eAlerts

-

The Road Not Taken

Jody Locke, CPC

Vice President of Anesthesia and Pain Management Services, Anesthesia Business Consultants, Jackson, MIOne of Robert Frost’s most popular poems is The Road Not Taken. It is about two paths that diverge in the woods. It is a wonderful and powerful metaphor for the decisions we make in life. By selecting one option we inevitably forgo another. More often than not this results in endless speculation as to whether it was the right choice. And so it is with the strategic decision to sell one’s anesthesia practice. The allure of being part of a bigger, stronger and better-managed entity is a powerful draw but does it really result in a more secure practice situation? That is the question of the day.

Anesthesia providers are a curious breed. They are credited with having the shortest decision cycle in medicine. They routinely make critical life and death decisions in a matter of seconds. Ironically, despite their facility in the operating room, when presented with major strategic decisions pertaining to their practice they often freeze like deer caught in the headlights. One can explain this on the basis of their training, which involves clinical decision trees that have been assiduously memorized. In other words they perform consistently in the known environment of the operating room and delivery suite. We often joke that physicians and CRNAs are not business people. Although some are, many have simply focused their energy on their professional training and clinical skills. Such an intense focus on managing patients safely through the trauma of surgery has resulted in a population of providers who tend to be extremely cautious and risk-averse in their personal and business lives. Their comfort zone is defined by the operating room and the processes over which they have learned to exercise a modicum of control.

Anesthesia providers are known for their independence. For them anesthesia is both art and science; a unique creation that responds to the unique requirements of patient, surgeon and surgical procedure. Some have suggested that even the notion of an anesthesia practice is an anachronism. Most anesthesia groups operate more as professional business fraternities than as rigorous business entities. The typical American anesthesia practice provides just enough structure and focus to ensure a viable franchise that collects an adequate income to provide a reasonable income to its members without imposing any undue constraints or limitations on the clinical activities of its members. For most, partnership or shareholder status is the medical equivalent of tenure where cause for termination is almost unknown.

How curious is it, then, that so many of these loose confederations of providers are willingly and eagerly selling out to aggregators which offer so little in the way of long term security or protection? What does this say about the current state of healthcare in this country? What does it say about the nature of the specialty and its practitioners? What is the problem to which selling one’s practice is the perceived best alternative? And when a practice decides to merge or sell out, how do its members know they have chosen the best path? There is a lot of wishful thinking in such decisions, but more than anything it is blind faith since no one can really predict the outcome.

Such change can only be motivated by fear or hope, and in the case of what is taking place in the specialty of anesthesia, it is obvious that fear is the predominant motivator. Consider some of the most significant recent developments in U.S. healthcare. There is nothing to reassure providers that things will work out for the best. Just the opposite occurs, from a provider’s perspective; each new regulation, consolidation or proposed quality metric only reinforces a perception that the system is out of control. More service will be required for less pay.

If U.S. healthcare is a boat that has been quietly cruising a predictable course these past few decades, most would agree that it has suddenly been thrust out into uncharted waters. The passage of HIPAA was the first wake-up call. While compliance had been a topic of discussion prior to 1996, the year of HIPAA’s enactment, it became a major concern. One could even say that U.S. medicine has evolved through three phases over the last few decades. In the seventies and eighties one collected what one billed. In the late eighties and nineties managed care changed the rules of engagement so that one got paid what one negotiated. Now it can be said—with only slight exaggeration—that one gets to keep what does not get taken away in a compliance audit.

While most physicians could deal with the implications of HIPAA, the passage of healthcare reform and the implementation of the Affordable Care Act, aka Obamacare, has been an entirely different matter. It is the very nature of the legislation that it presupposes structural changes in the market for healthcare, few of which are actually defined. At every level of healthcare delivery entities are struggling to envision a future that is as clear as the forest paths Frost described and to position themselves to be serious players. Never has U.S. healthcare seen such an explosion of activity. Two themes appear to be driving all the strategic considerations: quality and cost, for the underlying assumptions of Obamacare are that U.S. healthcare is too inconsistent and too expensive. Americans pay a huge premium for less than optimum care.

While most physicians could deal with the implications of HIPAA, the passage of healthcare reform and the implementation of the Affordable Care Act, aka Obamacare, has been an entirely different matter. It is the very nature of the legislation that it presupposes structural changes in the market for healthcare, few of which are actually defined. At every level of healthcare delivery entities are struggling to envision a future that is as clear as the forest paths Frost described and to position themselves to be serious players. Never has U.S. healthcare seen such an explosion of activity. Two themes appear to be driving all the strategic considerations: quality and cost, for the underlying assumptions of Obamacare are that U.S. healthcare is too inconsistent and too expensive. Americans pay a huge premium for less than optimum care.Capital has a curious way of finding its way into such situations. Investors love to think that one man’s challenge is another’s opportunity. Businessmen are eager to bring order to the chaos of healthcare. The amount of venture capital that has flowed into the specialty of anesthesia in recent years is impressive. It is the availability of such capital to buy and aggregate anesthesia practices that is so dramatically changing the landscape. Obviously there are those who believe that the application of better management will result in better, cheaper and more profitable healthcare. By all accounts, however, one must acknowledge that the proposed outcome is still much more of a concept than a reality.

The current environment has given new life to an old aphorism. The beliefs and strategies that have gotten us to where we are today will not get us to where we want to be tomorrow. American anesthesia providers have always believed that if they consistently provided quality care all the rest of their issues would take care of themselves. Ironically, they may have done too good a job. Quality is now a given. Anesthesia care has become a commodity.

And so anesthesia providers have become increasingly anxious about the future of their practices. They are starting to feel impotent, that the game is rigged, that they cannot compete with bigger,slicker and more aggressive competitors. And so they ask themselves, is bigger better? With increasing frequency they conclude that it must be, not because they know this to be true, but because it appears to be the only alternative.

