019 and January 1, 2021, were the following:

- 48,400 physicians left independent practices and became employees of hospitals or other corporate entities, with 22,700 of those physicians moving after the onset of Covid-19.

- 18,600 became hospital employees (11,400 made the shift after the onset of Covid-19)

- 29,800 became employees of corporate entities (11,300 made the shift after the onset of Covid-19)

- Over the two-year study period this shift resulted in a 12 percent increase of employed physicians.

- Importantly, the study indicated that 69.3 percent of all U.S. physicians were either employed by hospitals or corporate entities as of January 2021, versus 62.2 percent as of January 2019.

- Interestingly, the study indicated that as of January 2021, 49 percent of all U.S. physicians were employed by hospitals and health systems and 20 percent of U.S. physicians were employed by corporate entities.

Avalere’s analysis well documents the national trend in the consolidation of physician practices and the increasing momentum from independent practices to employed models—clearly exacerbated by the economic dislocations associated with the pandemic. This article will examine the trends within physician practices in general and examine how these trends apply to anesthesia practices in particular.

It is difficult to obtain data similar to the above solely for anesthesia. Surveys conducted by Enhance Healthcare Consulting (EHC) does provide some evidence of employment trends in anesthesia. EHC conducted surveys of hospital C-suite executives in 2016 and in 2021. The 2016 survey results indicated that 49 percent of the respondents “actively sought an alternative to their current anesthesia provider” and 25 percent of respondents made a change. In 2021, these results were 42 percent and 87 percent, respectively. The 87 percent change in anesthesia providers in 2021 seems to reflect the underlying tumult in the anesthesia services space. The primary reason cited by the hospital executives for seeking a new provider was the subsidy level (40 percent in 2016 and 33 percent in 2021). “Inadequate service level” was cited for initiating the anesthesia review process by 34 percent of the respondents in 2016 but only 20 percent in 2021. (Note: “Desire to change staffing model” gained 40 percent of the vote in 2021 and no votes in 2016, but this may have resulted from a change in the format in 2021.) While this survey is not an exact parallel to the Avalere survey, it is indicative of the level of discordance between hospitals and their anesthesia groups. The survey also did not indicate whether the current provider group was part of a national consolidator or an independent group. The survey’s primary importance is that it provides insight into current thinking of hospital administrations and their levels of dissatisfaction. This certainly reflects a sense of continued uncertainty within the provision of anesthesia services at hospitals in the Unites States. Such dissatisfaction could suggest overall risks and potential opportunities for consolidators and independent practices as well as opportunities for groups to become employed.Initial Efforts at Consolidation

For a number of years, large corporate entities, often funded by private equity firms, have attempted to further consolidate the anesthesia practice space. Among the consolidators are North American Partners in Anesthesia (NAPA), Mednax, US Anesthesia Partners, and Envision Healthcare. Consolidation has been going on for over a decade. I am personally aware of a large private New England group having been approached by Pediatrix (predecessor corporation of Mednax) in 2007. As one of the first consolidators, Mednax’s experience with anesthesia services is enlightening with the results of the operation of anesthesia services proving to be disappointing to the acquirer. Mednax reported an operating loss for its Anesthesiology Services Medical Group for the year ending December 31, 2020 of $716.3 million (this included the loss on sales of $663.7 million). This loss followed an operating loss for Anesthesiology Services Medical Group for the year ending December 31, 2019 of $1.23 billion dollars (this included a non-cash goodwill impairment charge of $1.33 billion dollars). Mednax’s anesthesia assets represented an investment in excess of $1 billion dollars but were sold to NAPA in May, 2019 for $50 million in cash with retained accounts receivable and a contingent economic interest in future success of these sites under NAPA. Mednax cited (in its SEC filings) some of the difficulties associated with its practice of anesthesia as the following:

“During the time that it operated as part of Mednax, and particularly since 2017, American Anesthesiology experienced multiple business challenges, including inflation in unit labor costs and other expenses, constraints to revenue growth based on adverse changes in payer mix, and a difficult reimbursement environment where unit revenues grew at levels meaningfully below unit cost.”

