The ACA’s Impact on Healthcare Payment

Maurice Madore, MBA, CPC

Chief Client Officer, Anesthesia Business Consultants, Jackson, MI

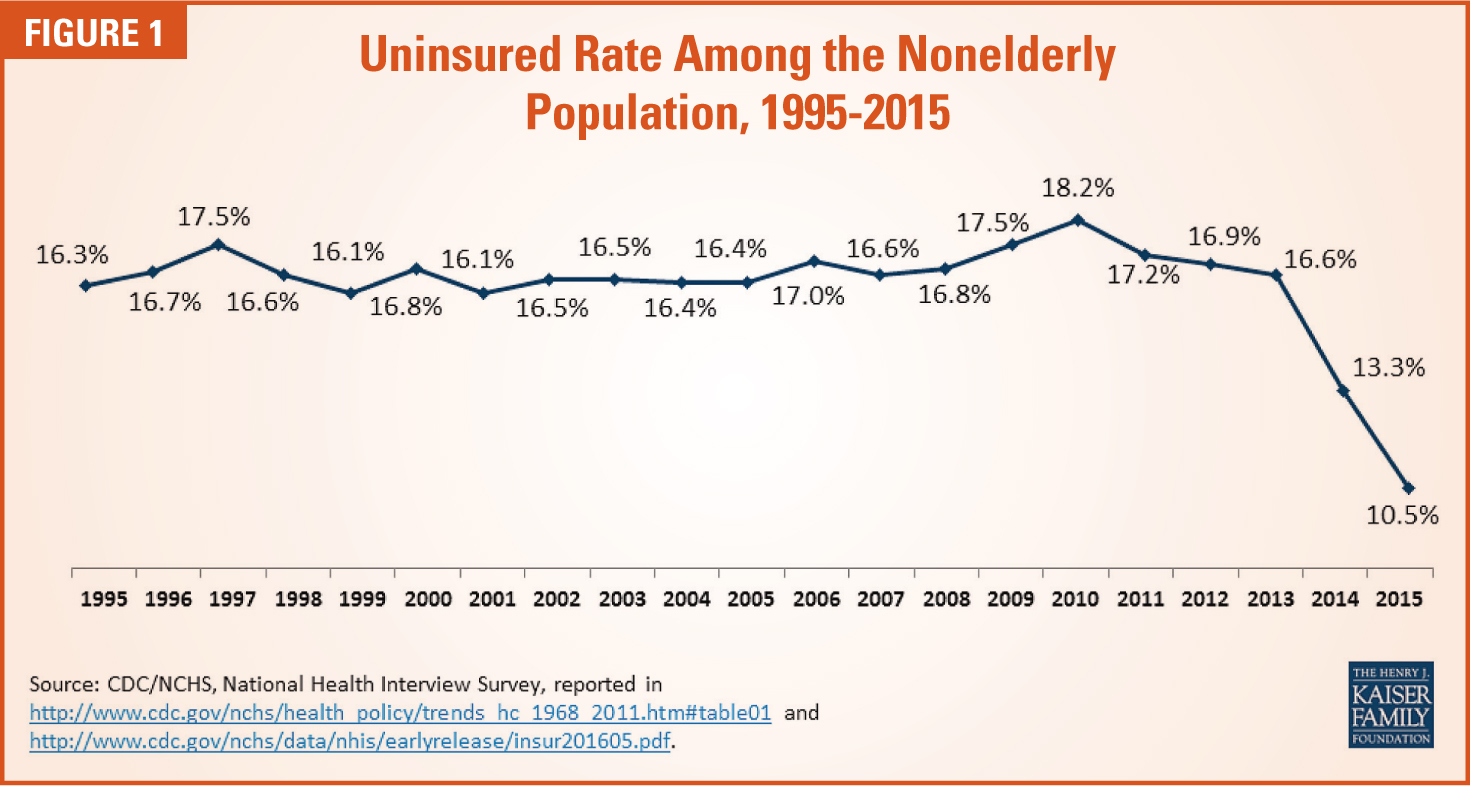

When the Affordable Care Act (ACA) was signed into law in 2010, it set into motion a series of intended and unintended actions and consequences that, after several years, can now be reviewed and interpreted. According to the Centers for Disease Control and Prevention, the number of uninsured in the United States has decreased from 15.7 percent in 2009, at the height of the most severe economic downturn in recent U.S. economic history, to about 9.1 percent in 2015.