As scientists, anesthesia providers like to analyze things objectively. The art of administering anesthesia is based on a feedback paradigm where the availability of reliable data about a patient’s physiology allows for effective decision-making. How, though, does one make business decisions when the desired feedback is so illusory and delayed? While the desired outcome of each anesthetic is clearly defined a priori, what is the desired outcome of strategic decision-making? Thoughtful observers suggest three:

- Job security

- Increased income for work performed

- Control over one’s destiny

If the motivation to sell or merge one’s practice is concern for the future, which is the most common concern of most practices today, then this requires careful due diligence. While it is true that larger entities have the ability to ensure providers will have work, they cannot necessarily guarantee any specific work situation. There is growing evidence that hospital administrations are increasingly concerned about the power of anesthesia mega-groups. Many an anesthesia practice has aggressively pursued a merger or acquisition only to learn that such an act would result in termination of the contract.

While it is true that large anesthesia practices have the ability to negotiate better rates with payers, this does not necessarily translate into better physician or CRNA compensation. For those entities that are investor owned, increased contract rates are viewed as integral to generating profits as is the ability to drive down the cost of providing care. Most observers agree that the more aggregation that occurs in anesthesia, the more this will result in reduced provider compensation. The strategy is simple. Today’s aggregators offer new graduates lower salaries but predictability in lifestyle, a formula that seems to be playing well. What they also offer is a career path for those who have management ability. The formula ties the reward of higher compensation to the risks of managing other providers and reducing the overall cost of care.

And to the third litmus test, control over one’s destiny, what is the impact of adding one’s name to a longer list of providers? Clearly it diminishes an individual’s influence or control, unless that individual is politically astute and can be an active member of the management team. But this objective may actually be a chimera. While anesthesia providers love to think they have a certain degree of autonomy and independence, this probably only refers to what happens within the four walls of the operating room. Outside the O.R. no specialty is more captive to the requirements and expectations of its customers.

So why do so many practices and providers so willingly give up what seemed so important to them? Quite simply, most have come to believe they have no alternative, or at least no better alternative. Many may be right but most are simply unwilling to make the changes necessary to meet new market conditions. This perspective is consistent with the long-held belief that all that really matters is good outcomes. Most practices that see themselves as being vulnerable or at risk could probably fix their practice and secure their own future. To do so would be a challenge. What happens instead is that they let someone else impose a better solution.

There is a classic admonition that one will never get rich working for someone else. Most anesthesia providers do not pick the specialty to get rich. Most pick the specialty because they are fascinated by the science, like the work and want to make a difference in patients’ lives. They see themselves as problem-solvers and decision-makers. It is ironic that the very skills that make most anesthesiologists and CRNAs so effective in the management of their patients don’t get applied to the management of their practices. Some large anesthesia practices and aggregators appear to have developed a successful formula for success but these are the exceptions. Many others are still focused on getting big without really having formulated a strategy to ensure security, income and control of destiny.

Ultimately, this is a classic buy-ormake decision. We pay for a service that we cannot provide for ourself. Anesthesia practices either do their own billing or they outsource it to a vendor. The decision to sell or merge should be viewed through the same lens. If the proposed solution does not create more value than you could create yourself then you might be deluding yourself by thinking it is a better option. Frost was prescient. How often do we pick a path just because we think it will be better or easier and how do we know whether it was the right path? That is the question that will haunt us for years to come.

Jody Locke, MA serves as Vice President of Anesthesia and Pain Practice Management for ABC. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He will be a key executive contact for the group should it enter into a contract for services with ABC. Mr. Locke can be reached at Jody.Locke@AnesthesiaLLC.com. -

The Perioperative Surgical Home: Of Economics and Value

Rick Bushnell, MD MBA

Director, Department of Anesthesia, Shriners Hospital for Children, Los Angeles, CA and Huntington Memorial Hospital, Pasadena, CA“If someone offers you an amazing opportunity but you are not sure you can do it, say YES, then learn how to do it later.”—Sir Richard Branson

Presented with inevitable change and opportunity, how will each of our anesthesia groups create its own future? Will you continue to commit yourself to fading traditional practice patterns and payment models? Or will you take advantage of the paradigm shifts that are already upon us?

Payers are demanding better results. The Centers for Medicare and Medicaid Services (CMS) is willing to pay. Our hospitals are begging for physician leadership and our surgeons will need anesthesiologists more than ever. Best of all, proactive physicians in the American Society of Anesthesiologists (ASA) are pointing the way. There is every reason for a great future...depending on how you respond to the challenges.

CMS has been encouraging coordinated care and quality through the Physician Quality Reporting System and the Value-Based Payment Modifier. Those programs, along with the Meaningful Use (EHR) incentive program, will be replaced on January 1, 2019 by the Merit-Based Incentive Payment System (MIPS) and Alternative Payment Models (APMs). CMS will pay up to a four percent bonus for high self-reported MIPS scores and up to a four percent penalty for poor performers, beginning in 2019. In 2019, therefore— assuming that the overall amount of penalties assessed offset the amount of bonuses, in budget-neutral fashion—the difference between maximum positive and negative scores will be eight percent and by 2022 the difference will be 18 percent—every single year. Might I ask what return on your business investment do you need? When did you achieve that return on your personal investment portfolio? Private payers are sure to soon follow suit, but this 18 percent CMS incentive alone is strong enough that anesthesiologists should fully embrace MIPS quality and coordinated metrics. As for APMs, if you receive a “significant portion” of your Medicare payments through an eligible APM entity, you will be totally exempt from the MIPS requirements. As a “qualifying APM participant,” you will receive a five percent bonus in each of the five years between 2019 and 2024. From 2026 onward, you will be eligible for 0.75 percent increase in your annual Medicare payments—half a percent more than physicians who merely satisfy MIPS.Our hospital administrative partners, who are subject to their own increasingly important value incentives, are begging for anesthesia’s help. If they haven’t yet realized the value of your perioperative skill set, then it’s time for you to offer to show them. Administrators are overworked, under-inspired and dealing with their own mandates to coordinate care and share outcomes data. Hospitals are also subject to their own system of CMS penalties, caps and bundled payments. You may not personally know it yet, but your management and vision are in demand and needed outside the operating room. Your new management target is the 20 percent of sickest patients presenting for surgery. These are the patients at highest risk for readmission and anesthesiologists need to see those patients in clinic beforehand. This is the time and place for medical leadership.