Mednax is an example where a company with tremendous success in hospital-based physician services, i.e., the pediatric neonatal intensive care space, had difficulty translating that success to the anesthesia marketplace for the above reasons. Mednax’s experience highlights the difficulty of large-scale acquirers successfully operating in the anesthesia space. Later in this article, we will discuss this further in the context of the independent anesthesia practice and the future of the independent anesthesia practice versus consolidation.Hospitals Get into the Act

As the private equity firms have moved into the anesthesia marketplace, hospital systems have also made aggressive efforts at employing groups. Hospital systems have moved to absorb all or most of the anesthesia groups at their member hospitals, e.g., MassGeneral Brigham in the Boston area, McLeod Health in South Carolina, Southcoast Health in southern Massachusetts, Steward Healthcare (a for-profit system started in Massachusetts and now in multiple states), Cedars Sinai Hospital in Providence, Rhode Island. Other systems have dipped their toes into the anesthesia services space by employing anesthesia providers as a subset of their system, e.g., Piedmont Healthcare. In our experience, the systems have paid greater amounts to support their anesthesia groups when employed as opposed to when they were independent.

Pondering a Loss of Independence

What would motivate an independent group to either sell to a consolidator or to become employees of a hospital system? First, let’s look at why a group would consider a sale to a national consolidator. Speaking with practitioners who have either entertained offers from a consolidator or have, in fact, consummated a sale with a consolidator, we have a good sense of how the economics of these transactions are structured. The consolidators essentially are paying out future earnings to the owner-providers through the buy-out process. Typically, the owner-providers income is reduced by an agreed upon formula, and that reduction in the previous compensation is paid back to the owner-providers in the form of a buy-out that is calculated as a negotiated multiple of said adjusted “earnings.” In some cases, the earn-out is subject to holdback, growth-related incentives and other potential earning enhancement opportunities. The question, of course, is how the acquirer can get an economic return by “pre-paying” these future earnings. The previously quoted analysis from Mednax provides some light on how consolidators “expected” to be able to work the post-acquisition environment to their economic advantage. For example, the consolidator would look to leverage higher commercial rates including, in some cases, going non-par with commercial payers. (The No Surprises Act may significantly reduce this potential.) A consolidator would look for labor substitution, e.g., using lower cost new graduates of anesthesia medical programs or nurse anesthetists or anesthesia assistants. The consolidators would also look to leverage other potential expense areas regarding overhead including lowering revenue cycle management costs, quality assurance costs and malpractice costs. On the providers side, the motivation is clear–prepayment of future, uncertain income. In addition, being part of a larger system may create opportunities for certain physician leaders within these groups, to take on larger roles in the clinical and business sides on a regional and national basis. Given the potential economic upside to the owner-provider, what are the downsides? Clearly, the Mednax example points to one downside—the inherent uncertainty in future prospects of the acquirer relative to the anesthesia marketplace. A second downside related to the providers could be related to the earlier discussed “hold-back” with that payment potentially being at risk depending on the success of the consolidator in the marketplace, as well as the group’s attaining its pre-negotiated objectives. The underlying contracts with the institutions could also be at risk, and depending on the terms of the employment contract, the providers ability to stay at that particular location post-termination could also be at risk. Young providers within the group, not yet risen to the owner status level, may become dispirited. It is no surprise that a provider’s motivation changes when they move from an independent practice status, with attendant incentives to work hard to become an owner and be rewarded no longer in play. Macro-economic factors have a significant impact on the anesthesia business. Covid and the consequent downturn in elective cases in 2020 had a major, negative economic impact across all levels of anesthesia—whether independent practice, corporate or hospital employed. The recent No Surprises Act has seen an impact on anesthesia contract rates and on payment rates for non-par payers. Covid-related retirement/employment expectation changes among anesthesia providers has resulted in increased demand for services among a smaller base of anesthesia providers. A recent review of Gasworks suggested there were over 3000 openings for anesthesiologists and over 7000 openings for nurse anesthetists. Supply and demand suggest that wages will increase. Consequently, groups that we manage are experiencing pressures for higher wages from their existing staff and from potential new hires. With the possibility of decreases in commercial reimbursement and the ever-present threat of further reductions in the already very low governmental payer rates, the primary mechanism to attain their earnings expectations is to look to the hospitals (and in some cases ambulatory surgical centers) for financial support. Already, over 80 percent of hospitals provide some form of stipend to their anesthesia providers. For the consolidators, these market forces place even greater pressure on their potential for economic returns. When a consolidator approaches a hospital for an increase in stipend, the administrators understand that an economic driver for the increase is support for the return on investment for the owners of the consolidators. This may become a factor in hospitals looking to terminate contracts with physician groups run by consolidators (or independent groups, for that matter) and choose to either select a new independent group or employ the current group.