While millions of people have gained coverage under provisions of the ACA that went into effect in 2014, over 28 million nonelderly individuals remained uninsured in 2015. Many of these people are ineligible for ACA coverage, either because of their immigration status or because their state did not expand Medicaid. Others may be eligible, but do not know of the new coverage options, have had difficulty navigating the enrollment process or have opted not to enroll. In addition, affordability, even with the availability of tax credits, remains a barrier for many. Uninsured adults continue to name cost as a major reason for remaining uninsured.1 The increase in the number of insured Americans was an intended impact of the ACA. But the ACA has had some unintended consequences as well. Hospitals and providers have been forced to restructure how they get paid for services as patients have become responsible for a higher percentage of their healthcare costs. Employers have offered more high deductible health plans (HDHPs) and fewer traditional policies. A look at the types of plans that many of us have personally chosen in our own places of employment verifies that this trend is real. In 2009, only about eight percent of employer-sponsored plans were of the HDHP variety. By 2015, that percentage had risen to 24 percent, according to Health Affairs.2

The Rise of High Deductible Health Plans

According to Towers Watson,3 in order to reduce their healthcare costs, 52 percent of employers now offer at least one type of HDHP and 22 percent offer only HDHPs. Many employees opt into these plans because of the significantly lower premiums. However, what many fail to consider is the high deductible that they will need to cover. Out-of-pocket healthcare costs have increased by 230 percent since 2009.

This increase in patient responsibility has important implications for providers. It was assumed that increasing patient responsibility for healthcare costs would lead to “shopping” by patients for low cost/high quality services. The reality of the shift from a traditional model to a shared cost model has been much different. Preliminary data show that employees with HDHPs are reducing their healthcare expenditures—but not because they have found lower cost/ higher quality services. Rather, the reductions in healthcare expenditures are more closely related to the tendency among a growing number of individuals to delay care and to delay treatment during the early stages of illness. Although longterm data is not yet available, studies by the National Bureau of Economic Research (NBER) give early indication of some interesting trends.

NBER followed several companies offering HDHPs to employees to examine how employees handle larger responsibility for their own healthcare costs. Employees were considered affluent, with median annual incomes of $125,000 to $150,000. The companies also provided financial assistance through health savings accounts (HSAs). Even with additional financial support, employees sought fewer services. Colonoscopies and mammograms decreased by 32 percent and nine percent, respectively, compared with previous periods when employees had access to low deductible plans. The researchers concluded that the behavior in this small sample might signal an emerging trend among employees with HDHPs who are shouldering a significantly larger portion of their healthcare costs. This shift in behavior could have long-term public health consequences. As more patients opt out of early screening and treatment, even for covered services, they will find themselves dealing with more serious illnesses and greater medical expenses.

The Bad Debt Dilemma

As the percentage of patients covered by these types of plans increases, the challenge to providers of collecting payments from patients will grow as well. PricewaterhouseCoopers (PwC) has estimated that in the next few years 44 percent of employers will offer only HDHPs—a 74 percent increase from 2010. Add enrollees in the federal and state-run marketplaces, in which HDHPs are the most popular type of plan and in which patients are responsible for as much as 30 percent of their healthcare costs, and it becomes clear that the industry is undergoing a major shift in how providers and hospitals are paid.

More data on this new paradigm comes from the hospital sector. Before 2011, the majority of payments collected by healthcare systems were from insurance companies and government agencies. In 2014, payments collected from patients had risen by 193 percent. It’s a number that can’t be ignored. And it tells only half of the story. The other half relates to the enormous amount of money that healthcare organizations and practices are not collecting from patients. More patients have not been paying their balances. These unpaid balances become bad debt.

A report from the American Hospital Association notes that more than $502 billion in uncompensated care—$33 billion annually—has been delivered since 2000.4 This number is expected to grow as health systems continue to experience increases in bad debt. According to McKinsey & Company, bad debt has increased by 30 percent since implementation of the ACA.