Fortunately for our specialty, the ASA is pointing the way to the concept of the Perioperative Surgical Home (PSH). For the ASA, this is the moral and medical core of the future of our specialty. Who better than anesthesiologists to understand the physical challenges posed to patient physiology by surgery? Who better to coordinate the preoperative work-up, the acute intraoperative care and the post-discharge medical management? Establishing an Anesthesia PSH clinic is medically and politically valuable to your group.

Then that pesky, repetitive, timeless question arises, “But how do I get paid for being in clinic?” If perioperative management of the sickest patients is such a great thing, who is willing to support that anesthesiologist? Will CMS and private insurance pay; will anesthesia groups internally reimburse and will hospitals share the savings back with anesthesia groups?

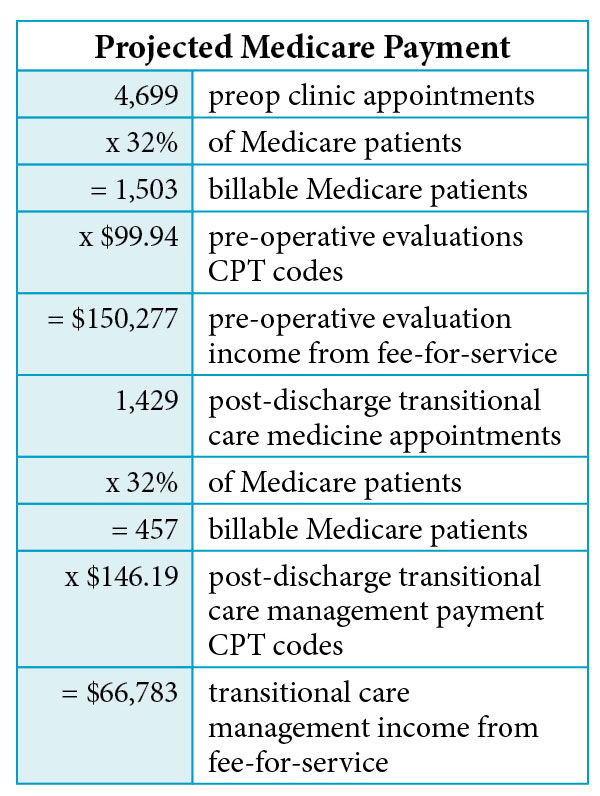

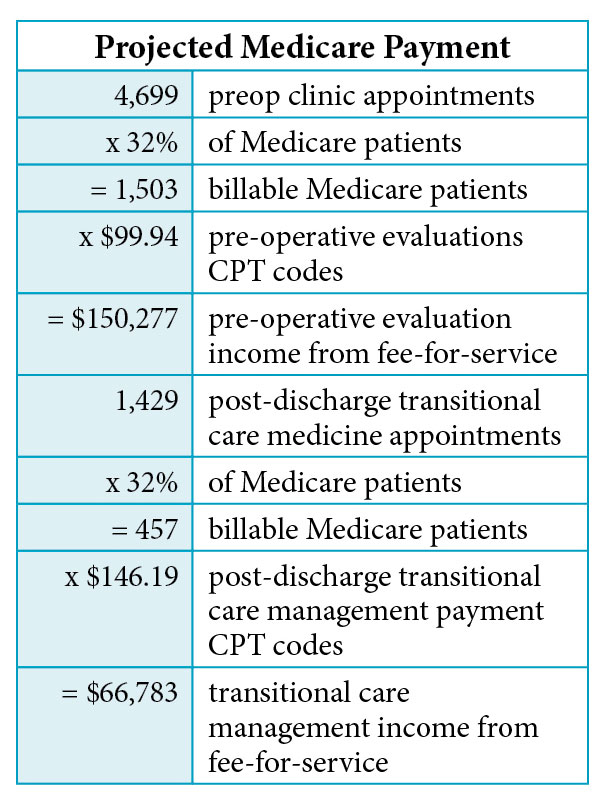

Believe it or not, CMS is willing to pay. “Yes,” there are fee-for-service codes. “Yes,” they will pay for both preop and post-discharge management. “Yes,” you can use these codes for your clinic time. And just as you suspected, “No,” it’s not enough. But let’s explore the initial math of fee-for-service clinic appointments.

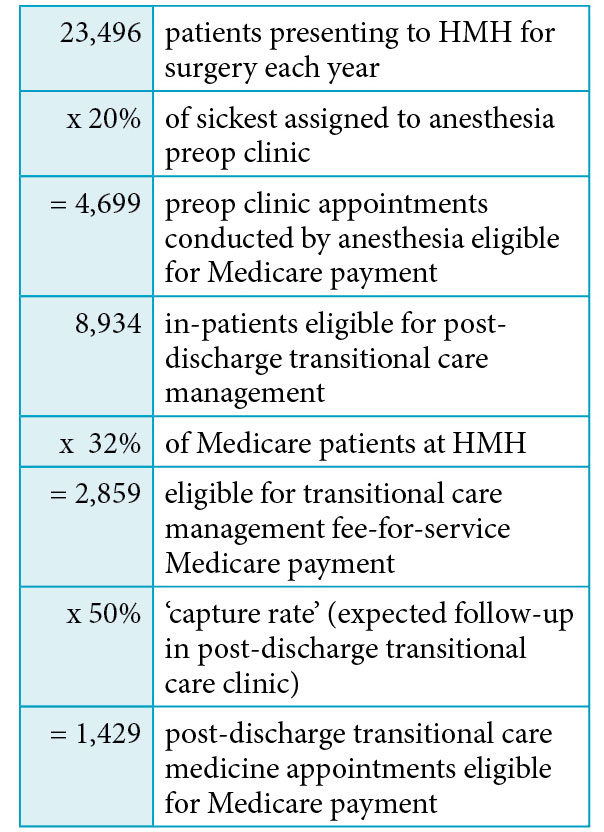

Consider our southern California hospital, Huntington Memorial (HMH), with 14,562 outpatient and 8,934 inpatient surgeries per year (total 23,496). Because of our PSH proposals, HMH will strongly encourage surgeon triage and risk stratification of these patients. HMH will soon mandate the appearance of all patients in preop clinic before elective surgery and assign the 20 percent of sickest to be seen by an anesthesiologist. Our Pacific Valley Medical Group (PVMG) anesthesia group will station one full time equivalent (FTE) anesthesiologist in clinic targeting the 20 percent of sickest patients, clearing, medically optimizing or canceling them as indicated. The goal is for our anesthesiologists to also see these same 20 percent of sickest patients in post-discharge clinic.

