March 9, 2015

The Supreme Court heard oral arguments in King v. Burwell, the case challenging the subsidies provided for health insurance policies through the federally-run exchanges, on March 4, 2015. A decision is expected in late June or early July. If the plaintiffs prevail—and no one is confidently predicting the outcome at this point—more than 7.5 million Americans may lose their insurance. Congress and/or the states could adopt legislation that would prevent or mitigate any loss of coverage, however. The uncertainty renders meaningful planning impossible.

Health policy dominated the news media last week, with the Supreme Court hearing oral arguments in King v. Burwell, the case with the potential to eviscerate Obamacare, on Wednesday March 4. Demonstrators crowded the steps in front of the Court during the hearing; most urged that the Affordable Care Act (ACA) be left intact.

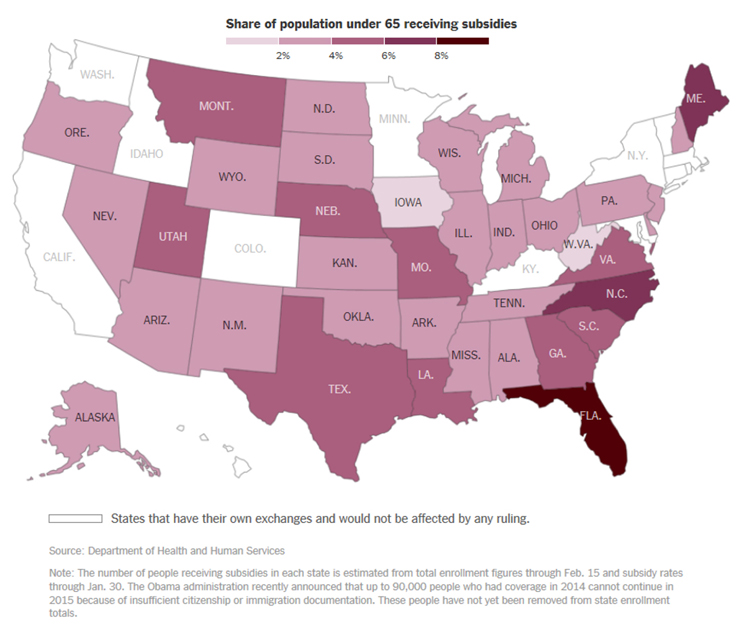

The interest in King v. Burwell is not surprising. If the Court decides in favor of the plaintiffs, between 7.5 and 8.2 million persons in 34 states that have not created their own health insurance exchanges stand to lose the coverage that they have been able to obtain because of the ACA subsidies. Eighty-seven percent of individuals who have signed up in the 34 states are eligible for subsidies, which average about $268 per month. Premiums are expected to increase by about 35-57 percent for those who remain in the federally run exchanges if and when many of the formerly subsidized drop out.

The 16 states that have established their own exchanges, and that will not be affected by the decision, are shown in white in the following map published by the New York Times:

The plaintiffs are challenging the subsidies available to individuals who have bought policies through the federally-established ACA health insurance exchanges. Specifically, they contend that the tax credits (or subsidies) are only available to individuals who buy health insurance on exchanges “established by the State,” as opposed to the exchanges established by the federal government, because of the wording of a single provision of the ACA. The Administration, on the other hand, maintains that the statute should be read as a whole consistent with the intent to make affordable health care coverage available as widely as possible.

This is far from the first Supreme Court decision that pits a strict construction of the legislative language against a contextual interpretation of statutory wording. The infamous Dred Scott decision of 1857, holding that a slave was a slave even when accompanying his owner in free states, is an example of the former; Brown v. Board of Education (1954), in which the Court found that racial segregation in public schools violated the Constitution despite the existence of “equal” facilities, is an example of the latter. King v. Burwell will not be the last confrontation between the two approaches.