Hospitals Looking to Hire and Acquire

In looking at hospital motivations for acquiring groups, one can see both economic and non-economic justifications. The changing demographic of the United States as a result of the aging baby boomers and the concomitant increase in the Medicare population has had a significantly disproportionate impact on anesthesia providers. (Medicare pays anesthesia at rates which are one-quarter to one-third of commercial payers.) One expert in the anesthesia revenue cycle space has estimated that the percentage of Medicare will increase by one percent per year over the next decade as the population continues to age. As indicated earlier, it is estimated that 80 percent of hospitals currently provide stipend payments. The increase in the Medicare population will place more pressure on hospitals to continue to supplement those stipends. Moreover, shortages of anesthesia providers and increased compensation create a double-whammy effect.

Hospitals may believe that, through employing anesthesia groups, they can exert more control over staffing models and coverage arrangements, as well as obtaining higher reimbursement rates from commercial payers, so they can theoretically provide a lower support to an employed group—as opposed to the stipend required by an independent group. Our experience in working with groups that were formerly independent and are now employed suggests otherwise. In fact, we have seen the required support paid by hospitals in order to cover their anesthesia services go up many multiples over what they were paying the independent groups. This, of course, may relate to the inherent incentives of a private group to work more hours than an employed provider. An employed provider has less incentive to work the additional hours unless they are paid for those additional hours. An independent provider will work additional hours because of the benefits of operating at a “reduced” staffing level, i.e., the ability to not hire an additional body but absorb that work within the existing complement of staff translates into additional compensation that can be shared with the core provider group. It will be interesting to see how the recent movement to employ anesthesia provider groups continues into the future given the potential for unforeseen additional costs associated with the employed model.Of course, there are other motivations for a hospital wanting to acquire the anesthesia group. The hospital may believe they can lower the overhead costs, such as taking revenue cycle in-house or by being better able to leverage less for outside revenue cycle companies. The hospital may be able to lower other administrative costs, such as benefit costs and administrative overhead costs by absorbing those types of administrative services into its existing infrastructure. Moreover, the hospital may be able to implement policies that may not be cost effective for a private group (e.g., flip rooms) but would be very attractive to surgeons in the hospital as part of a hospital’s policy to increase its surgical case load.

The market forces, including provider supply/demand dynamics, demographic changes, the No Surprises Act repercussions and recent “failed” consolidations, will require continued observation in assessing the future direction for anesthesia services. Will increased costs to the hospitals after employing the independent groups create a backlash and potential reversal of this practice? Similarly, as with Mednax, will some of the larger consolidators realize that the return on investment is not in the anesthesia space? We have recent evidence of another large consolidator agreeing with some of the acquired groups to relinquish contracts to those groups and waive their non-competes. These recent examples suggest there may be more underlying economic turmoil in the acquisition model than has been apparent heretofore. The core motivations for independent groups continuing their independent status exist as much now as they did before with their ability to control their revenue streams, select their colleagues, create a positive culture and select the types of locations they prefer to practice. In addition, those physicians have the ability to work the most flexible staffing models, the ability to control their vacations to the greatest extent and control care team environment and call burden in ways that are determined by the group and its members. From our working with independent practices throughout the United States, the level of internal satisfaction in independent groups continues to be largely positive. As discussed earlier, the healthcare market has seen earlier waves of acquisition of physician practices. In the nineties, these were primarily driven by hospital systems and their physician practice management companies. The earlier efforts were largely unsuccessful. Most recent consolidation of physician practices is now often led by health insurance companies, such as United Healthcare, Humana and BCBS of Texas. As discussed, the private equity firms have made a full commitment to consolidation of a broad range of physician practices. It is unclear where anesthesia services will fit given some of the issues discussed herein.

The overall trend in the healthcare marketplace is for increasing employment of physicians either by hospital systems or by large corporate entities. This trend has accelerated during the pandemic, not surprisingly as a result of the increased amount of uncertainty surrounding the drop in patient volume and attendant incomes. This movement has translated into the anesthesia provider services as well. As noted, the large health systems have moved to employ physicians on a large-scale basis. We have also seen, perhaps, the beginning of a negative trend resulting from those consolidations (e.g., Mednax and other national providers) fully abandoning anesthesia or selectively abandoning anesthesia sites. Other hospitals have slowed plans to employ anesthesia groups as they see the increased costs associated with an employed model. In the meantime, salaries for independent and employed anesthesia providers are increasing significantly due to staffing shortages. For the independent practice of today, there are multiple avenues of support including external practice management companies that can assist in maximizing economic return to the group through commercial contract negotiations, expert revenue cycle management and expertise in hospital negotiations. Will this be a repeat of the nineties where the momentum of physician practice consolidation was reversed as a result of dissatisfaction with the resulting practices? We do not know. It is a trend we will continue to watch while this process unfolds. The old adage seems to apply to the ongoing anesthesia practice environment: “May you live in interesting times.”