So based on the assumptions below,* let’s do the math on just three of the various revenue streams that could be used to support our private practice, full-time equivalent PSH clinic anesthesiologist.

The Fee-for-Service Payment Model:

CMS Payment for Pre-Operative Evaluations Current Procedural Terminology (CPT®) Codes for Los Angeles (locality #0118218) in 2016:

Post-Discharge Transitional Care Management Reimbursement Codes:

For the purposes of the revenue projection below, we’ll assume an average mix of CPT codes submitted to CMS. Let us also assume Medicare patients constitute 32 percent (actual HMH payer mix) of clinic appointments.

Using the above averages to project Medicare perioperative clinic payment:

Anesthesiologists should understand these codes and their associated compliance criteria.

At-Risk Medicare Payments to Anesthesia Practice, 2019-2022 Onward

Groups must quantify the contribution of the PSH to their practices. The Medicare MIPS at-risk numbers for our PVMG anesthesia practice are:

Assuming that PVMG qualifies for the maximum MIPS amount in each of the five years 1919-2023:

Anesthesia groups should be willing to invest a portion of their at-risk revenues to comply with CMS quality and practice mandates.

Costs to Hospital of Preventable Readmissions

Hospitals must quantify the contribution that anesthesiologists can make to hospital cash flow. The Medicare preventable readmissions at-risk numbers for HMH are:

The total potential savings to HMH is projected to be $1,056,684 over three years which justifies PSH support for anesthesiologist involvement. This incentive projection peaks around $100,000 in the third year and is used in summary calculations below.

Hospital Savings Accrued through Decreased Length of Stay**:

New York University (NYU) School of Medicine has now demonstrated that patients who attend their preop evaluation clinic have significantly shorter length of stays (LOS) and observed-to-expected LOS ratios than those who do not attend clinic.

For the NYU study’s financial analysis, 28,828 surgical encounters were included. There were 17,593 patients who attended clinic and 11,235 who did not. The mean variable direct cost per case was $5,754 for patients seen in the preoperative clinic and $7,127 for those who were not. The resulting savings were more than $1,373 per case.

Assuming much and applying the NYU numbers to HMH’s Medicare population: Hospitals should be willing to invest and incentivize to support the PSH FTE anesthesiologist in the PSH in an attempt to lower readmission rates and costs.

The Total of Annual At-Risk and Potential Cash Flows Available for Support:

This is our bottom line result using only a Medicare population (32 percent of inpatient surgeries). Certainly if we included private payer patients, the total potential savings and cash flows would be much larger. Based on these financial calculations, hospitals and practices have all the financial motivation they need to form joint ventures.

Possibly more important, you now have an objective analytic process by which to work your own numbers. By projecting your own practice’s contribution, you can approach your own Accountable Care Organization (ACO) with objective financial cause for an appropriate percentage of future bundled payments. An anesthesiologist presence in the PSH is negotiating power.

My strong suggestion is that hospitals and anesthesia practices contribute to a financial plan that supports one FTE clinic anesthesiologist. The joint hospital/practice financial plan should be monitored closely by all parties and adjusted accordingly. The stated goal of the financial plan should be an effective system of incentives and support, not an excessive revenue stream for the anesthesia practice or physician. Excess funds should be qualified and retained in a separate pool for use as additional personnel or performance incentives.

Your Own Amazing Opportunity

You now have my calculations, projections and suggestions for generating payment support from three categories of PSH cash flows. It may take a bit of financial creativity, but the combination of fee-for-service, shared CMS savings and hospital incentives should be enough to support one FTE anesthesiologist in the PSH. A well-constructed financial plan should get most organizations to that point. But allow us to conclude by considering a calling.

At the beginning of this article, Sir Richard Branson spoke of taking advantage of “an amazing opportunity.” His reference was to business and finance. Surely those issues are important, but consider what an amazing opportunity the PSH is for medical leadership.

Anesthesia is naturally positioned at the logistical and medical nexus of surgical challenges presented to both the patient and the healthcare system. It is my postulate that this position obligates our specialty to exercise greater medical leadership than we have lately assumed. Thirty years ago patients were admitted for surgery the night before and stayed a week after the procedure. We rounded on our next day’s patients the night before and called on them the day after surgery. Today we meet complicated patients three minutes before surgery and seldom round on them afterward, if they are admitted at all. We’ve allowed ourselves to become anonymous and our reputation often now suffers from invisibility. We are often being replaced by mid-level care providers.

The PSH is the perfect position from which to reclaim the medical authority that has slipped away from anesthesiologists. We can only reassert the great value of our specialty by practicing our medical and management skills thought out the entire continuum of the perioperative surgical process. Stepping up to assume our share of the responsibility for outcomes will naturally give rise to the credibility only medical leadership can confer.

Greater anesthesia involvement promises increased day-of-surgery efficiencies, increased rapport between services, better outcomes, increased patient satisfaction and the elevated perception of our specialty. How could these things not flow from our greater ownership of all the obligations of our position? We already know we can do better than relegating ourselves to three minutes before surgery and one minute after. It is now time to pick up this cause and to once again own all of our obligations. This is the reclamation and maturation of our specialty.

It is my personal challenge that you value the opportunity for medical leadership above all cash flows. Your physician presence in the PSH is your own “amazing opportunity.” As an anesthesiologist, this is the platform upon which to practice your entire medical skill set and to exert your medical leadership.

In the fourth article of this series, which will appear in the summer issue of the Communiqué, let us consider the future of the Perioperative Surgical Home.