Following last Wednesday’s hearing, it is not easy to predict whether the literal meaning or the presumed intent of the contested language will prevail. Chief Justice John Roberts, who authored the opinion that preserved the ACA when it was challenged in 2012, did not ask a single material question of the lawyers (the same ones who had argued the earlier case). Justice Anthony Kennedy was in the four-judge minority that would have found the ACA unconstitutional three years ago, but his questions this time appeared to cut both ways. His widely quoted comment to the lawyer arguing against the subsidies—that the narrow reading of the statute would improperly coerce the states by telling them to “create your own exchange, or we’ll send your insurance market into a death spiral”—suggested to many observers that Justice Kennedy would vote to uphold the ACA.

If, however, the Court decides for the plaintiffs and rules that the premium subsidies are not available in the states that are relying on federally-run exchanges, the consequences could be far-reaching. Then again, they might not, depending on how Congress or the states individually may react. Here are some possible developments if the subsidies are disallowed for coverage bought on the state exchanges:

- The 34 states could establish their own exchanges, although not immediately as a practical matter. Purchasers of policies on the new state-run exchanges would be entitled to subsidies.

- A likelier solution would involve a new type of partnership with the federal government or between states, such as a model in which the state creates the exchange in name but still relies on the federal government’s technology systems to run it. The exchanges in Nevada, New Mexico and Oregon have operated in that fashion. “Other workarounds that have been discussed include setting up regional exchanges that cover multiple states, or keeping the HealthCare.gov website operating as a place to sign up for insurance but allowing states to disburse the federal subsidies.” (Morgan D. What Will States Do If Court Kills Health Insurance Subsidies? Insurance Journal, February 19, 2015.)

- Congress could change the ACA, or come up with another solution. Few observers expect that this Congress will do more than continue to try to repeal the ACA, which federal legislators have now done unsuccessfully 56 times. We cannot resist noting, as did a columnist in the St. Louis Dispatch-Post on February 10, that a resolution now pending in the Missouri legislature calls on the state's congressional delegation to “endeavor with 'manly firmness' and resolve to totally and completely repeal the Affordable Care Act ....”

- In any and all of the 34 states that do not set up their own exchanges, the cost of coverage through the federal exchanges will probably increase significantly, since the ACA will continue to prohibit health plans from excluding or charging more for pre-existing conditions or for older patients, to require a defined “essential” benefits package and to set limits on out-of-pocket costs. Very few individuals will be willing or able to pay the full cost. Furthermore, according to the Urban Institute, “Medicaid and CHIP [Children's Health Insurance Plan] enrollment would be about 500,000 lower without tax credits and cost-sharing reductions. Many children eligible for Medicaid or CHIP have parents eligible for marketplace tax credits under the current implementation. Without tax credits, fewer parents would seek marketplace coverage and, as a result, fewer children would be screened for and enrolled in public insurance.” [Urban Institute, January 2015]

- Health systems and hospitals in some of the 34 states—particularly not-for-profit entities—may see a rebound in the proportion of patients who cannot pay their bills, leading to downstream consequences such as lowered credit ratings. Last year's increase in the number of patients with insurance helped many hospitals to increase earnings sharply.

The cash flow impact on physicians, including anesthesiologists and pain specialists, obviously will depend on the numbers of their patients who may become uninsured and unable to pay their medical bills. As Dori Zweig observed in King v. Burwell: Impact on healthcare industry (Fierce Health Payer, March 3, 2015), even if premiums rise dramatically, “the Affordable Care Act will not cease to exist. Other provisions within the healthcare reform law—such as the individual mandate and employer mandate—may pick up the slack in a post-subsidies industry. Both mandates would still require individuals to obtain coverage and employers to offer coverage; the market would just have to overcompensate to pay for the influx of new consumers.”

The Supreme Court’s decision is expected at the end of June or the beginning of July. Until then, there will no doubt be a good deal of speculation, but little information on which anesthesia groups or anyone else can base strategy. As soon as the picture becomes clearer, we will provide an update.

With best wishes,

Tony Mira

President and CEO