Daniel S. Reale, JD, MBA, President has been with Plexus Management Group for 17+ years. His responsibilities include overseeing the expansion of managed physician practices. Mr. Reale has 30+ years of experience in managing healthcare services and biomedical operations. Previous experience includes a public, biomedical company that develops medical devices for urological and oncological applications, a biotech company responsible for the development and opening of manufacturing operations for an autologous colon cancer vaccine and a venture-based company outsourcing hospital blood-banking and blood collection services to hospitals throughout the United States. His education includes both a Juris Doctor degree from Northeastern University, Boston, MA; as well as a Master of Business Administration degree from the University of North Carolina at Chapel Hill. He can be reached at dreale@PlexusMG.com.

- 48,400 physicians left independent practices and became employees of hospitals or other corporate entities, with 22,700 of those physicians moving after the onset of Covid-19.

-

Is Your Board Overloaded?

Will Latham, MBA, President

Latham Consulting Group, Inc., Chattanooga, TNMany anesthesia group boards meet late in the day after a full clinical load. Exhaustion can set in, and board members can be overloaded. This may result in work not getting done or make it more difficult to find individuals to serve on the board.Many anesthesia group governing boards often get mired down while addressing important group issues or trying to make decisions. They also have a tendency to micro-manage rather than govern. Following are some ways to overcome these challenges.

Send It to Committee

We have found that the best medical group boards use their committees to process information prior to the board addressing an item. When an item is raised at the board level, the first step of the committee is to:

- Define the scope of the issue.

- Gather needed data.

- Analyze the data.

- Recommend a solution.

Once the committee has developed a solution or recommendation, this information should be presented to the board. However, the board must be extremely careful to not redo the work of the committee. If the board feels the committee has not completed the assignment, it should be sent back for further work.

In addition, the board should make every effort to accept the committee’s recommendation. Why? If the board members always reject the recommendations or re-does the work, the committees will reach the conclusion that their thoughts are not being considered and stop doing the work.

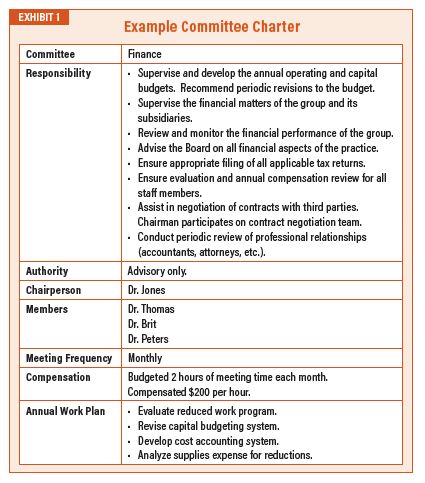

Naturally, the above assumes that the group has done a good job in establishing committees to get group members involved and share the administrative workload. The board should create a committee “Charter” for each committee (an example of such a charter is found in Exhibit 1) and outline:

- What are the on-going responsibilities of the committee?

- What authority does the committee have (for example, can they spend money, make certain decisions, etc., without coming back to the board)?

- Who is the chairperson and who are the members?

- What is the timeline of work being completed? If the answer is “whenever,” you may want to seriously consider whether or not the committee is even needed.

- What is the compensation for serving on the committee? • What is the annual work plan for the committee? This is where the board can outline its expectations for specific projects they would like the committee to work on in the coming year.

Disruptive Behavior

Many medical group boards get bogged down dealing with physician behavior issues. Hours and hours can be spent investigating and discussing disruptive behavior.

