Ten Weeks of COVID-19: A Look at Anesthesia’s Journey

Summary:

COVID continues to have an impact on anesthesia practices. A review of our clients' case volumes during the pandemic provides a picture of disparity, with some groups still grappling with the effects of the virus and others ramping back up to near normal case levels. This article provides insight on the current status and future outlook of anesthesia practices.

Two questions preoccupy the thinking of most anesthesia providers these days: what will the new normal look like, and how soon will we get there? Most of our clients are starting to see surgical volumes pick up after the unprecedented drop-off in early March, but there is a huge divergence. Some practices are almost back to where they were in January and February, but most are not. Clearly, multiple factors determine surgical volume. State COVID guidelines are just one aspect of the recovery. Even where elective cases are permitted, concerns about potential exposure still determine how willing patients are to schedule needed surgeries. Most surgeons are actively soliciting their patients to schedule recommended procedures but many report a certain degree of patient resistance. The fact is that we still don't have a handle on this pandemic, and the numbers are still going up in 21 states.

Past Impacting Future

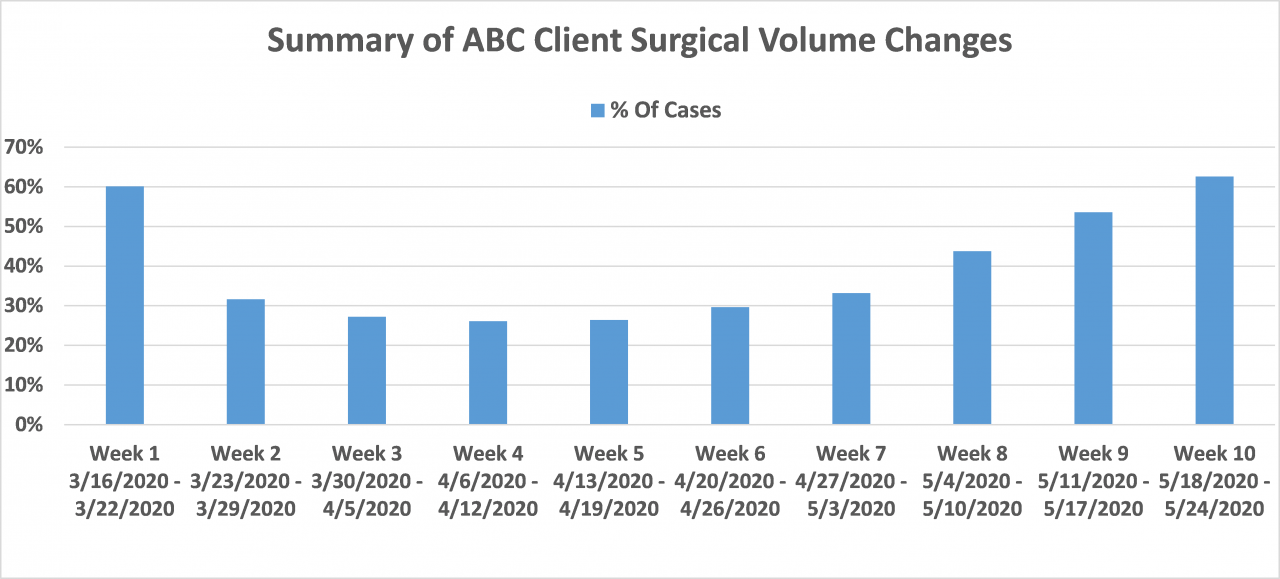

The chart below is a summary of ABC client experience for the first ten weeks of this pandemic, from March 16 to May 24. Based on our analysis, the average client is only back to 64 percent of typical weekly surgical volume after 10 weeks. Most have continued to see subsequent increases in surgical case volume, but this will be a gradual transition. This recovery notwithstanding, it is the drop in surgical volume in March and April that will most impact collections in June and July. Seeing fuller schedules is a good and positive sign. It is the reality of accounts receivable management, though, that it can take two to three months for the bulk of those expected receipts to be realized. This is just the reality of medical economics.

Road to Recovery

It is interesting to note how our clients are recovering from the dramatic drop in surgical volumes. As is true of so many aspects of anesthesia practice management, most clients are simply captive to the facilities they serve for surgical volume and collection. Only 13 percent of clients are back to 90 percent of pre-COVID surgical volume, and some of these are experiencing above average volumes as surgeons get caught up on procedures not performed during the pandemic peak. Some 22 percent appear to be on track for a solid recovery, having recovered to 75 to 90 percent of pre-COVID case volumes. Another 42 percent have only achieved 50 to 75 percent of pre-COVID volumes after ten weeks, and 23 percent are still at or below 50 percent.

What are the most relevant factors in this recovery? Location is probably the most significant factor. Demographics and payer mix are critical factors, as well. Affluent suburban practices with a strong base of commercial insurance appear to be leading the pack. The strongest practices have a solid base of surgery center business where their centers have been most active in ramping up surgical volume. As a general rule, most surgery centers and endo clinics are not filling their schedules so quickly.

Anatomy of Recovery

Certain common procedures that are typically done on an inpatient basis are now consistently being performed. Examples would include appendectomies and cholecystectomies. By contrast, male urinary procedures such as TURPs are still lagging well behind historical averages. CABGs have also been slow to come back.

Orthopedic procedures took a big hit in March. They are always a topic of considerable interest because they generally involve younger patients with better insurance. These cases also provide an additional revenue opportunity because of the use of nerve blocks. For the most part, though, these much-needed procedures are now being performed. The chart below is based on a global client sample of four common orthopedic procedures:

- *Knee arthroscopy

- *Shoulder arthroscopy

- *Total Hip

- *Lumbar spine fusion

So many practices have seen an expansion of their colonoscopy services over the past few years, but these cases are not ramping back up with any consistency. Most practices are only back to 40 percent of their pre-COVID levels. This appears to be a clear example of a non-urgent surgical procedure that patients are reluctant to schedule, especially if they consider themselves at risk, as so many Medicare patients do.

Many practices anticipated having to provide intensive care services to COVID-19 patients. As it turns out, this was needed only in certain states where the impact of the virus was most pronounced. The chart below presents a summary of ICU visits billed by month. Clearly, the trend is positive for May. Let us hope such cases continue to decline in June; although in reality the numbers were lower than expected.

The Road Ahead

Where does this leave our clients, and how do they plan for the future? While the coronavirus is a general challenge to all clients, an individual practice's situation is a function of many specific conditions. The reality is that most practices have little or no opportunity to impact volume and collections. The real challenge is that they must try to project a realistic ramp-up and adjust staffing accordingly. It is this reality that will have been the greatest challenge of this pandemic: reducing staffing for the duration of the crisis. How our clients have managed their staffing will be the subject of a future eAlert. If you would like assistance evaluating the impact of COVID-19 on your practice, please contact your account executive or email us at info@anesthesiallc.com.