New Collection Strategies

The dual trends of increased patient responsibility and increases in unpaid balances have put a large financial strain on hospitals and physicians that has forced them to develop new revenue cycle management strategies. Some hospitals are creating teams of specialists to help patients identify their financial responsibilities before admission with the goal of securing some prepayment for elective care. However, the trend among patients to delay care has led to an increase in emergency department visits that hinders careful financial screening of patients before admission. In addition, emergent patients often receive out-of-network care. The inability, in these instances, to collect payment upfront increases the chances that these balances will not be paid.

Office-based physicians are trying some of the same strategies, including attempting to collect a portion of patient balances up front. Hospital-based specialties, including anesthesia, radiology and pathology, have limited opportunities to conduct these financial reviews because many services are not clearly defined prior to the delivery of care. A surgical patient may be under anesthesia longer than expected due to complications, or may need intraoperative x-rays or a pathology report. These patients may be unwilling to pay for additional services that exceed original estimates.

In an attempt to manage the revenue cycle, hospitals have developed revenue cycle management processes that focus on getting a clean claim to the carrier for processing. Some organizations focus on ensuring that claims are processed in a timely manner and that patients with high deductibles are processed when the carrier, rather than the patient, is responsible. This process was highly effective several years ago, when average deductibles were relatively low. As deductibles have risen, some providers have begun holding charges for longer periods, hoping to receive payments from carriers. This strategy has led to a practice among many providers of sending claims to patients much later in the billing cycle following the delivery of services—a practice that has led to patient complaints and increases in dissatisfaction. Billing company professionals, hospital administrations and group practice management staff have been carefully reviewing data and payment patterns in order to adapt to the changing environment and develop effective strategies.

Conclusion

In conclusion, hospitals and providers have had to change their billing and collection practices to adapt to major changes in the health plan market. More Americans are insured, but more are carrying HDHPs. The shift of more financial responsibility to patients has led more patients to defer care in order to avoid out-of-pocket costs and has increased bad debt among hospitals and providers.

The provision in the ACA for a “Cadillac tax” penalizing employer-sponsored plans likely would force more employers to offer HDHPs in order to avoid the tax. However, president-elect Trump’s promise to repeal the ACA has lessened the likelihood of that tax becoming a reality. Are we looking at another 2,000-page document to replace the 2,000-page document that we currently have? Rest assured that whatever the lawmakers in Washington draft, it will be a journey into the unknown. As healthcare professionals, we will be challenged to create a process that ensures payment from insurers and patients. As Larry Levitt, a senior vice president at the Kaiser Family Foundation, said in the Washington Post: “The Affordable Care Act, enacted in the spring of 2010 with virtually no GOP support, is a 2,000-page statute that has ushered in the broadest changes to the healthcare system in half a century. With Trump’s election, the ACA as we know it would seem to be toast.”

Only time will tell whether this will happen, and if it does, what the replacement package will look like.

1 Kaiser Family Foundation analysis of the 2015 National Health Interview Survey, http://kff.org/uninsured/fact-sheet/key-facts-about-the-uninsured-population/

2 Islam, Ifrad, “Trouble Ahead for High Deductible Health Plans,” Health Affairs Blog, October, 7 2015, http://healthaffairs.org/blog/2015/10/07/trouble-ahead-for-high-deductible-health-plans/

3 Brandelsky, Karen, “The Hidden Risk of High Deductible Health Plans,” Time/Money, November 3, 2015, http://time.com/money/4091524/health-insurance-high-deductible-plans-risk/

4 American Hospital Association, Uncompensated Hospital Care Cost Fact Sheet, January 2016, http://www.aha.org/content/16/uncompensatedcarefactsheet.pdf

Maurice (Moe) Madore, MBA, CPC serves as Chief Client Officer for Anesthesia Business Consultants. Mr. Madore has over 30 years of experience in healthcare and business administration, including operations of billing centers, management, strategic healthcare planning, business financial planning, marketing new business development, and physician recruiting and practice management. Prior work experience included six years as a vice president of medical affairs at a regional medical center in Maine. He can be reached at Moe.Madore@AnesthesiaLLC.com.

Maurice (Moe) Madore, MBA, CPC serves as Chief Client Officer for Anesthesia Business Consultants. Mr. Madore has over 30 years of experience in healthcare and business administration, including operations of billing centers, management, strategic healthcare planning, business financial planning, marketing new business development, and physician recruiting and practice management. Prior work experience included six years as a vice president of medical affairs at a regional medical center in Maine. He can be reached at Moe.Madore@AnesthesiaLLC.com.