*Assumptions and Caveats: Some aspects of CMS programs are beyond the scope of this article. For the cause of simplicity and to focus on the major issues, many details and arguments have been reserved for another conversation. Please accept the assumptions below that we have made for the sake of analysis here.

- The limitations of data access necessarily confine this analysis to publically available Medicare data. Private data have not been included. More complete individual analysis should include billing company, individual practice and hospital data that is inclusive of private payer reimbursements.

- The stated, targeted goal is to have our anesthesiologist attend to the 20 percent of sickest patients is an arbitrary number. That number will not be initially achievable for many reasons, principally the challenge of volume. Totaling the projected pre- and post-op clinic appointments and dividing that number into the available days results in the clinic anesthesiologist attending to 23 appointments per day. This number is not feasible and reductions of volume based on actual clinic volume will likewise reduce fee-for-service revenue projections.

- Not all MIPS or APM scores will or can be improved by the PSH. It is assumed that commitment to the high level of coordinated care it takes to manage a PSH will lead naturally to commitment to all areas of quality scoring and reporting. Credit the PSH with leadership.

- Conversations concerning MIPS, APMs and Value-Based Purchasing will be taken up in another article.

**Preop Evaluation Clinics (PEC) Reduce Readmission Rates and Hospital Stays, Clinical Anesthesiology, March 23, 2016. http://www.anesthesiologynews.com/Clinical-Anesthesiology/Article/03-16/Preop-Evaluation-Clinics-Reduce-Readmission-Ratesand-Hospital-Stays/35555/ses=ogst

Rick Bushnell, MD, MBA is the Director of the Department of Anesthesia, Shriners Hospital for Children, Los Angeles, CA and a Clinical Anesthesiologist at Huntington Memorial Hospital in Pasadena, CA. Dr. Bushnell graduated from the University of Illinois College Of Medicine and attended the University of Pittsburgh Medical Center, Pittsburgh and Loma Linda University for internship and residency. He has been with Pacific Valley Medical Group since 2003 and consults with Shriners Hospital for Children, Los Angeles. He and his partner have six adopted children in Tanzania where he serves as Visiting Clinical Anethesiologist at St. Elizabeth’s Hospital for the Poor in Arusha. He can be reached at propofolstingsme@gmail.com.

-

Owning Our Future

Deciding on new models for an anesthesiology practice is one of our very biggest challenges. It is not realistic for anesthesiologists to continue believing that if they consistently provide good quality care, all of their financial and business issues will take care of themselves. “The beliefs and strategies that have gotten us to where we are today will not get us to where we want to be tomorrow,” as ABC Vice President Jody Locke writes in his article The Road Not Taken in this issue of The Communiqué.

The transition to value-based payment, combined with the strong trend toward larger anesthesia groups and tight affiliations with national anesthesia companies and/or with health systems, has changed the landscape for traditional independent practices. Bill Britton sums up the current environment in Critical Issues to Consider When Exploring the Sale of Your Practice: hospitals are facing mounting pressures to minimize operating costs, including the costs of subsidizing anesthesia groups; coordinated care is pressuring margins, and uncoordinated quality reporting mandates are increasing operating costs for all.

Mr. Britton, who runs a private equity firm he co-founded, believes that it will become more and more difficult for anesthesia groups to remain independent and that every such group “should begin discussing preparation initiatives that will streamline operations, reduce costs, improve financial transparency, and other specific measures to increase their overall enterprise value.” It may be tempting to consider employment by the hospital or a bigger group, but this option does not realize the equity value of the practice. He urges group leaders instead to consult with the “right M&A advisor” to steer them through the six- to twelve-month process of negotiating a one-time sale to a strategic partner.

A very different option comes from Rick Bushnell, MD, MBA who is working with his hospital in Pasadena, CA to put in place a perioperative surgical home (PSH). An anesthesiology group that, like Dr. Bushnell’s, offers its hospital partner a solid PSH may secure its place with that institution at least for the medium term while CMS rolls out the Merit-Based Incentive Payment System and other pay-for-value programs. In the third of his series of articles on the experience, The Perioperative Surgical Home: Of Economics and Value, Dr. Bushnell lays out the calculations for revenue streams that will help to support the PSH taking shape at his facility.

There are some difficult decisions to be made. Mr. Locke’s article is a plea to groups to be very sure whether to sell or merge or whether to fix one’s own practice, through a PSH or any other strategy that truly enhances the value of the practice.

Will Latham, MBA, CPA explains in detail how to improve an anesthesiology group’s board meetings and decision making in his article Strengthening Your Board. This manual could not be more timely as the pace of change continues accelerating. As evidence of that pace, Computer-Assisted Personalized Sedation—The Beginning of the End of the Anesthesia Provider? by Steven Boggs, MD, MBA was written just before Ethicon ended sales of the Sedasys® system. Dr. Boggs used the opportunity to remind us all that anesthesia providers are going to remain indispensable for the foreseeable future. What technology could replace their combination of “deep technical expertise, human flexibility, problem solving [skills], creativity and compassion?” Once again, we salute the professions of anesthesiology and nurse anesthesia.

With best wishes,

Tony Mira

President and CEO -

Confidentiality in the Peer Review Process: What Does it Mean and What is Covered? Part II

Neda M. Ryan, Esq.

Corporate Compliance Attorney, Anesthesia Business Consultants, Jackson, MIIn the Winter 2016 issue of The Communique, we offered Part I of a summary of state laws (Alabama through Iowa) involving the peer review process. Here we are continuing that summary with the remaining states (Kansas through Wyoming).1

1Special thanks is given to Amy Bell for her assistance in preparing this article.

-

Critical Issues to Consider When Exploring the Sale of Your Practice

Bill Britton

Co-Founder and Managing Director of Cross Keys Capital, LLC, Fort Lauderdale, FLGiven the heightened level of interest in acquisitions of independent anesthesiology groups, physician shareholders are being confronted with a myriad of questions. Many are finding that anesthesiology groups in the local region are being acquired by larger medical groups. What should their practice do? What would be the value of their practice if they sought to be acquired? What does the acquisition process look like and how could maintaining a steady course of non-action not result in the best long term outcome?