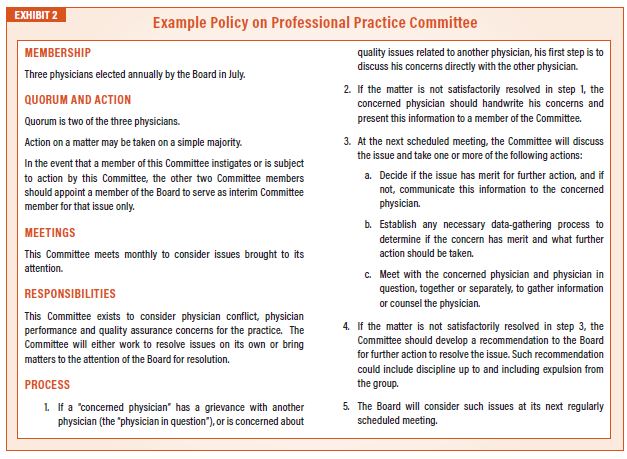

Although the board is typically the final decision maker in regards to fining or terminating a physician, much work can and should be done by a “Professional Practice Committee.”

This committee exists to consider physician conflict, physician performance and quality assurance concerns for the practice. The committee will either work to resolve issues on its own or bring matters to the attention of the board for resolution. In most situations, this committee does not have the power to censure or take action against a physician. Instead, it serves as an intermediary step or process to try to resolve the issues before significant steps are taken. A policy for such a committee may be found in Exhibit 2.

Avoid Micromanagement through Setting Policy

As a board tries to do its work, it’s often tempted to move from “governance/ oversight” to micromanagement of the organization. The best way to avoid this is to focus the board on setting “policy” rather than on making specific decisions.

A “policy” is a statement which guides and constrains the subsequent decision making. In setting policy, you try to specify the end rather than the means.In setting policy, the board should identify what is to be accomplished and a range of acceptable and unacceptable means for achieving the objectives. This could include a set of directives for how the group will operate in the future or instructions for management to implement.

To help the board avoid micromanagement, it’s often helpful to remind them that they don’t have to (and shouldn’t) make each and every decision. The board has options, which include:

- Request proposals and recommendations from management prior to making a decision. Example: “We need to avoid problem X. Management, please develop a set of alternative methods to achieve this end.”

- Delegating decision-making authority with constraints. Example: “We need to avoid problem X. Management, please develop a set of alternative methods to achieve this end, but it must cost less than $50,000.” • Delegating decisions with exceptions. Example: “We need to avoid problem X. Management, please develop a set of alternative methods to achieve this end, but it must be a process solution rather than a technology solution.”

- Retain authority and make decisions itself.

The best boards always think: “is this something that management or a committee should decide once we’ve provided guidelines?” The best boards spend most of their time setting policy.

For more than 30 years, Will Latham, MBA has worked with medical groups to help them make decisions, resolve conflict and move forward. During this time he has: facilitated over 900 meetings or retreats for medical groups; helped hundreds of medical groups develop strategic plans to guide their growth and development; assisted over 130 medical groups improve their governance systems and change their compensation plans; and advised and facilitated the mergers of over 135 medical practices representing over 1,300 physicians. Latham has an MBA from the University of North Carolina in Charlotte. He is a frequent speaker at local, state and national, and specialty-specific healthcare conferences. He can be reached at wlatham@lathamconsulting.com.

Most providers are aware of a basic reality, which is that it is easier to get paid by insurance plans than patients. This has been especially true during the pandemic. Collecting money from patients has always been a particular challenge for which there is no good solution. Collection agencies used to rely on a “dialing for dollars” approach to encourage patients to pay, but caller ID has effectively undermined that strategy. Many providers may have been concerned that the No Surprises Act would further erode the ability to collect from patients, but this is not true. As demonstrated above, only a small percentage of practice revenue has ever come from patients affected by this act.

Most providers are aware of a basic reality, which is that it is easier to get paid by insurance plans than patients. This has been especially true during the pandemic. Collecting money from patients has always been a particular challenge for which there is no good solution. Collection agencies used to rely on a “dialing for dollars” approach to encourage patients to pay, but caller ID has effectively undermined that strategy. Many providers may have been concerned that the No Surprises Act would further erode the ability to collect from patients, but this is not true. As demonstrated above, only a small percentage of practice revenue has ever come from patients affected by this act.

Fear is a driver of action, and I don’t blame speakers, authors or experts for driving home the point that, for an incumbent anesthesia group, an RFP can be a calamitous event, one to be avoided at nearly all cost. In full disclosure, as a speaker, author and expert, I, too, often drive home that exact same point.

Fear is a driver of action, and I don’t blame speakers, authors or experts for driving home the point that, for an incumbent anesthesia group, an RFP can be a calamitous event, one to be avoided at nearly all cost. In full disclosure, as a speaker, author and expert, I, too, often drive home that exact same point.

It is difficult to obtain data similar to the above solely for anesthesia. Surveys conducted by Enhance Healthcare Consulting (EHC) does provide some evidence of employment trends in anesthesia. EHC conducted surveys of hospital C-suite executives in 2016 and in 2021. The 2016 survey results indicated that 49 percent of the respondents “actively sought an alternative to their current anesthesia provider” and 25 percent of respondents made a change. In 2021, these results were 42 percent and 87 percent, respectively. The 87 percent change in anesthesia providers in 2021 seems to reflect the underlying tumult in the anesthesia services space. The primary reason cited by the hospital executives for seeking a new provider was the subsidy level (40 percent in 2016 and 33 percent in 2021). “Inadequate service level” was cited for initiating the anesthesia review process by 34 percent of the respondents in 2016 but only 20 percent in 2021. (Note: “Desire to change staffing model” gained 40 percent of the vote in 2021 and no votes in 2016, but this may have resulted from a change in the format in 2021.) While this survey is not an exact parallel to the Avalere survey, it is indicative of the level of discordance between hospitals and their anesthesia groups. The survey also did not indicate whether the current provider group was part of a national consolidator or an independent group. The survey’s primary importance is that it provides insight into current thinking of hospital administrations and their levels of dissatisfaction. This certainly reflects a sense of continued uncertainty within the provision of anesthesia services at hospitals in the Unites States. Such dissatisfaction could suggest overall risks and potential opportunities for consolidators and independent practices as well as opportunities for groups to become employed.

It is difficult to obtain data similar to the above solely for anesthesia. Surveys conducted by Enhance Healthcare Consulting (EHC) does provide some evidence of employment trends in anesthesia. EHC conducted surveys of hospital C-suite executives in 2016 and in 2021. The 2016 survey results indicated that 49 percent of the respondents “actively sought an alternative to their current anesthesia provider” and 25 percent of respondents made a change. In 2021, these results were 42 percent and 87 percent, respectively. The 87 percent change in anesthesia providers in 2021 seems to reflect the underlying tumult in the anesthesia services space. The primary reason cited by the hospital executives for seeking a new provider was the subsidy level (40 percent in 2016 and 33 percent in 2021). “Inadequate service level” was cited for initiating the anesthesia review process by 34 percent of the respondents in 2016 but only 20 percent in 2021. (Note: “Desire to change staffing model” gained 40 percent of the vote in 2021 and no votes in 2016, but this may have resulted from a change in the format in 2021.) While this survey is not an exact parallel to the Avalere survey, it is indicative of the level of discordance between hospitals and their anesthesia groups. The survey also did not indicate whether the current provider group was part of a national consolidator or an independent group. The survey’s primary importance is that it provides insight into current thinking of hospital administrations and their levels of dissatisfaction. This certainly reflects a sense of continued uncertainty within the provision of anesthesia services at hospitals in the Unites States. Such dissatisfaction could suggest overall risks and potential opportunities for consolidators and independent practices as well as opportunities for groups to become employed. Mednax is an example where a company with tremendous success in hospital-based physician services, i.e., the pediatric neonatal intensive care space, had difficulty translating that success to the anesthesia marketplace for the above reasons. Mednax’s experience highlights the difficulty of large-scale acquirers successfully operating in the anesthesia space. Later in this article, we will discuss this further in the context of the independent anesthesia practice and the future of the independent anesthesia practice versus consolidation.