Your Practice has Equity Value

Over the years, long-standing relationships have been developed with other healthcare providers and service contracts have been established with medical facilities, securing work for all the practice-employed physicians. A practice will accumulate a substantial amount of sweat equity, which has an equally substantial amount of economic value associated with it. Opportunity currently exists to monetize the value of this equity, and depending on regional market activities and the overall global economy, this opportunity may not always be available or as lucrative as it can be today.

Uncertainty is Prevalent

Anesthesiologists are currently enjoying high and steady market compensation rates with incomes that fall in the upper echelons within the healthcare physician provider spectrum. However, considering the current landscape of the industry these statistics likely won’t maintain their relative position forever—especially in markets that are experiencing consolidation since rates will become more competitive, resulting in downward pressure.

As hospital service contracts come up for renegotiation through the RFP process, practices entrenched in these hospitals may find their subsidies and other benefit offerings thinning. Hospitals are facing increasing pressures to minimize operating costs and are being met with an increasing number of alternative providers as options to obtain necessary services. These alternatives are becoming bigger, more competitive and are offering more benefits to the hospitals, making the market as a service provider that much more competitive.

Additional uncertainty over reimbursement rates and models is increasing. Coordinated care is pressuring reimbursement rates down. The industry is experiencing a shift from fee-for-service to pay-for-performance, increasing burdensome requirements to report and maintain quality metric levels by the practice, resulting in greater operating costs and impacting smaller practices disproportionately to larger ones.

Bargaining Power

The industry is at a point in its life cycle when size matters, and many of the large buyers are bundling different physician and multispecialty services to gain critical mass and achieve greater bargaining power for contracts and resources. The regulatory environment is becoming increasingly tumultuous with recent legislated healthcare reforms, such as bundled payments, pay-for performance, value-based purchasing and accountable care organizations.Partnering with a larger organization in most cases provides your group access to greater resources, existing infrastructure and established business platforms to help address these challenges today, as well as the unforeseen obstacles that will arise in the future. It gives practices the support they need to negotiate with insurance carriers to improve (or at least maintain) current reimbursement rates. They have people whose full-time jobs are to look at managed care, figure out contracts and manage the collection of quality data that is used to improve outcomes. Sophisticated, tried and true systems are in place to process billing and insurance claims and manage administrative functions to improve the overall process without having groups solve these problems on their own. Physicians can focus on their clinical responsibilities without the administrative burden or managing the practice; overhead costs can be lowered.

Status Quo

The evolution of the anesthesiology industry is heading in a direction where the smaller, independent physician practice will encounter difficulties in competing with bigger and more capable competitors in the upcoming future. At the very least, this will result in a decrease in overall profitability. To maintain parity with today’s levels, a group would need to experience an increase in reimbursement rates and/or growth in the practice’s customer base, either via organic or inorganic growth maneuvers (pain clinics, ASCs, etc.) or through vertical integration (multi-specialty practices).

Inevitably, external market forces will threaten the ability of many practice models to continue independently. Regardless of any immediate plans or desire to undergo the transaction process, every independent anesthesiology practice group should begin discussing preparation initiatives that will streamline operations, reduce costs, improve financial transparency and other specific measures to increase their overall enterprise value. Furthermore, the group leadership should evaluate and keep apprised of the options available, so that when the necessity arises, familiarity exists with the process and educated decisions can be made.

One-Time Sale

Large strategic buyers with practices spanning regional and national geographies may be interested in acquiring your physician practice—in order to establish their presence in a new market or strengthen their position in an established one. These buyers may seek for the acquisition of up to 100 percent of the practice. Five to seven year employment commitment contracts for the selling physicians at fair market salaries and standard non-compete agreements are typical expectations from the buyer in return for this “cash-out.” In some deals, the buyer will seek to have ancillary transaction consideration tied to performance-based “earn-out” arrangements in order to incentivize post-transaction performance by the service provider group.

Financial Recapitalizations

Private equity firms (referred to as “financial buyers”) may be looking to invest in your practice via infusion of financial capital in return for a controlling stake in the practice—a cashout of up to 80 percent of the equity value in the practice. They back privately held mergers and acquisitions (M&A) companies generally seeking to create a financial “exit” for themselves, typically through the sale of the company to an even larger company or, less commonly, by attempting to “go public” and selling shares on the stock market. Their strategy is not to hold forever—they focus on a growth strategy where they make their businesses large enough to pull returns from their investments. These buyers are most suitable as partners to a practice where the leadership is interested in an active approach to growth. These firms typically bring financial and operational expertise to the table to undertake a rapid top-line and bottom line expansion campaign. Once the growth strategy has been executed (in three to five years’ timeframe), the firm will look to sell ownership of the practice to another buyer, resulting in a cash-out of remaining ownership interest held by the original shareholders (commonly referred to as the “second bite of the apple”) at a substantially higher enterprise valuation.

Alternative Employment

If the opportunity to partner with a strategic or financial acquirer is no longer on the table, the group may continue its regular course or it may seek to be absorbed into employment within another group or with the hospital itself. While this provides opportunity to secure work and income with another group, this means any of the equity value and goodwill that was associated with original practice will be foregone—never to be realized. Physicians will receive fair market value salaries, but employment contracts are likely only to be short-term. This is often the least desirable scenario. With proper consultation and planning with the right M&A advisor—not a single dollar worth of value will be unnecessarily left behind.

Transaction Process

A physician group that decides that it wants to move forward with bringing another business partner into the picture should expect a transaction process that will run anywhere from six to twelve months. The stages of the process can be defined according to the following process chart:

Data Collection/CIM Creation—advisors work closely with key practice management and administration personnel to gather key financial and operational information about the practice to build a Confidential Information Memorandum (CIM), which will be used to market your practice. This will serve as an introduction to prospective buyers on what makes your group attractive and as a means of highlighting strengths of the practice. A qualified M&A advisor will work closely with you to develop this comprehensive brochure in order to expand on various aspects, including:

- General overview—history and background of the group, locations serviced, understanding of the ownership and reporting structure lines

- Management and operation model—key personnel biographies, staffing and service delivery models

- Operational and financial performance—case statistics and analysis of revenues, charges, collections and other accounting trends

Tactical Marketing—a campaign is thoughtfully planned and coordinated to reach the desired group of qualified transaction partners able and interested in merging with your practice. A qualified M&A advisor will solicit interest from these prospects on your behalf, coordinate for meetings with these suitors and strategize subsequent steps with your group in considering all viable options. In this stage, attention is given to differentiating characteristics among the buyers, particularly:

- Strategic vision—prospective acquirer’s business plan alignment with the interests of practice stakeholders

- Synergies/value-adds—business relationships, reporting and information systems, shared resources, negotiation leverage and payer rate arbitrage

Letter-of-Intent (LOI)—once the most suitable partners have been evaluated, the process of narrowing down the potential acquirers takes place. M&A advisors are critical in this stage, as they aid in the negotiation to arrive at favorable terms for the selling practice. Review of key factors, not limited to the cash that is being offered for the ownership, include:- Consideration offered—ancillary to cash offer and any contingencies tied to future receipts

- Employment and benefits—post transaction compensation rates, employment conditions and terms, and benefits packages

Preliminary terms of sale and an exclusivity agreement are drawn up in the form of a LOI and entered into between the parties, consummating the due diligence process for the buyer and limiting the ability of the seller to solicit offers from any other suitors.

Due Diligence—the buyer will initiate the comprehensive audit review process of the practice, performing procedures to assess the reliability of any assumptions upon which the buyer based its purchase price valuations. This process requires the business to submit numerous legal and financial records requests to the buyer for their evaluation, involving a significant amount of secondary requests and follow-up inquiries. A qualified M&A advisor will prepare the practice and its management to efficiently complete the process, will assume the bulk of the responsibilities in order to limit the impact on everyday business operations, and will help overcome obstacles encountered along the way.

Closing—upon conclusion of the diligence process, a Definitive Purchase Agreement is drafted according to the final terms agreed upon between the parties. Business continues as usual under the new ownership structure.

Selection Of Advisor

Before heading down the route selling of the practice, it is important for leadership to understand that hiring the right advisor is crucial for executing a successful transaction. The ideal M&A professionals will understand it is not only about selling your practice; it is also about understanding your practice, your partners and your unique value—in addition to finding both the optimal economics, as well as “the right fit and best partner” for your group.

The right M&A professionals will have extensive experience specific to the anesthesiology sector in order to advise you on a successful transaction. They will have completed numerous transactions with other independently-owned physician practices and have worked intimately with all of the prospective buyers of anesthesiology groups. A qualified M&A team will have an advisory board of healthcare professionals, including anesthesiologists, who have practiced, sold their groups, worked for large national anesthesiology companies and consulted on mergers and acquisitions of anesthesiology groups.

The right M&A professionals will be experts in handling communication among all of the interested parties within the transaction. They will recognize the importance of appropriate, timely and well-designed, on-point communication to the various internal constituencies.

- The Executive Committee or Equivalent—keeping them involved on issues and updated on progress being made, walking them through the offers and differentiate the relative pros and cons

- Shareholders—keeping them incrementally informed, educating them about the process, potential structures, employment provisions and other details of the transaction as it impacts life after the deal with their new partner

- Employees—leading town hall meetings with all the stakeholders to help introduce the Buyer and explain, amongst other things, how compensation and benefits will work post-closing

- Customers—strategizing on when and how best to inform them of the transaction

The benefits of hiring the most suitable M&A advisors when your group is investigating a transaction opportunity by far outweigh any cost savings thought to have been realized when considering anything less. The prime opportunity for the sale of your independent practice will only come around once—this is a consideration that deserves to be taken seriously. Have the best professionals on your side of the negotiation table.

Bill Britton is Co-Founder and Managing Director of Cross Keys Capital, LLC, Ft. Lauderdale, FL. He is a Wall Streettrained investment banker with a track record of success in M&A and corporate finance with Morgan Stanley and Fortune 500 companies. He leads the Cross Keys Capital Healthcare Services team working with physicianowned practice groups throughout the country. Mr. Britton has represented over 25 anesthesiology groups nationwide, serving as the sell-side advisor in facilitating transactions with a multitude of strategic and financial buyers. In 2013, Mr. Britton and Cross Keys Capital received the prestigious M&A Advisor Healthcare Deal of the Year Award for the firm’s advisory role in representing Broad Anesthesia Associates, LLC and Mid-Florida Anesthesia Associates, Inc. in their sale to Goldman Sachs Private Capital Investing, completing the formation of Resolute Anesthesia and Pain Solutions, LLC. He is a graduate of the Wharton School of Business. He can be reached at bbritton@ckcap.com.

While most physicians could deal with the implications of HIPAA, the passage of healthcare reform and the implementation of the Affordable Care Act, aka Obamacare, has been an entirely different matter. It is the very nature of the legislation that it presupposes structural changes in the market for healthcare, few of which are actually defined. At every level of healthcare delivery entities are struggling to envision a future that is as clear as the forest paths Frost described and to position themselves to be serious players. Never has U.S. healthcare seen such an explosion of activity. Two themes appear to be driving all the strategic considerations: quality and cost, for the underlying assumptions of Obamacare are that U.S. healthcare is too inconsistent and too expensive. Americans pay a huge premium for less than optimum care.