Mednax is an example where a company with tremendous success in hospital-based physician services, i.e., the pediatric neonatal intensive care space, had difficulty translating that success to the anesthesia marketplace for the above reasons. Mednax’s experience highlights the difficulty of large-scale acquirers successfully operating in the anesthesia space. Later in this article, we will discuss this further in the context of the independent anesthesia practice and the future of the independent anesthesia practice versus consolidation. What would motivate an independent group to either sell to a consolidator or to become employees of a hospital system? First, let’s look at why a group would consider a sale to a national consolidator. Speaking with practitioners who have either entertained offers from a consolidator or have, in fact, consummated a sale with a consolidator, we have a good sense of how the economics of these transactions are structured. The consolidators essentially are paying out future earnings to the owner-providers through the buy-out process. Typically, the owner-providers income is reduced by an agreed upon formula, and that reduction in the previous compensation is paid back to the owner-providers in the form of a buy-out that is calculated as a negotiated multiple of said adjusted “earnings.” In some cases, the earn-out is subject to holdback, growth-related incentives and other potential earning enhancement opportunities. The question, of course, is how the acquirer can get an economic return by “pre-paying” these future earnings. The previously quoted analysis from Mednax provides some light on how consolidators “expected” to be able to work the post-acquisition environment to their economic advantage. For example, the consolidator would look to leverage higher commercial rates including, in some cases, going non-par with commercial payers. (The No Surprises Act may significantly reduce this potential.) A consolidator would look for labor substitution, e.g., using lower cost new graduates of anesthesia medical programs or nurse anesthetists or anesthesia assistants. The consolidators would also look to leverage other potential expense areas regarding overhead including lowering revenue cycle management costs, quality assurance costs and malpractice costs. On the providers side, the motivation is clear–prepayment of future, uncertain income. In addition, being part of a larger system may create opportunities for certain physician leaders within these groups, to take on larger roles in the clinical and business sides on a regional and national basis. Given the potential economic upside to the owner-provider, what are the downsides? Clearly, the Mednax example points to one downside—the inherent uncertainty in future prospects of the acquirer relative to the anesthesia marketplace. A second downside related to the providers could be related to the earlier discussed “hold-back” with that payment potentially being at risk depending on the success of the consolidator in the marketplace, as well as the group’s attaining its pre-negotiated objectives. The underlying contracts with the institutions could also be at risk, and depending on the terms of the employment contract, the providers ability to stay at that particular location post-termination could also be at risk. Young providers within the group, not yet risen to the owner status level, may become dispirited. It is no surprise that a provider’s motivation changes when they move from an independent practice status, with attendant incentives to work hard to become an owner and be rewarded no longer in play.

What would motivate an independent group to either sell to a consolidator or to become employees of a hospital system? First, let’s look at why a group would consider a sale to a national consolidator. Speaking with practitioners who have either entertained offers from a consolidator or have, in fact, consummated a sale with a consolidator, we have a good sense of how the economics of these transactions are structured. The consolidators essentially are paying out future earnings to the owner-providers through the buy-out process. Typically, the owner-providers income is reduced by an agreed upon formula, and that reduction in the previous compensation is paid back to the owner-providers in the form of a buy-out that is calculated as a negotiated multiple of said adjusted “earnings.” In some cases, the earn-out is subject to holdback, growth-related incentives and other potential earning enhancement opportunities. The question, of course, is how the acquirer can get an economic return by “pre-paying” these future earnings. The previously quoted analysis from Mednax provides some light on how consolidators “expected” to be able to work the post-acquisition environment to their economic advantage. For example, the consolidator would look to leverage higher commercial rates including, in some cases, going non-par with commercial payers. (The No Surprises Act may significantly reduce this potential.) A consolidator would look for labor substitution, e.g., using lower cost new graduates of anesthesia medical programs or nurse anesthetists or anesthesia assistants. The consolidators would also look to leverage other potential expense areas regarding overhead including lowering revenue cycle management costs, quality assurance costs and malpractice costs. On the providers side, the motivation is clear–prepayment of future, uncertain income. In addition, being part of a larger system may create opportunities for certain physician leaders within these groups, to take on larger roles in the clinical and business sides on a regional and national basis. Given the potential economic upside to the owner-provider, what are the downsides? Clearly, the Mednax example points to one downside—the inherent uncertainty in future prospects of the acquirer relative to the anesthesia marketplace. A second downside related to the providers could be related to the earlier discussed “hold-back” with that payment potentially being at risk depending on the success of the consolidator in the marketplace, as well as the group’s attaining its pre-negotiated objectives. The underlying contracts with the institutions could also be at risk, and depending on the terms of the employment contract, the providers ability to stay at that particular location post-termination could also be at risk. Young providers within the group, not yet risen to the owner status level, may become dispirited. It is no surprise that a provider’s motivation changes when they move from an independent practice status, with attendant incentives to work hard to become an owner and be rewarded no longer in play.  Hospitals may believe that, through employing anesthesia groups, they can exert more control over staffing models and coverage arrangements, as well as obtaining higher reimbursement rates from commercial payers, so they can theoretically provide a lower support to an employed group—as opposed to the stipend required by an independent group. Our experience in working with groups that were formerly independent and are now employed suggests otherwise. In fact, we have seen the required support paid by hospitals in order to cover their anesthesia services go up many multiples over what they were paying the independent groups. This, of course, may relate to the inherent incentives of a private group to work more hours than an employed provider. An employed provider has less incentive to work the additional hours unless they are paid for those additional hours. An independent provider will work additional hours because of the benefits of operating at a “reduced” staffing level, i.e., the ability to not hire an additional body but absorb that work within the existing complement of staff translates into additional compensation that can be shared with the core provider group. It will be interesting to see how the recent movement to employ anesthesia provider groups continues into the future given the potential for unforeseen additional costs associated with the employed model.