While most physicians could deal with the implications of HIPAA, the passage of healthcare reform and the implementation of the Affordable Care Act, aka Obamacare, has been an entirely different matter. It is the very nature of the legislation that it presupposes structural changes in the market for healthcare, few of which are actually defined. At every level of healthcare delivery entities are struggling to envision a future that is as clear as the forest paths Frost described and to position themselves to be serious players. Never has U.S. healthcare seen such an explosion of activity. Two themes appear to be driving all the strategic considerations: quality and cost, for the underlying assumptions of Obamacare are that U.S. healthcare is too inconsistent and too expensive. Americans pay a huge premium for less than optimum care. Jody Locke, MA serves as Vice President of Anesthesia and Pain Practice Management for ABC. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He will be a key executive contact for the group should it enter into a contract for services with ABC. Mr. Locke can be reached at

Jody Locke, MA serves as Vice President of Anesthesia and Pain Practice Management for ABC. Mr. Locke is responsible for the scope and focus of services provided to ABC’s largest clients. He is also responsible for oversight and management of the company’s pain management billing team. He will be a key executive contact for the group should it enter into a contract for services with ABC. Mr. Locke can be reached at  CMS has been encouraging coordinated care and quality through the Physician Quality Reporting System and the Value-Based Payment Modifier. Those programs, along with the Meaningful Use (EHR) incentive program, will be replaced on January 1, 2019 by the Merit-Based Incentive Payment System (MIPS) and Alternative Payment Models (APMs). CMS will pay up to a four percent bonus for high self-reported MIPS scores and up to a four percent penalty for poor performers, beginning in 2019. In 2019, therefore— assuming that the overall amount of penalties assessed offset the amount of bonuses, in budget-neutral fashion—the difference between maximum positive and negative scores will be eight percent and by 2022 the difference will be 18 percent—every single year. Might I ask what return on your business investment do you need? When did you achieve that return on your personal investment portfolio? Private payers are sure to soon follow suit, but this 18 percent CMS incentive alone is strong enough that anesthesiologists should fully embrace MIPS quality and coordinated metrics. As for APMs, if you receive a “significant portion” of your Medicare payments through an eligible APM entity, you will be totally exempt from the MIPS requirements. As a “qualifying APM participant,” you will receive a five percent bonus in each of the five years between 2019 and 2024. From 2026 onward, you will be eligible for 0.75 percent increase in your annual Medicare payments—half a percent more than physicians who merely satisfy MIPS.

CMS has been encouraging coordinated care and quality through the Physician Quality Reporting System and the Value-Based Payment Modifier. Those programs, along with the Meaningful Use (EHR) incentive program, will be replaced on January 1, 2019 by the Merit-Based Incentive Payment System (MIPS) and Alternative Payment Models (APMs). CMS will pay up to a four percent bonus for high self-reported MIPS scores and up to a four percent penalty for poor performers, beginning in 2019. In 2019, therefore— assuming that the overall amount of penalties assessed offset the amount of bonuses, in budget-neutral fashion—the difference between maximum positive and negative scores will be eight percent and by 2022 the difference will be 18 percent—every single year. Might I ask what return on your business investment do you need? When did you achieve that return on your personal investment portfolio? Private payers are sure to soon follow suit, but this 18 percent CMS incentive alone is strong enough that anesthesiologists should fully embrace MIPS quality and coordinated metrics. As for APMs, if you receive a “significant portion” of your Medicare payments through an eligible APM entity, you will be totally exempt from the MIPS requirements. As a “qualifying APM participant,” you will receive a five percent bonus in each of the five years between 2019 and 2024. From 2026 onward, you will be eligible for 0.75 percent increase in your annual Medicare payments—half a percent more than physicians who merely satisfy MIPS.

The industry is at a point in its life cycle when size matters, and many of the large buyers are bundling different physician and multispecialty services to gain critical mass and achieve greater bargaining power for contracts and resources. The regulatory environment is becoming increasingly tumultuous with recent legislated healthcare reforms, such as bundled payments, pay-for performance, value-based purchasing and accountable care organizations.

The industry is at a point in its life cycle when size matters, and many of the large buyers are bundling different physician and multispecialty services to gain critical mass and achieve greater bargaining power for contracts and resources. The regulatory environment is becoming increasingly tumultuous with recent legislated healthcare reforms, such as bundled payments, pay-for performance, value-based purchasing and accountable care organizations.

Letter-of-Intent (LOI)—once the most suitable partners have been evaluated, the process of narrowing down the potential acquirers takes place. M&A advisors are critical in this stage, as they aid in the negotiation to arrive at favorable terms for the selling practice. Review of key factors, not limited to the cash that is being offered for the ownership, include:

Letter-of-Intent (LOI)—once the most suitable partners have been evaluated, the process of narrowing down the potential acquirers takes place. M&A advisors are critical in this stage, as they aid in the negotiation to arrive at favorable terms for the selling practice. Review of key factors, not limited to the cash that is being offered for the ownership, include: Bill Britton is Co-Founder and Managing Director of Cross Keys Capital, LLC, Ft. Lauderdale, FL. He is a Wall Streettrained investment banker with a track record of success in M&A and corporate finance with Morgan Stanley and Fortune 500 companies. He leads the Cross Keys Capital Healthcare Services team working with physicianowned practice groups throughout the country. Mr. Britton has represented over 25 anesthesiology groups nationwide, serving as the sell-side advisor in facilitating transactions with a multitude of strategic and financial buyers. In 2013, Mr. Britton and Cross Keys Capital received the prestigious M&A Advisor Healthcare Deal of the Year Award for the firm’s advisory role in representing Broad Anesthesia Associates, LLC and Mid-Florida Anesthesia Associates, Inc. in their sale to Goldman Sachs Private Capital Investing, completing the formation of Resolute Anesthesia and Pain Solutions, LLC. He is a graduate of the Wharton School of Business. He can be reached at

Bill Britton is Co-Founder and Managing Director of Cross Keys Capital, LLC, Ft. Lauderdale, FL. He is a Wall Streettrained investment banker with a track record of success in M&A and corporate finance with Morgan Stanley and Fortune 500 companies. He leads the Cross Keys Capital Healthcare Services team working with physicianowned practice groups throughout the country. Mr. Britton has represented over 25 anesthesiology groups nationwide, serving as the sell-side advisor in facilitating transactions with a multitude of strategic and financial buyers. In 2013, Mr. Britton and Cross Keys Capital received the prestigious M&A Advisor Healthcare Deal of the Year Award for the firm’s advisory role in representing Broad Anesthesia Associates, LLC and Mid-Florida Anesthesia Associates, Inc. in their sale to Goldman Sachs Private Capital Investing, completing the formation of Resolute Anesthesia and Pain Solutions, LLC. He is a graduate of the Wharton School of Business. He can be reached at