Hospitals may believe that, through employing anesthesia groups, they can exert more control over staffing models and coverage arrangements, as well as obtaining higher reimbursement rates from commercial payers, so they can theoretically provide a lower support to an employed group—as opposed to the stipend required by an independent group. Our experience in working with groups that were formerly independent and are now employed suggests otherwise. In fact, we have seen the required support paid by hospitals in order to cover their anesthesia services go up many multiples over what they were paying the independent groups. This, of course, may relate to the inherent incentives of a private group to work more hours than an employed provider. An employed provider has less incentive to work the additional hours unless they are paid for those additional hours. An independent provider will work additional hours because of the benefits of operating at a “reduced” staffing level, i.e., the ability to not hire an additional body but absorb that work within the existing complement of staff translates into additional compensation that can be shared with the core provider group. It will be interesting to see how the recent movement to employ anesthesia provider groups continues into the future given the potential for unforeseen additional costs associated with the employed model. The overall trend in the healthcare marketplace is for increasing employment of physicians either by hospital systems or by large corporate entities. This trend has accelerated during the pandemic, not surprisingly as a result of the increased amount of uncertainty surrounding the drop in patient volume and attendant incomes. This movement has translated into the anesthesia provider services as well. As noted, the large health systems have moved to employ physicians on a large-scale basis. We have also seen, perhaps, the beginning of a negative trend resulting from those consolidations (e.g., Mednax and other national providers) fully abandoning anesthesia or selectively abandoning anesthesia sites. Other hospitals have slowed plans to employ anesthesia groups as they see the increased costs associated with an employed model. In the meantime, salaries for independent and employed anesthesia providers are increasing significantly due to staffing shortages. For the independent practice of today, there are multiple avenues of support including external practice management companies that can assist in maximizing economic return to the group through commercial contract negotiations, expert revenue cycle management and expertise in hospital negotiations. Will this be a repeat of the nineties where the momentum of physician practice consolidation was reversed as a result of dissatisfaction with the resulting practices? We do not know. It is a trend we will continue to watch while this process unfolds. The old adage seems to apply to the ongoing anesthesia practice environment: “May you live in interesting times.”

The overall trend in the healthcare marketplace is for increasing employment of physicians either by hospital systems or by large corporate entities. This trend has accelerated during the pandemic, not surprisingly as a result of the increased amount of uncertainty surrounding the drop in patient volume and attendant incomes. This movement has translated into the anesthesia provider services as well. As noted, the large health systems have moved to employ physicians on a large-scale basis. We have also seen, perhaps, the beginning of a negative trend resulting from those consolidations (e.g., Mednax and other national providers) fully abandoning anesthesia or selectively abandoning anesthesia sites. Other hospitals have slowed plans to employ anesthesia groups as they see the increased costs associated with an employed model. In the meantime, salaries for independent and employed anesthesia providers are increasing significantly due to staffing shortages. For the independent practice of today, there are multiple avenues of support including external practice management companies that can assist in maximizing economic return to the group through commercial contract negotiations, expert revenue cycle management and expertise in hospital negotiations. Will this be a repeat of the nineties where the momentum of physician practice consolidation was reversed as a result of dissatisfaction with the resulting practices? We do not know. It is a trend we will continue to watch while this process unfolds. The old adage seems to apply to the ongoing anesthesia practice environment: “May you live in interesting times.”

Many anesthesia group boards meet late in the day after a full clinical load. Exhaustion can set in, and board members can be overloaded. This may result in work not getting done or make it more difficult to find individuals to serve on the board.

Many anesthesia group boards meet late in the day after a full clinical load. Exhaustion can set in, and board members can be overloaded. This may result in work not getting done or make it more difficult to find individuals to serve on the board.

A “policy” is a statement which guides and constrains the subsequent decision making. In setting policy, you try to specify the end rather than the means.

A “policy” is a statement which guides and constrains the subsequent decision making. In setting policy, you try to specify the end rather than the means.